Key Stats for UPS Stock

- Past week’s performance: Consolidating

- 52-week range: $82.00 to $122

- Valuation model target price: $139

- Implied upside: +27.9% over the next 2.5 years

Build your own UPS valuation scenario on TIKR (It’s free) >>>

FedEx’s Margin Miss Puts the Whole Parcel Sector in Focus

United Parcel Service (UPS) shares came into focus this week as FedEx reported earnings on June 24 that highlighted the margin pressure running through the freight and parcel industry. FedEx’s operating margins compressed, and shares fell sharply, according to Reuters, even as the company guided for 11% revenue growth in fiscal 2026. That disconnect between top-line optimism and bottom-line execution is the same dynamic investors have been watching at UPS for the past year.

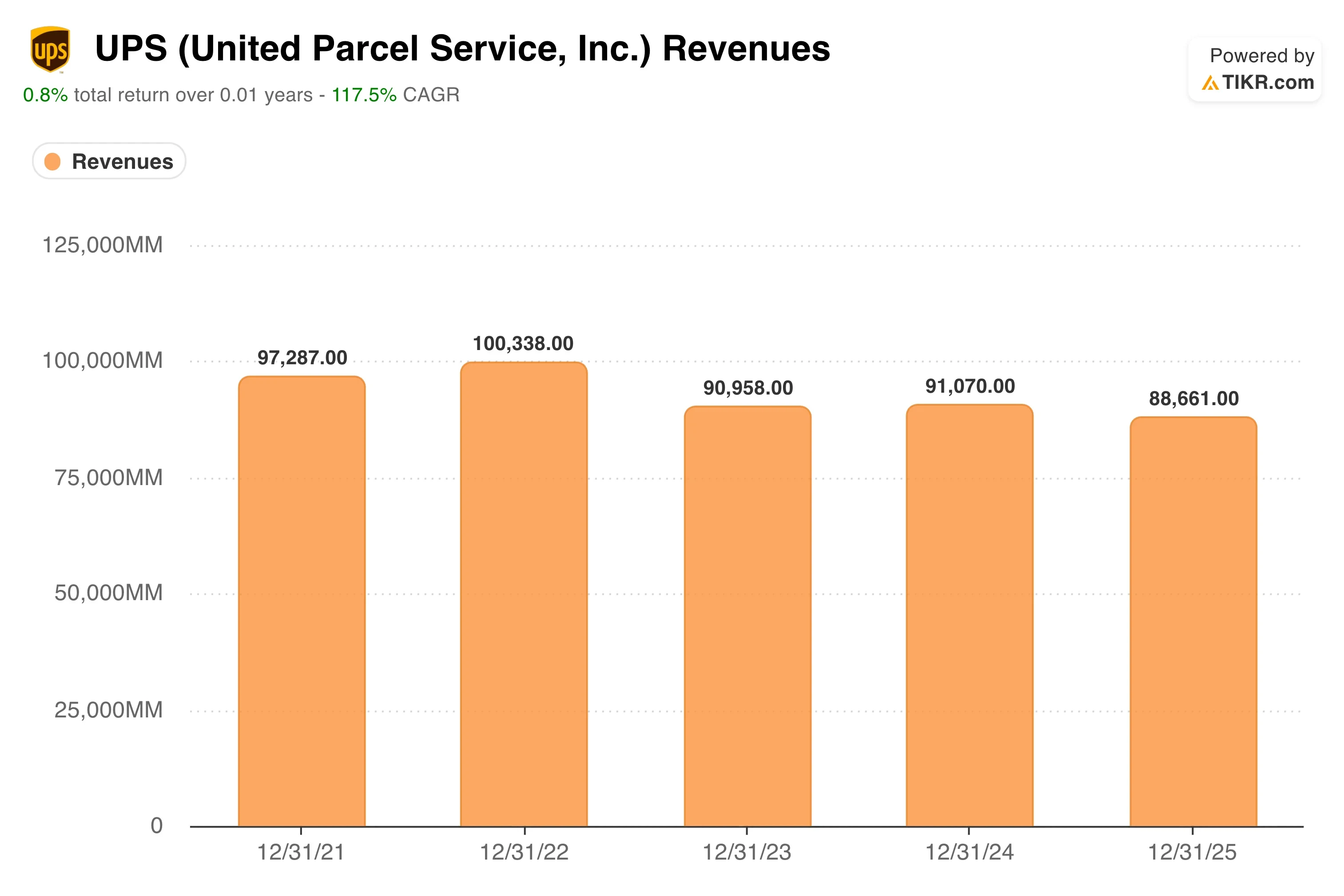

UPS has been in its own restructuring cycle. The company cut costs aggressively following the post-pandemic parcel boom and subsequent volume normalization. Revenue declined 2.6% over the past year, reflecting lower package volumes and pricing pressure. That contraction is the backdrop against which UPS’s current network investments must be assessed.

