Key Stats for Figma Stock

- Current Price: $18.62

- Target Price (Mid): ~$59

- Street Target: ~$36

- Potential Total Return: ~217%

- Annualized IRR: ~29% / year

- Earnings Reaction: +13.24% (5/14/26)

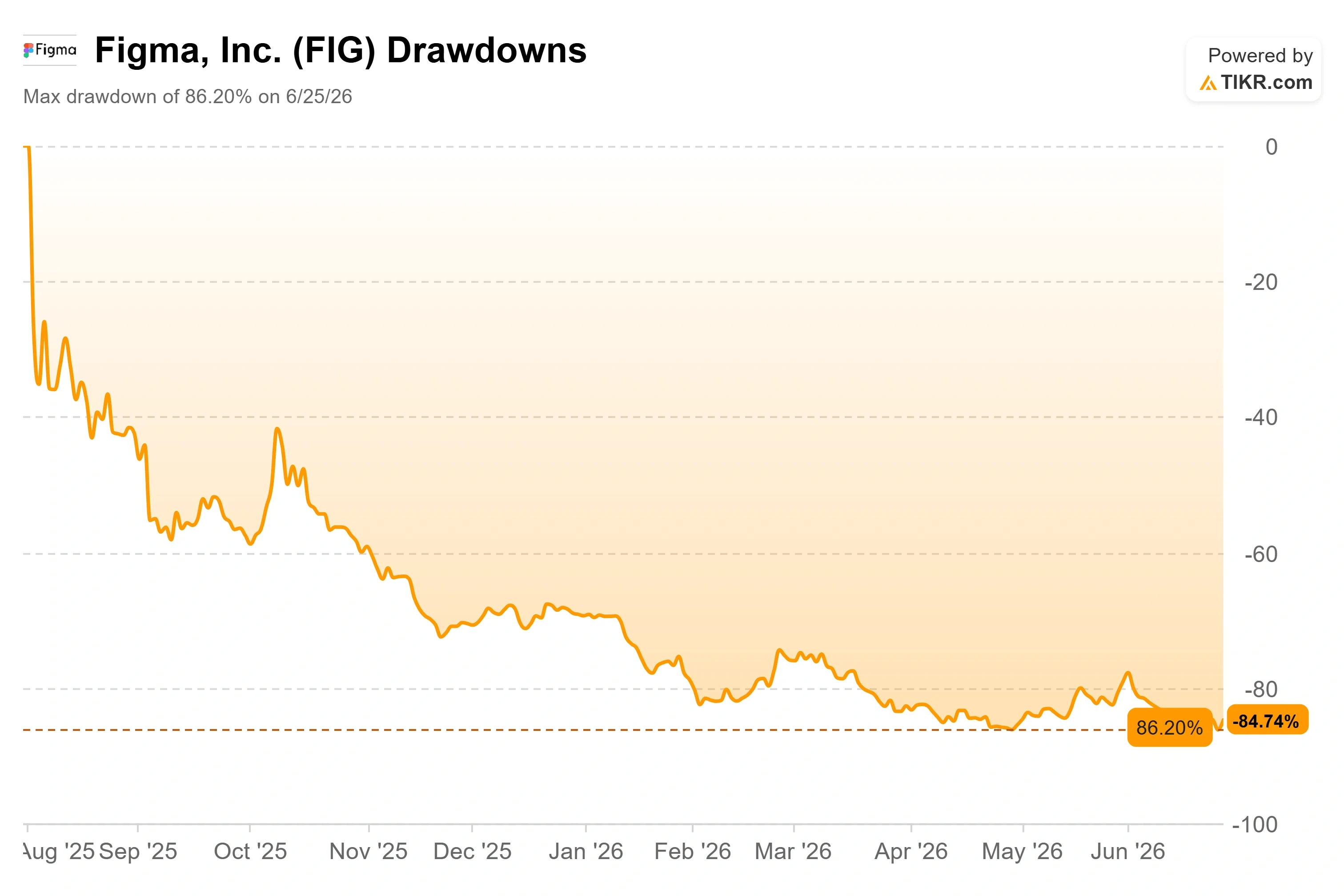

- Max Drawdown: 86.20% (6/25/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Figma, Inc. (FIG) gained 10.57% on June 26 to close at $18.62, capping a stretch of days where buyers finally stepped in near the lows. The bounce barely registers on the chart. The stock still sits about 87% below its 52-week high of $142.92, and its drawdown bottomed at 86.20% on June 25. That gap is the whole story. Figma stock in 2026 has become a fight between a business that is reaccelerating and a market convinced artificial intelligence will hollow it out. One side points to 46% revenue growth. The other points to a rival design tool built by Figma’s own former boardroom partner. Neither side has been proven right, which is why the stock can swing 10% in a session without a single clear catalyst.

The question the market cannot answer is simple. Is an 87% drawdown a broken company, or a mispriced one?

The Catalysts Sitting Under the Stock

Two dated events frame the current setup. On June 17, Citi initiated coverage with a Buy rating and a $36 price target, and FIG rose about 4% that session. Weeks earlier, on May 28, Findell Capital Management issued a letter and report to Figma’s CEO and board. The activist campaign has stayed an overhang ever since, and it is the more consequential of the two.

