Key Takeaways for Micron Stock

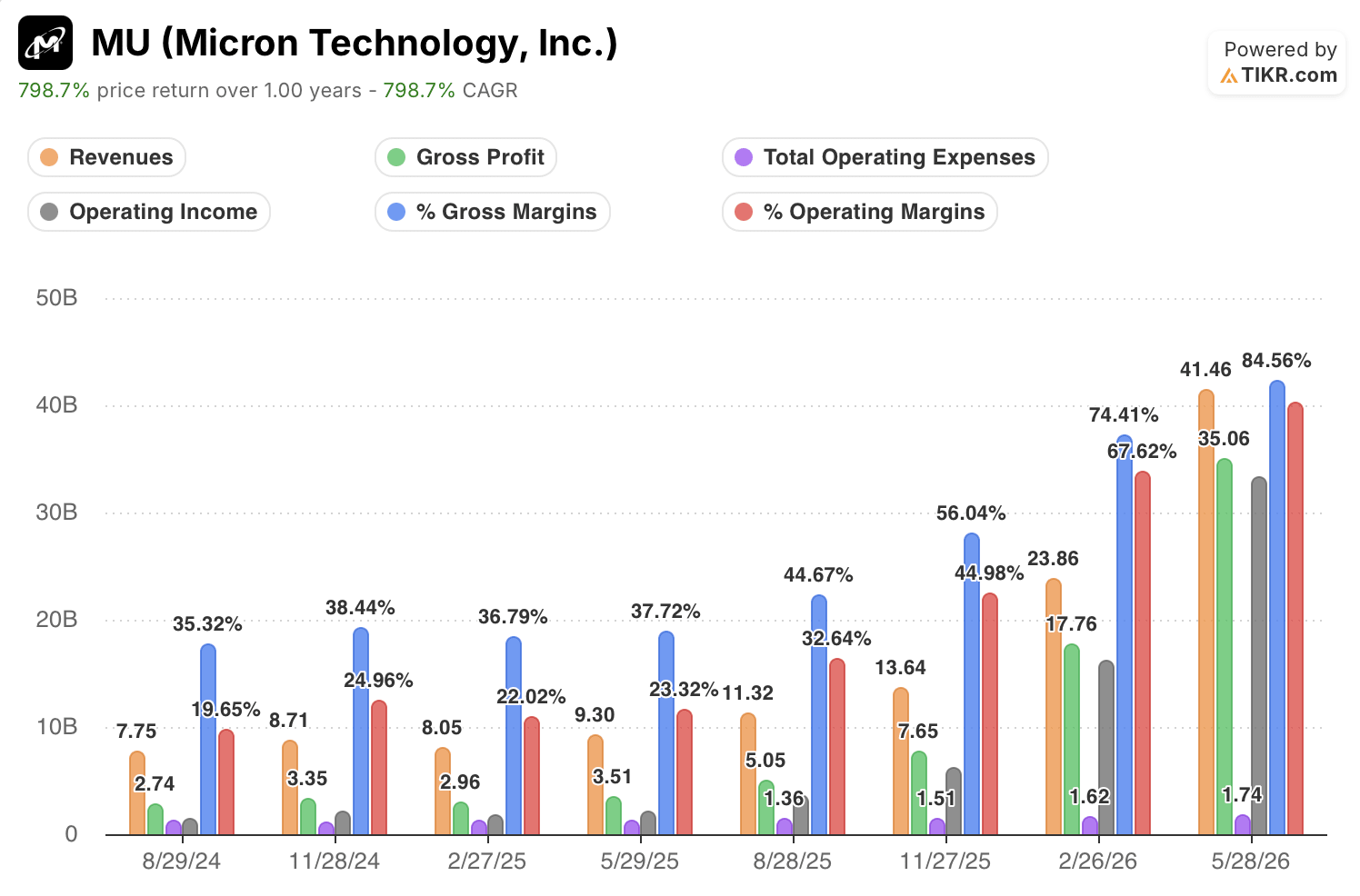

- Revenue reached $41.46 billion in Q3 FY2026, a 346% increase year-over-year.

- Gross margins expanded to 85% in Q3 FY2026, up from 45% in Q3 FY2025.

