Key Takeaways for Carnival Corporation Stock

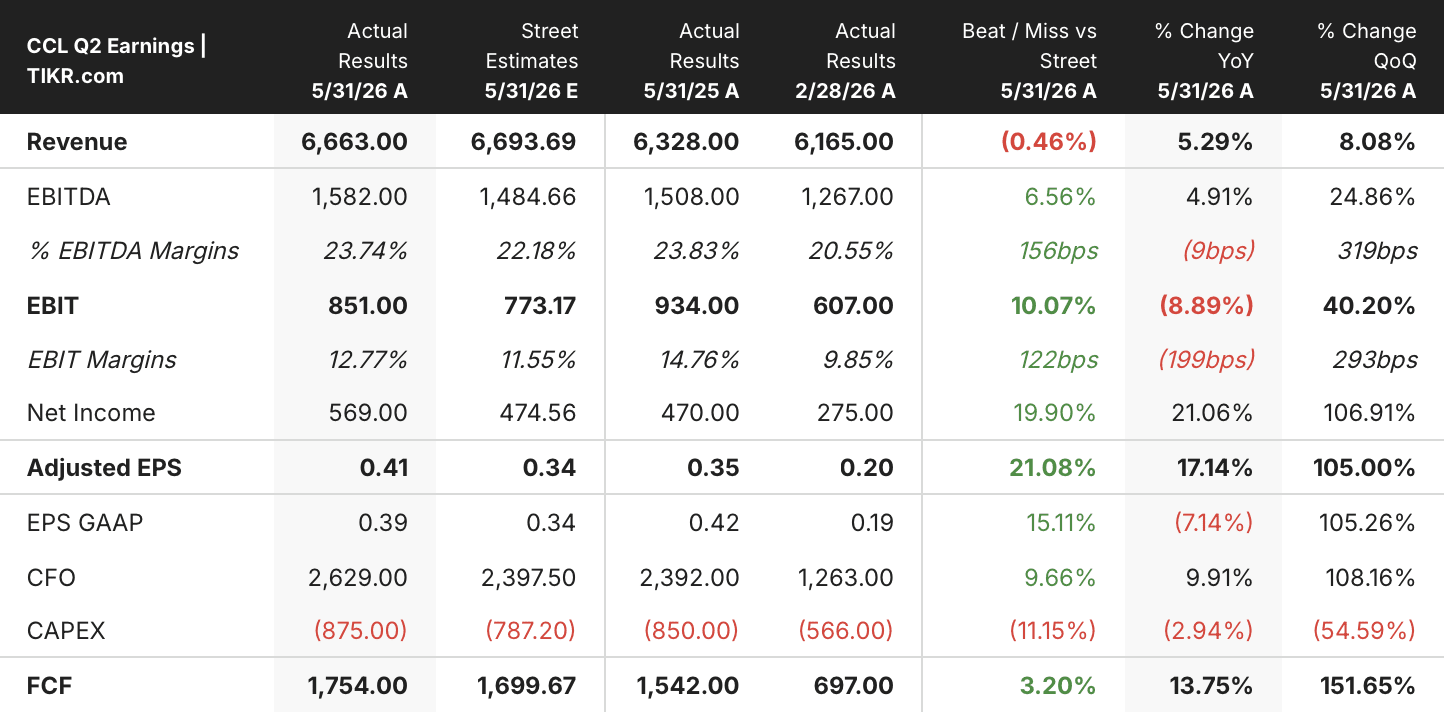

- Carnival Corporation delivered Q2 2026 net income of $569 million, more than 20% above the prior year.

- Revenue grew 5% year-over-year to $6.66 billion, marking the 12th consecutive quarter of record net yields.

- Operating income reached $851 million, with operating margins expanding to 13% from 9% in the prior quarter.

- TIKR’s model values CCL at around $54, implying roughly 86% total return from the current price of $29.

