Key Stats for VZ Stock

- Past week’s performance: 2.6%

- 52-week range: $38 to $52

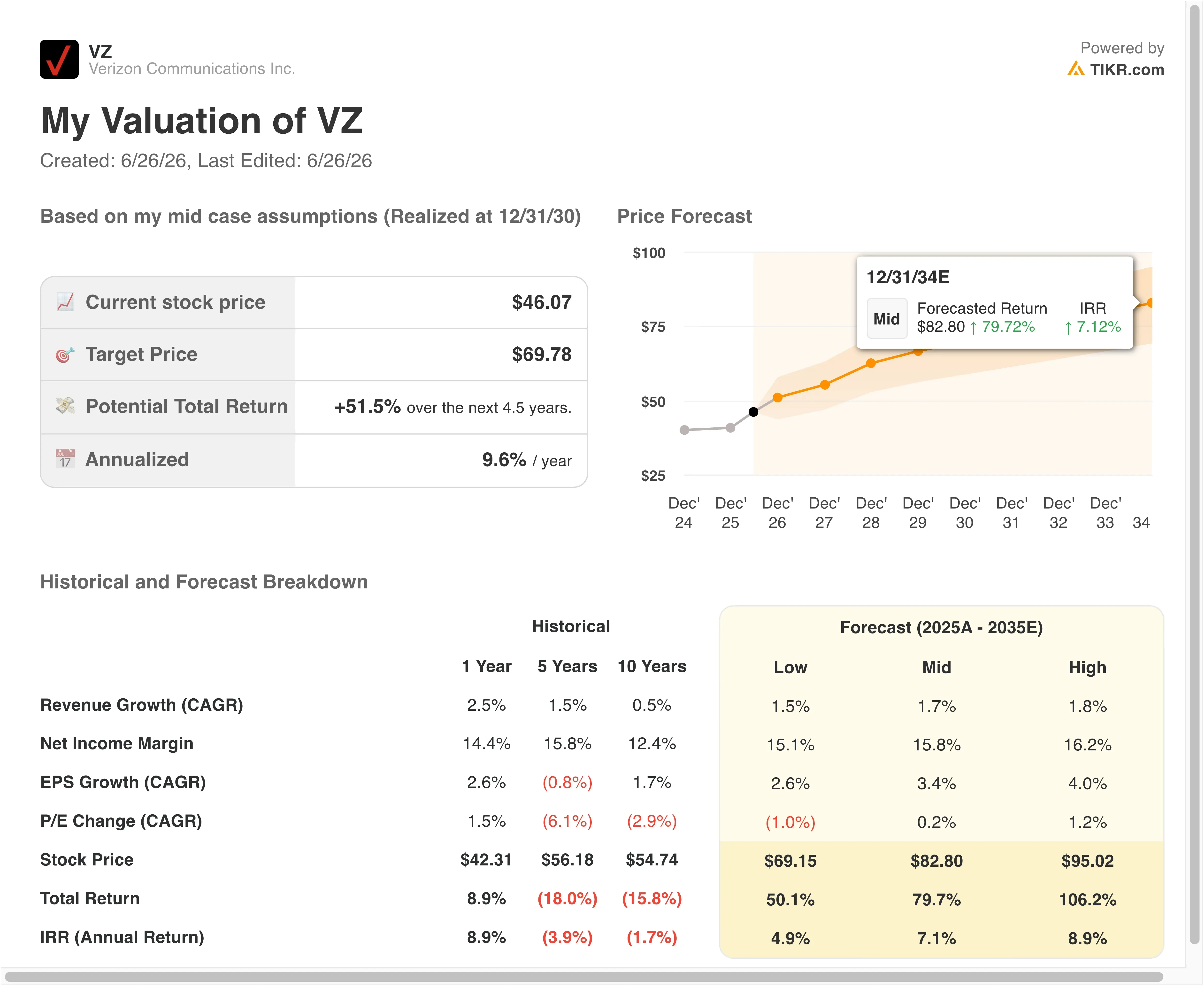

- Valuation model target price: $60

- Implied upside: +32.2% over the next 2.5 years

A Quiet Giant Gets Noisy Headlines

Verizon Communications (VZ) has spent most of 2026 rebuilding investor confidence after years of subscriber concerns and heavy debt. But two headlines arrived close together this week that forced a fresh look at the stock. On June 24, Reuters reported that Alphabet will replace Verizon in the Dow Jones Industrial Average, a widely followed index of 30 major US companies. Then, on June 26, Reuters reported that SpaceX is pushing Starlink’s mobile service directly into the US consumer wireless market.

Neither development changes Verizon’s business overnight. But both landed on a stock already trading below its 52-week high and reinforced the market’s persistent concern: can a traditional carrier hold its ground as technology continues to erode the edges of its network?

