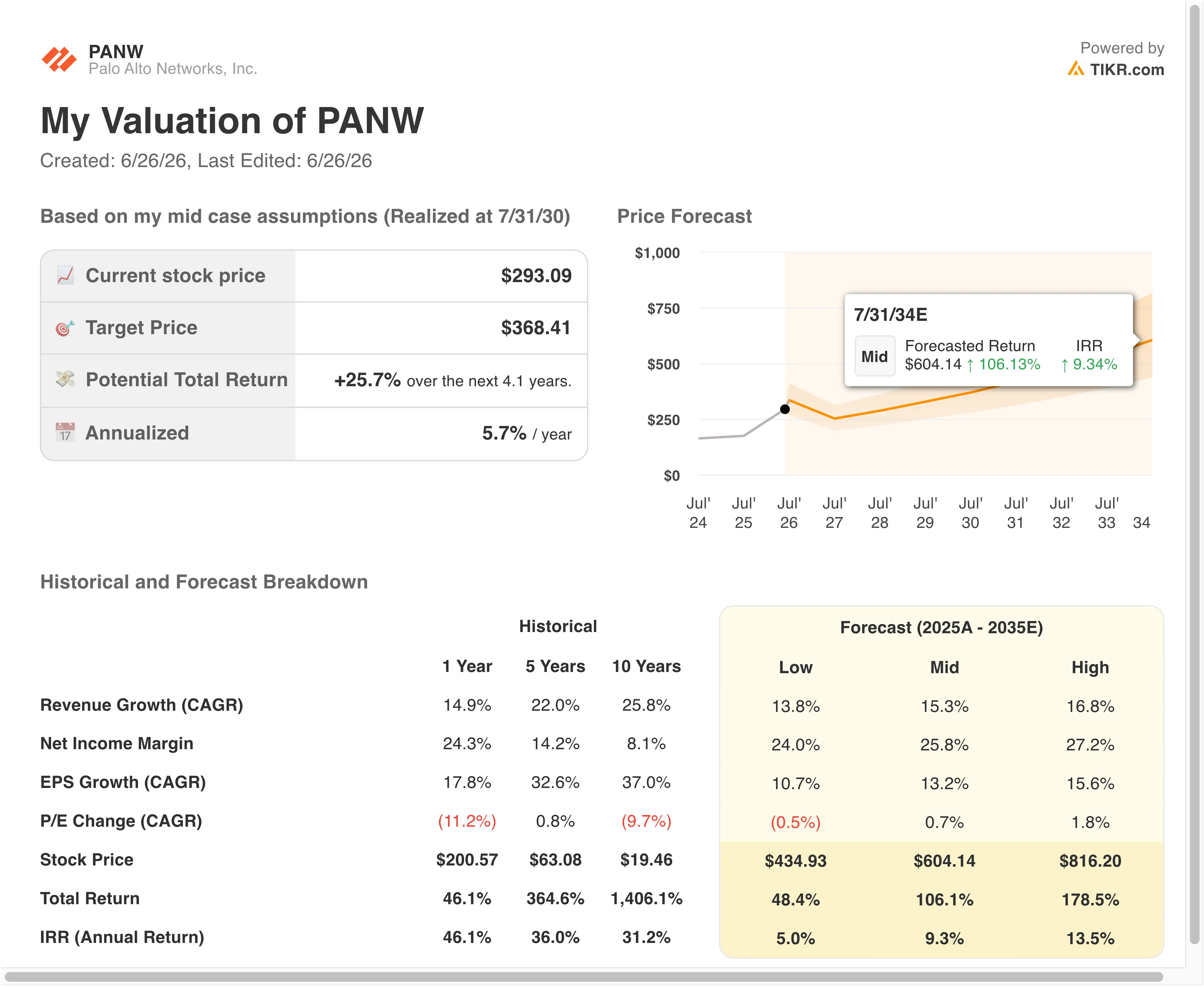

Key Stats for PANW Stock

- Past week’s performance: 6.22%

- 52-week range: $139 to $302

- Valuation model target price: $360

- Implied upside: +23% over the next 2.1 years

Value your favorite stocks like PANW with 5 years of analysts’ forecasts using TIKR’s new Valuation Model >>>

Palo Alto Delivers a Standout Q3 and Raises the Full-Year Bar

Palo Alto Networks (PANW) delivered one of the cleanest earnings reactions in cybersecurity this month. The company reported fiscal Q3 revenue of $3.0 billion, up 31% year over year, and raised its full-year forecast. Management cited AI-driven demand for its cybersecurity platform as the primary growth engine.

The revenue figure deserves context. Of the $3.0 billion in Q3 revenue, $388 million came from the CyberArk and Chronosphere acquisitions. That means organic growth ran at a lower rate than the headline 31% suggests. Still, the beat against the $2.94 billion consensus was real, and the platform momentum across Cortex, Prisma, and Strata was broad-based.

CEO Nikesh Arora said: “Q3 was a standout quarter for Palo Alto Networks, with accelerating organic bookings growth as customers turn to us to secure their AI deployments at scale.” CFO Dipak Golechha added that the company is “executing ahead of M&A integration plans” and “on track to achieve 40% adjusted free cash flow margin in FY28.” Full-year revenue guidance was raised to $11.415–$11.425 billion, and Q4 revenue is expected between $3.345–$3.355 billion, up 32% year over year.