That campaign is not about a competitor. It is about the board. Findell demanded three things: a simpler product lineup, costs brought in line with peers, and a governance review of one specific sequence of events. Anthropic’s Chief Product Officer, Mike Krieger, resigned from Figma’s board on April 14. Three days later, on April 17, Anthropic launched Claude Design, a product Findell described in its own letter as one that directly competes with Figma. Findell called for an independent board investigation into whether confidential information moved across that line, and it flagged that two remaining directors carry economic exposure to Anthropic through their venture firms. These are allegations in a shareholder letter, not findings.

The cost critique is sharper. Findell noted that analyst estimates call for Figma to spend roughly $375 million, around 27% of revenue, on stock-based compensation in 2026, versus about 8% of revenue at Adobe in its most recent quarter. For a company still posting GAAP losses, share dilution at that scale is a real drag on per-share value. Investors appear to welcome the pressure rather than fear it, because tighter spending and sharper focus are exactly what a loss-making grower needs.

See historical and forward estimates for Figma stock (It’s free!) >>>

The Business Is Doing the Opposite of What the Chart Suggests

Strip out the noise, and Figma’s first quarter was its strongest as a public company. Revenue grew 46% year-over-year to $333 million in Q1 2026, accelerating from 40% the prior quarter. Net dollar retention, which measures how much more existing customers spend over time, reached 139%, the highest in over two years. Paid customers grew 54% year-over-year to roughly 690,000.

The number that matters most for the AI debate is willingness to pay. Figma began enforcing AI credit limits on March 18. As of late April, over 75% of Org and Enterprise users who had previously exceeded their limits kept consuming credits under the new paid system. CFO Praveer Melwani put the monetization milestone plainly on the Q1 2026 earnings call: “With full seat AI credit limits now live, growing AI usage and adoption now translates into revenue.” That sentence is the bridge between Figma’s product story and its income statement, because it converts engagement into dollars for the first time.

CEO Dylan Field addressed the Anthropic threat directly rather than dodging it. “I think when it comes to Anthropic, obviously, we can’t dismiss them,” he said on the call, before arguing that Figma’s performant multiplayer canvas and deep product context are hard to replicate. That candor matters because the entire bear case rests on whether management sees the threat clearly. The market reacted to the print: FIG rose 13.24% on the day of the May 14 release, the strongest earnings-day gain among its reported quarters.

What the Valuation Says When You Run the Numbers

Here is where the disconnect gets quantified. Figma trades at about 5.5x next-twelve-months revenue, a multiple that has compressed from above 21x a year ago. On a peer basis, the contrast is stark. Adobe trades at roughly 3.0x NTM revenue, and Manycore Tech trades at roughly 17x. Figma sits between them on multiple fronts but grew revenue by around 46% last quarter, faster than either. A near-46%-grower priced at 5.5x forward sales is not the valuation of a company the market believes in. It is the valuation of one of the markets that is bracing to be disrupted.

That fear is not baseless. Google launched a free AI design tool, Stitch, earlier this year, and Anthropic’s Claude Design followed in April. If foundation-model providers commoditize design generation, Figma’s pricing power erodes, and the growth assumption breaks. There is also a disclosed risk worth naming plainly: Figma has stated in a filing that Anthropic’s legal dispute with the U.S. government over Claude’s federal supply-chain status could affect Figma’s government sales, since Claude powers some of its federal AI products. The bull case is that switching costs are real, retention is rising, and AI is showing up as a revenue tailwind rather than a leak. The bear case is that the most dangerous competitor sat on the board until April, and the next few quarters will decide which read is correct.

See how Figma performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $18.62

- Target Price (Mid): ~$59

- Potential Total Return: ~217%

- Annualized IRR: ~29% / year

See analysts’ growth forecasts and price targets for Figma stock (It’s free!) >>>

Using TIKR’s mid-case scenario, the model puts a target price of around $59 on Figma stock, realized at the end of 2030. If those assumptions hold, that implies around 217% total upside and roughly a 29% annualized return over the next four and a half years. The mid case is the right lens here because it assumes disciplined execution, not a miracle.

Two revenue drivers carry the forecast: continued seat expansion across enterprise organizations, and AI credit monetization now that paid limits are live and converting. The margin driver is operating leverage, as Figma’s roughly 80% gross margin lets revenue growth flow toward profitability while management leans on model routing and first-party models to manage inference costs. The primary risk is AI commoditization: if rivals like Claude Design erode pricing power, the around 19% mid-case revenue CAGR does not hold.

The upside: if AI converts from threat to tailwind and seat growth compounds, the model’s around $59 target reflects a durable software platform the market mispriced in a panic.

The downside: if growth decelerates toward 30% and losses persist, a re-rating toward the Street’s around $36 target, or lower, is the more honest outcome.

Conclusion

The next real test is the August quarter. Watch one number above all: net dollar retention. It hit 139% in Q1, and the second full quarter of AI credit monetization will show whether that holds or fades. Above 135% with continued credit consumption confirms the thesis that AI is a tailwind. A drop toward the high 120s, paired with revenue growth slipping below the high 30s, would hand the bears their proof and put the around $36 Street target back in focus. The board’s response to Findell is the wild card that could move the stock first. If Figma announces a governance review or explicit cost targets before August, the re-rating may start before the numbers ever arrive.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Figma?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Figma, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Figma alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!