Verizon’s most recent fundamentals were actually encouraging. The company beat first-quarter adjusted EPS at $1.28 versus the $1.20 consensus estimate and raised its full-year profit forecast. Revenue climbed 2.9% in Q1 to $34.4 billion. Most importantly, Verizon added 55,000 postpaid phone net subscribers in Q1, the first positive first-quarter result on that metric since 2013. CEO Dan Schulman said, “Our first-quarter 2026 results show that our turnaround is not only progressing, but it is also gaining momentum.”

On June 16, Verizon simplified its wireless plan lineup and dropped certain fees. That move is a competitive response, but it also creates revenue risk: simpler plans can drive subscriber growth while compressing average revenue per user if customers trade down. If VZ stock is to recover toward prior highs, the Q2 results scheduled for July 21 will need to show that subscriber momentum continued without material ARPU deterioration.

See analysts’ growth forecasts and price targets for VZ (It’s free) >>>

Is Verizon’s Dividend Yield Enough to Make the Stock Attractive?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 2.1%

- Operating Margins: 24.4%

- Exit P/E Multiple: 8.8x

Based on these inputs, the model estimates a target price of $60, implying 32.2% total upside and an 11.7% annualized return over the next 2.5 years.

An 11.7% annualized return with a 6.2% current dividend yield is the right frame for this story. Verizon is not a growth stock. But a total return of roughly 32% over 2.5 years, combining capital appreciation with income, is a meaningful proposition for investors who prioritize yield and downside protection.

A dividend history and free cash flow per share chart covering the past five years is the most useful visual here. It shows whether the dividend is well-covered, whether payout has grown consistently, and whether cash generation supports the debt-reduction plan that underpins the investment thesis.

Revenue growing at 2.1% annually is modestly below Verizon’s one-year historical rate of 2.5%. It also reflects ongoing uncertainty about whether fiber network expansion adds net-new revenue or simply offsets declining legacy wireline volumes. Operating margins expanding to 24.4% from the current LTM level of 23.3% requires modest but meaningful cost efficiency improvement as network integration matures.

The exit P/E of 8.8x matches Verizon’s own five-year historical multiple exactly. There is no multiple expansion assumption in this model. Investors are paying for cash flows and dividends at a traditional telecom multiple, which is the most conservative way to frame the stock.

See how Verizon’s dividend coverage compares to AT&T and T-Mobile on TIKR >>>

Verizon vs. AT&T and T-Mobile in a Changing Wireless Market

AT&T (T) is the clearest peer on the dividend and debt-reduction narrative. AT&T has been executing its own cost-cutting and debt-paydown plan and trades at a similarly low single-digit revenue multiple. Both companies generate meaningful free cash flow, but neither is growing revenue fast enough to attract growth-oriented investors. The primary battleground between the two is wireless postpaid phone net additions, the cleanest measure of competitive health in the consumer market.

T-Mobile (TMUS) is the growth outlier in US wireless. T-Mobile lifted its annual forecast for account additions after strong Q1 results and trades at a meaningfully higher P/E than either AT&T or Verizon. T-Mobile’s network speed advantage and aggressive pricing have consistently taken share from both larger carriers. That share pressure is structural rather than cyclical, which is why Verizon’s June plan simplification and fee cuts read as a direct competitive response.

The Starlink threat adds a new variable. SpaceX’s reported push into US consumer mobile service could create a fourth wireless option for rural and suburban customers underserved by traditional carriers. Verizon has some rural network-sharing agreements involving satellite connectivity. But a direct Starlink consumer offering would compete for the same subscriber segments that Verizon and AT&T have been targeting with 5G home internet expansion.