Partnerships are amplifying the momentum. On June 9, Palo Alto and Deutsche Telekom launched Sovereign Cortex, an AI security offering for regulated European industries. On June 24, Palo Alto expanded Project Lightwell with IBM and Red Hat, adding agentic AI security capabilities. If PANW stock holds near $293, the next test will be fiscal Q4 results in August.

See analysts’ growth forecasts and price targets for PANW (It’s free) >>>

Is Palo Alto Networks Stock Undervalued at $293?

Under valuation model assumptions realized through 7/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 19.3%

- Operating Margins: 30.0%

- Exit P/E Multiple: 65.0x

Based on these inputs, the model estimates a target price of $360, implying 23% total upside and a 10.4% annualized return over the next 2.1 years.

A 10.4% annualized return from a cybersecurity platform leader is not spectacular, but it is not dismissible either. Revenue growing at 19.3% annually represents a deceleration from the Q3 headline rate. But it also accounts for a much larger revenue base. Palo Alto is already generating $3 billion per quarter, so maintaining high-teens growth at scale is a genuine achievement.

A revenue and forward-estimates chart is the right visual to anchor this section. It shows the trajectory clearly: revenue growth bottomed when platformization compressed billings, then recovered sharply as consolidation contracts matured. Placing this chart here lets readers see whether the Q3 result is a true inflection or a one-quarter anomaly.

Operating margins expanding to 30% from the current last-twelve-month EBIT margin of 9.1% looks like a wide gap. But it reflects the fact that GAAP margins include significant stock-based compensation and acquisition-related amortization. On an adjusted basis, Palo Alto’s profitability is materially higher, and the model’s 30% target aligns with adjusted operating profitability. Investors should keep that distinction in mind when comparing these margins to peers.

The exit P/E of 65x is the most grounded assumption. Palo Alto’s NTM P/E currently sits at roughly 75x, so the model actually assumes some multiple compression by mid-2028. That is reasonable if revenue growth decelerates modestly and interest rates remain elevated.

Compare Palo Alto’s margin trajectory against CrowdStrike and Zscaler on TIKR >>>

How Palo Alto Networks Compares to Its Cybersecurity Peers

CrowdStrike (CRWD) is the most direct comparison on platform breadth. CRWD grew revenue 26% in its most recent quarter and delivered record free cash flow, but the revenue growth rate disappointed investors expecting acceleration. Palo Alto’s 31% revenue growth with a raised full-year forecast puts it ahead of CrowdStrike on near-term momentum. CRWD’s NTM P/E of roughly 130x remains significantly higher than PANW’s 75x, suggesting the market prices more future upside into CrowdStrike despite the near-term expectations gap.

Zscaler (ZS) is the other important peer to monitor. Zscaler recently warned that quarterly revenue would miss estimates as competition intensified. That guidance miss highlights execution risk across the sector and makes Palo Alto’s raised forecast comparatively stronger. Zscaler competes directly in cloud-delivered network security, where Palo Alto’s Prisma Access platform also operates, so any market-share shift between the two would be meaningful.

Palo Alto’s differentiation lies in platform breadth. Its Cortex, Prisma, and Strata product families address endpoint, cloud, and network security simultaneously. Competitors typically lead with one layer and expand from there. That bundled approach is what drove the platformization strategy and is now showing up as revenue acceleration as consolidation contracts mature.

Margins are the clearest near-term differentiator. Palo Alto’s adjusted operating margins are expanding as platformization discounts roll off and full-priced contracts replace them. Neither CrowdStrike nor Zscaler can point to the same margin inflection with the same clarity right now.

Read our full take on Palo Alto’s rally, AI momentum, and next catalysts >>>

What’s Driving PANW Stock Going Forward?

Fiscal Q4 results, expected around August 17, are the most important near-term catalyst. Investors will watch whether the raised full-year forecast proves conservative. Any upward revision to fiscal 2027 guidance would likely extend the stock’s momentum and push shares toward the prior 52-week high of $303.

The Sovereign Cortex launch with Deutsche Telekom addresses a specific and growing market. Regulated European industries, including banking, insurance, and defense agencies, cannot use US-hosted cloud security infrastructure due to data sovereignty laws. If Sovereign Cortex gains traction, it opens a revenue channel that most US-only cybersecurity vendors cannot easily replicate.

Project Lightwell’s expansion with IBM and Red Hat adds agentic AI security capabilities. AI agents are autonomous software programs that execute multi-step tasks without human input. They create new attack surfaces that traditional security tools were not designed to address, and Palo Alto is positioning itself as the category leader in securing those environments.

The broader demand environment is supportive. Verizon’s annual Data Breach Investigations Report found that vulnerability exploitation became the top breach entry point, representing 31% of all incidents. That shift plays directly into Palo Alto’s AI-powered threat detection capabilities and is the demand tailwind management has been pointing to as justification for the entire platformization investment cycle.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Palo Alto Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PANW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PANW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze PANW stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!