- Operating income hit $33.32 billion in Q3 FY2026, with operating margins reaching 80%.

Micron’s 346% Revenue Surge Locked In by $22 Billion in Customer Commitments

Micron Technology (MU) posted fiscal Q3 2026 revenue of $41.46 billion, a 346% increase year-over-year driven by record AI memory demand and a structural supply shortage that management says shows no sign of easing.

Micron designs, develops, and manufactures memory and storage products, including DRAM (dynamic random-access memory, the short-term memory inside servers and devices), NAND flash storage, and HBM (High Bandwidth Memory, the high-speed memory stacked directly alongside AI processors).

The headline number (quadruple the revenue of a year ago) tells only part of the story.

Micron’s CFO Mark Murphy disclosed that the company has signed 16 strategic customer agreements (SCAs), non-cancelable, take-or-pay contracts that obligate buyers to purchase fixed volumes at agreed prices regardless of market conditions.

These agreements carry a combined $22 billion in upfront customer cash deposits and financial commitments, giving Micron visibility into demand far beyond typical quarterly guidance.

Chief Business Officer Sumit Sadana told analysts that even with these agreements, committed volumes are still below what customers actually want to sign up for.

As Sadana put it in Q3 earnings call: “the asks from our customers for volume, not just in ’27, but…even going beyond 2027 into 2028…we are able to get very high confidence demand from our customers that is far in excess of our ability to support using our supply.”

The company also disclosed that the HBM addressable market (HBM TAM) is now expected to cross $100 billion as early as 2027 — one full year ahead of prior guidance.

Gross Profit Compounding at 85%: When Revenue Quadruples But Costs Barely Move

Micron’s gross margin reached 85% in Q3 FY2026, up from 45% a year earlier — a 40-point expansion driven by pricing power that the income statement now proves is structural, not cyclical.

Revenue grew 346% year-over-year to $41.46 billion while cost of goods sold rose only to $6.40 billion, essentially flat from the $6.26 billion posted in Q3 FY2025.

That is the mechanism: Micron quadrupled its topline on nearly unchanged production costs, compressing unit cost as a percentage of revenue from 67% to 15%.

Gross profit grew from $5.05 billion to $35.06 billion which is a 899% increase.

Operating expenses (SG&A and R&D combined) totaled $1.74 billion, almost unchanged across the past six quarters, generating extreme operating leverage as revenue scaled.

Operating income jumped from $3.69 billion to $33.32 billion, and operating margins expanded from 33% in Q3 FY2025 to 80% in Q3 FY2026.

The gap between gross margin and operating margin is now just 5 percentage points — meaning Micron retains the vast majority of its pricing gains as operating profit.

Micron Leads WDC and SNDK on Gross Margins by 34 Points and the Gap Is Widening

Micron’s 85% gross margin in the most recent quarter stands 34 points above Western Digital’s (WDC) 50% reading from the same period.

SanDisk (SNDK) posted 79% in the prior quarter, closing some of the historical gap, but Micron has held the lead in every period shown across the two-year comparison.

The divergence is most visible starting in Q3 FY2025, when Micron’s gross margin reached 41% while SanDisk sat at 26% and Western Digital matched Micron at 41%.

From that trough, Micron’s margin expanded by 44 points to reach 85%, while Western Digital expanded by only 9 points to reach 50%.

SanDisk’s trajectory is steeper than Western Digital’s, moving from 26% to 79% over the same span, but still trails Micron by 6 points as of the most recent data.

The structural explanation sits in the transcript: Micron’s non-cancelable take-or-pay contracts allow it to price above spot market conditions, a mechanism neither Western Digital nor SanDisk has publicly replicated at scale.

