Key Stats for UPS Stock

- Past week’s performance: +5.7%

- 52-week range: $82 to $122

- Valuation model target price: $135

- Implied upside: 34.1% over 2.6 years

Value your favorite stocks like UPS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Parcel Service (UPS) gained 5.7% this week but remains under meaningful competitive and macroeconomic pressure. First-quarter 2026 revenue came in at $21.2 billion, edging past the analyst consensus estimate of $21.0 billion.

Net income fell 27.2% to $864 million, while revenue declined 1.6% year over year. CEO Carol Tome warned that rising fuel costs and weaker US consumer confidence may reduce demand through 2026.

The week’s most disruptive development came from outside the UPS earnings report. Amazon announced on May 4 that it is opening its own logistics network to external businesses, creating a direct competitor to UPS and FedEx in the parcel delivery market.

Parcel delivery stocks dropped sharply on that news but have since partially recovered. Amazon’s logistics expansion poses a structural competitive threat that investors are still sizing, prompting investors to apply significant selling pressure across the sector.

On the positive side, UPS declared its quarterly dividend of $1.64 per share, which translates to an annual yield of approximately 6.5% at the current share price. That income yield provides meaningful support for shareholders weathering the current earnings cycle.

Shareholders also approved the 2026 omnibus incentive compensation plan at the May annual meeting. Board member Kevin Warsh resigned effective May 13, 2026, and the company remains engaged in the ongoing NTSB investigation into the fatal Kentucky cargo crash.

Going forward, UPS’s stock recovery depends on whether management can stabilize volumes and defend margins while navigating the emerging Amazon logistics threat.

See analysts’ growth forecasts and price targets for UPS (It’s free) >>>

Is UPS Stock Undervalued?

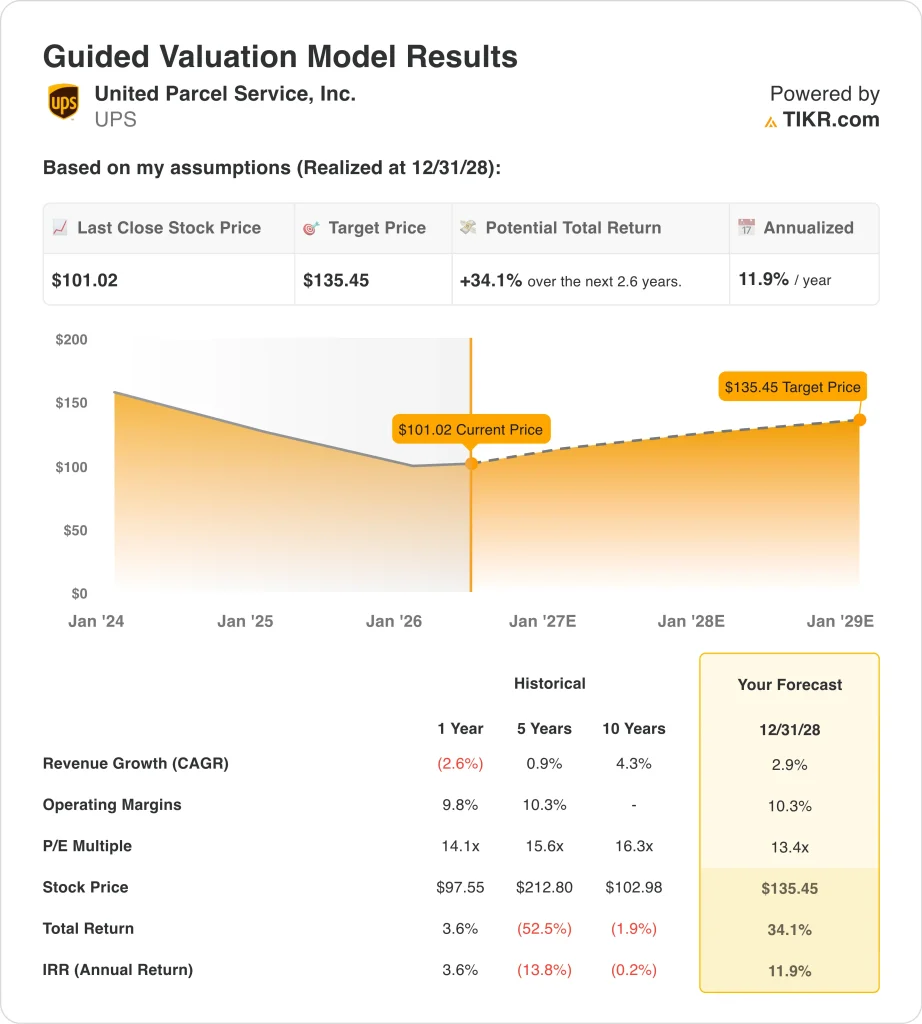

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 2.9%

- Operating Margins: 10.3%

- Exit P/E Multiple: 13.4x

Based on these inputs, the model estimates a target price of $135, implying 34.1% total upside from the current share price of $101 and an annualized return of 11.9% over the next 2.6 years.

United Parcel Service is the world’s largest package delivery company, operating a global logistics network across more than 220 countries and territories. The 2.9% revenue CAGR assumption is deliberately modest and reflects the headwinds UPS faces from softening package volumes, a more competitive landscape, and macroeconomic uncertainty.

The 10.3% operating margin target aligns with UPS’s five-year historical average and represents only a modest improvement from the current 9.1% LTM EBIT margin. Achieving that recovery will require cost discipline from the 2025 restructuring, which eliminated approximately 48,000 positions across management and operations.

If fuel costs stabilize and consumer confidence recovers modestly, the resulting operating leverage could push margins back toward 10% without requiring meaningful volume growth.

At 13.4x exit earnings, the valuation is conservative and appropriate for a mature logistics business facing structural headwinds. The stock trades at $101, roughly 17% below its 52-week high of $122, so the current entry point offers a real discount from recent valuations.

Combined with a 6.5% dividend yield, the 11.9% projected annual return makes UPS one of the more attractive risk-adjusted setups among large-cap industrial companies trading near multi-year lows.

What’s Driving UPS Stock Going Forward?

Volume recovery is the single most important variable in the UPS recovery case. The company reported 1.6% lower revenue in Q1 2026 despite beating estimates, which means underlying volume trends remain under pressure.

In the second-quarter report expected July 28, management must show that package volumes are stabilizing. Revenue per piece also needs to hold or improve, since pricing is the other lever UPS controls alongside cost management.

The Amazon logistics network announcement is a longer-term structural risk but not an immediate threat to near-term results. Amazon has historically prioritized fulfillment of its own packages, and redirecting that capacity toward external shippers requires significant time, capital, and operational restructuring.

UPS maintains decades of global infrastructure, air and ground network coverage, and deep enterprise relationships that Amazon cannot replicate quickly. The competitive threat is real and worth monitoring, but its impact is likely measured in years rather than in the next few quarters.

Cost management continues to be a near-term priority following the 2025 restructuring. UPS and its Teamsters workforce reached a settlement on driver severance packages in April 2026, removing one source of operational uncertainty.

Separately, UPS, FedEx, and DHL are urging the European Union to phase in new low-value package duty rules gradually, which could protect international volume if regulators adopt a more measured approach to implementation.

If UPS stock can demonstrate margin improvement across the second-half 2026 earnings cycle, the combination of a 34.1% total return model and a 6.5% dividend yield creates a compelling recovery setup for patient investors.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in United Parcel Service?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UPS stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!