On June 22, UPS announced a $48 million investment in 27 temperature-controlled freight cross-dock facilities worldwide, according to Reuters. Cross-dock facilities are sorting hubs where freight moves directly from inbound to outbound trucks without long-term storage. The temperature-controlled component targets pharmaceuticals and time-sensitive food freight, which are higher-margin categories than standard parcels. That investment follows a nearly $50 million North American logistics expansion announced in late May, signaling a deliberate shift toward specialized freight.

CEO Carol Tomé has consistently argued that higher-margin, contractually committed freight is more valuable than raw volume. Going forward, UPS stock will be assessed on whether that network repositioning translates into operating margin recovery toward the double-digit levels the company historically maintained before the post-pandemic volume correction.

See analysts’ growth forecasts and price targets for UPS (It’s free) >>>

Is UPS Stock Cheap at $109?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 2.9%

- Operating Margins: 10.1%

- Exit P/E Multiple: 14.2x

Based on these inputs, the model estimates a target price of $139, implying 27.9% total upside and a 10.2% annualized return over the next 2.5 years.

A 10.2% annualized return combined with a 6% current dividend yield is the right frame for this story. UPS is not a growth stock. But it is a dividend-paying logistics franchise with a capital appreciation overlay, and at $109, the combination makes the setup more compelling than the recent price action suggests.

A five-year operating-margin trend chart is the most useful visual here. It shows that UPS operated at margins above 12% for most of the past decade before volume normalization compressed profitability toward the current 9.1% LTM EBIT level. The model’s 10.1% margin target for 2028 is actually below UPS’s longer-term historical range, so the valuation rests on conservative margin recovery assumptions rather than an optimistic rebound.

Revenue growing at 2.9% per year reflects the expectation that parcel volumes will recover modestly as e-commerce stabilizes. That is not a bold forecast. The one-year historical revenue CAGR of negative 2.6% makes 2.9% forward growth look attainable if volumes have genuinely bottomed.

The exit P/E of 14.2x matches UPS’s own five-year historical multiple of 15.5x, so the model assumes no multiple expansion. Investors are essentially paying for a dividend-paying logistics franchise at or below historical valuation. FedEx’s margin trouble reinforces the bear case that the industry is still digesting overcapacity, but it also makes UPS’s specialized freight push look like the right strategic response.

UPS vs. FedEx and the Broader Logistics Landscape

FedEx (FDX) is the most direct peer, and its June 24 earnings provided the clearest sector-level read in weeks. FedEx guided for 11% revenue growth in fiscal 2026 but saw margins compress. That combination suggests volume is returning to the freight sector, but cost discipline remains the key competitive differentiator. UPS’s $48 million investment in specialized cross-dock infrastructure is a direct response to that same market dynamic.

On valuation, UPS trades at roughly 14.5x NTM earnings, in line with FedEx and at a discount to the broader S&P 500. UPS’s LTM net debt to EBITDA ratio of 1.59x is manageable and suggests the company can sustain its dividend while funding network investments simultaneously. That financial flexibility is a competitive advantage in a sector where overcapacity and cost pressure are still forcing difficult choices.

Amazon’s recent launch of a less-than-truckload freight offering rattled the trucking sector in mid-June, according to Reuters. Investors worried Amazon could replicate in freight what it did in last-mile parcel delivery. UPS and FedEx have more diversified freight and international operations than the pure-play trucking companies most affected. But the Amazon expansion is a long-term structural overhang on pricing power across the logistics sector.

UPS’s competitive moat lies in its integrated global network, its healthcare and specialized freight capabilities, and its enterprise customer relationships. Those advantages do not disappear in a tougher volume environment. Yet they require sustained capital investment to maintain, which is precisely what the cross-dock and North American expansions represent.

See what the Amazon threat could mean for UPS investors >>>

What’s Driving UPS Stock Going Forward?

Fiscal Q2 results and any revision to full-year guidance are the most critical near-term catalysts. UPS has been cautious on volume recovery, and any sign that package volumes are stabilizing ahead of schedule would likely trigger a meaningful re-rating toward the $140 model target.

The temperature-controlled freight expansion addresses a structurally attractive market. Pharmaceutical cold-chain logistics, meaning the regulated transport of drugs and biologics requiring specific temperature ranges, is growing as biotech shipment volumes increase globally. UPS’s $48 million investment in 27 cross-dock facilities positions it to capture more of that market from existing healthcare customer relationships.

The North American automotive and industrial logistics expansion announced in late May opens another specialized channel. Manufacturing reshoring, driven partly by recent trade policy changes, is increasing demand for just-in-time freight services within North America. UPS is investing in air freight capacity in Mexico to serve that trend, according to Reuters, which adds a geographic revenue dimension that FedEx does not yet match at the same scale in that market.

Cost discipline remains the most important internal lever. UPS has been reducing headcount and renegotiating contracts, and the effects will appear in operating margins over the next two to three quarters. If margin recovery tracks toward the model’s 10.1% assumption, the stock’s 6% dividend yield provides a meaningful total-return floor while investors wait for the recovery thesis to fully materialize.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in United Parcel Service?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UPS stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!