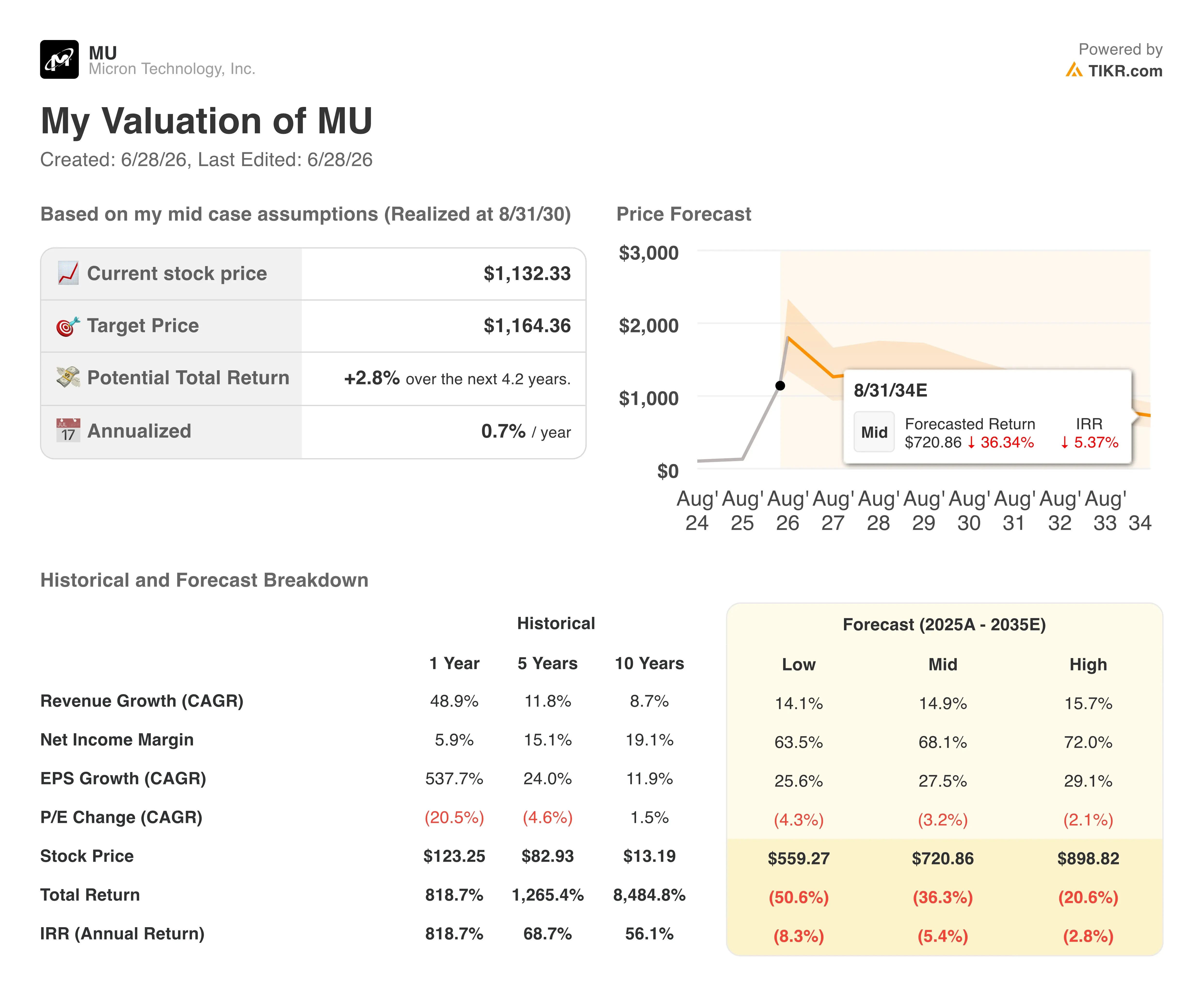

TIKR’s $1,164 Target on MU Stock Holds One Condition: Margins Must Stay Structural

TIKR’s model values Micron at approximately $1,164 by August 2030, implying around 3% total return from the current price of $1,132, or roughly 1% per year.

The model’s conservatism reflects a real tension: current margins are at levels the memory industry has never sustained across a full cycle, and the realization date is more than four years out.

What has to hold is the same mechanism the income statement already proved in Q3 FY2026: non-cancelable take-or-pay SCAs that lock customers into volume commitments, preventing the demand collapse that has historically ended memory margin cycles.

Should You Invest in Micron Technology, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron Technology, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron Technology, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MU stock on TIKR for Free →