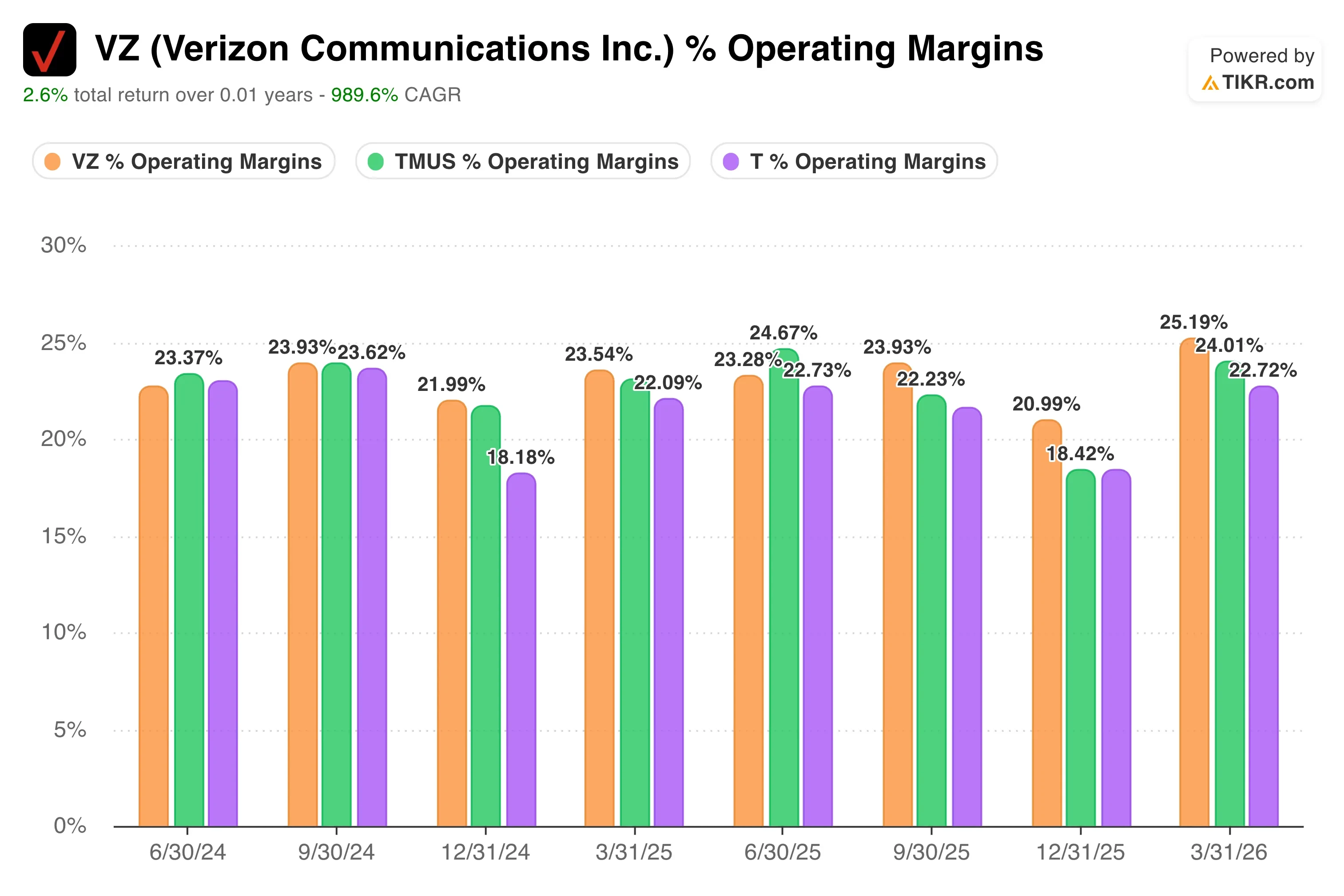

On operating margins, Verizon’s LTM EBIT margin of 25% is stable and competitive relative to its wireline peers. That margin stability is one of Verizon’s clearest strengths in the current environment, particularly as AT&T navigates higher costs and a more complex balance sheet.

Read our full take on Verizon’s 2026 gains, dividend, and outlook >>>

What’s Driving VZ Stock Going Forward?

The Q2 2026 earnings report, scheduled for July 21, is the most important near-term catalyst. Investors will focus on wireless postpaid net additions. A repeat of Q1’s historic first positive first-quarter result would reinforce the narrative that Verizon’s competitive position has stabilized under CEO Dan Schulman’s strategy.

The Frontier Communications acquisition, which closed on January 20, 2026, is the medium-term growth driver most often cited by management. The Frontier deal added fiber subscribers and significant fiber infrastructure in key markets. Verizon’s ability to sell wireless bundled with fiber broadband to the same household is one of the clearest revenue-per-customer improvement opportunities available right now. As fiber penetration grows in existing markets, it also reduces churn among bundled customers.

Spectrum management matters as well. The FCC approved Verizon’s $1 billion spectrum purchase in May, adding mid-band capacity that supports both 5G broadband and mobile network performance. Spectrum is the radio-frequency bandwidth that wireless networks use to carry data, and additional mid-band capacity supports Verizon’s ability to compete with T-Mobile on network speed in dense urban markets.

Debt reduction remains the clearest financial priority. Verizon carries approximately $192 billion in total net debt and has been actively managing its debt maturity profile through exchange offers and redemptions throughout 2026. Every incremental reduction in interest expense flows directly to free cash flow, which funds both the quarterly dividend and incremental network investment.

The dividend of $0.7075 per share for the July 10 payment yields 6.2% at current prices and remains the primary reason income investors hold the stock through periods of market noise like this week’s Dow removal.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Verizon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VZ, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VZ alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze VZ stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!