Carnival Corporation Beat Q2 Guidance by $100 Million But the Cost Story Is the Real Headline

Carnival Corporation (CCL), the world’s largest cruise operator with a fleet spanning nine global brands, delivered record Q2 2026 results on June 23, posting net income of $569 million while outperforming its own March guidance by $100 million despite active geopolitical volatility and near-historic fuel prices.

Revenue came in at $6.66 billion, up 5% year-over-year, though that figure carries context: CCL’s European deployments absorbed a direct hit from the prolonged Middle East conflict, which compressed close-in booking volumes and elevated airfares for North American guests sailing to Mediterranean itineraries.

The number that most validates the quarter is $9 billion, which is an all-time high in customer deposits, signaling that forward demand remains structurally intact even as near-term European yields softened.

CEO Josh Weinstein told analysts the yield impact is “transitory,” pointing to a reversal already visible in June booking trends.

Cruise costs without fuel per available lower berth day (ALBD — a per-capacity cost measure) were essentially flat year-over-year, beating cost guidance by around 250 basis points; CFO David Bernstein confirmed the majority of those savings are permanent, not timing-related.

Fuel efficiency improved by more than 5%, building on the prior year’s over 6% gain.

The company enters the second half of 2026 with 93% of capacity on the books at record prices, and Weinstein described 2027 European bookings as running “up year-over-year in mid-teens percentages at higher prices.”

Gross Profit Growth Is Decelerating, But Cost Structure Discipline Is Doing the Work Below the Line

Carnival’s gross profit grew 3% year-over-year to $3.51 billion in Q2 2026, while gross margins held at 53%, roughly flat with the prior quarter and below the 59% peak logged in the summer quarter of fiscal 2025.

The compression at the gross level was expected: cost of goods sold rose to $3.16 billion as fuel prices ran nearly 30% above the prior year.

Total operating expenses came in at $2.65 billion, a sequential improvement from the $3.07 billion reported in the prior quarter.

Operating income landed at $851 million, up 2% year-over-year, while operating margins expanded to 13%, the highest level in three quarters.

The gap between 53% gross margins and 13% operating margins is wide, but the trajectory is what the income statement is signaling: SG&A held near $860 million, and the sequential decline in total operating expenses confirms management is pulling on structural levers.

CCL Trades at a Persistent Operating Margin Discount to RCL Across Every Quarter on Record

Royal Caribbean (RCL) posted operating margins of 26% in the most recent quarter, more than double Carnival’s 13% in the same period.

The gap is not new and not narrow: RCL has held a margin advantage over CCL in every quarter shown, ranging from a 6-point spread in the off-peak winter quarters to a 20-point spread at the summer peak.

Norwegian Cruise Line (NCLH) closed Q2 2026 at 11% operating margins, sitting below both peers and illustrating that Carnival’s 13% sits in the middle of the competitive range, not at the bottom.

The structural question the chart raises is whether CCL’s cost discipline, which held unit costs flat against a nearly 30% fuel price increase this quarter, is the beginning of a compression of that RCL gap or simply a floor being defended.

In the peak summer quarter of fiscal 2024, CCL reached 28% operating margins against RCL’s 33%, a 5-point gap that represents the closest the two companies have traded on this metric in the data shown.

That prior peak suggests the margin discount to RCL is partially cyclical, narrowing when cruise demand is strongest, and the second half of 2026 — with 93% of capacity booked at record prices — sets up as the next test of how much of that gap Carnival can close.

TIKR’s $54 Target on CCL Stock Holds, If Cost Discipline Converts to Margin Recovery in the Back Half

TIKR’s model values Carnival Corporation at approximately $54 by November 2030, implying around 86% total return from the current price of $29, or roughly 15% per year.

The credibility of that target rests on one condition the income statement is already beginning to satisfy: operating expenses declining as a percentage of revenue while gross profit compounds modestly.

If flat unit costs in Q2 persist into the second half where Carnival enters with 93% capacity booked at record prices, operating margins should widen materially, and that is the mechanism the TIKR model is pricing.

Should You Invest in X?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up X stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track X alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CCL stock on TIKR for Free →