Walgreens Boots Alliance (NASDAQ: WBA) has been under pressure for years. Revenue growth has slowed, margins remain thin, and the stock trades near $12/share after a long multiyear decline. Persistent reimbursement pressure and softer retail traffic continue to weigh on results, raising concerns about how quickly the company can stabilize.

Recently, Walgreens made changes that caught investor attention. The company accelerated its cost reduction program and highlighted early signs that the savings are beginning to show up in results. Management also appointed a new CEO with deep healthcare experience, signaling a more focused approach to long-term strategy and operational discipline. These shifts suggest Walgreens is taking more proactive steps to rebuild profitability.

This article explores where analysts think Walgreens could trade by 2027. We combined consensus targets with TIKR’s valuation model to outline the stock’s potential path based on current expectations. These figures reflect analyst estimates and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Flat Performance

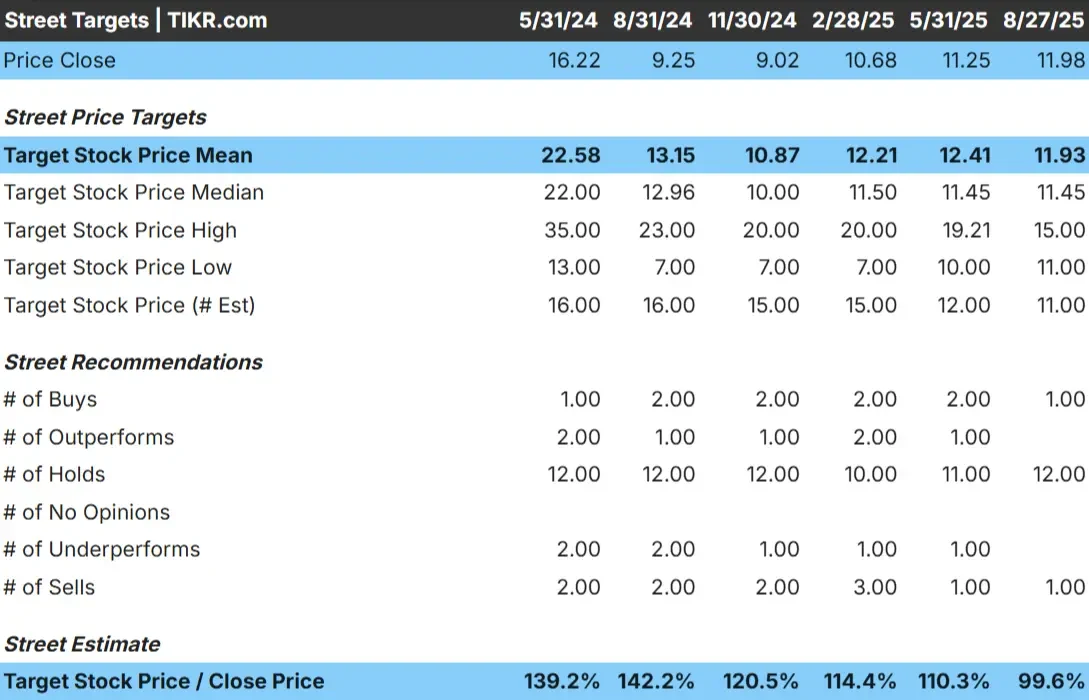

Walgreens trades near $12/share today. The average analyst price target is also $12/share, which implies essentially no upside from current levels. The forecast range is tight and shows limited disagreement among analysts.

- High estimate: $15/share

- Low estimate: $11/share

- Median target: $11/share

- Ratings: 1 Buy, 12 Holds, 1 Sell

For investors, the lack of upside suggests the stock may already reflect today’s fundamentals. Expectations remain cautious, and analysts appear to be waiting for clear signs of a turnaround before raising targets. Without meaningful improvement in margins or earnings visibility, the stock is likely to remain range bound.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Walgreens: Growth Outlook and Valuation

The company’s fundamentals appear steady, but not particularly strong:

- Revenue is projected to grow 1.9% through 2027

- Operating margins are expected to remain near 1.4%

- Shares trade at 6.7x forward earnings

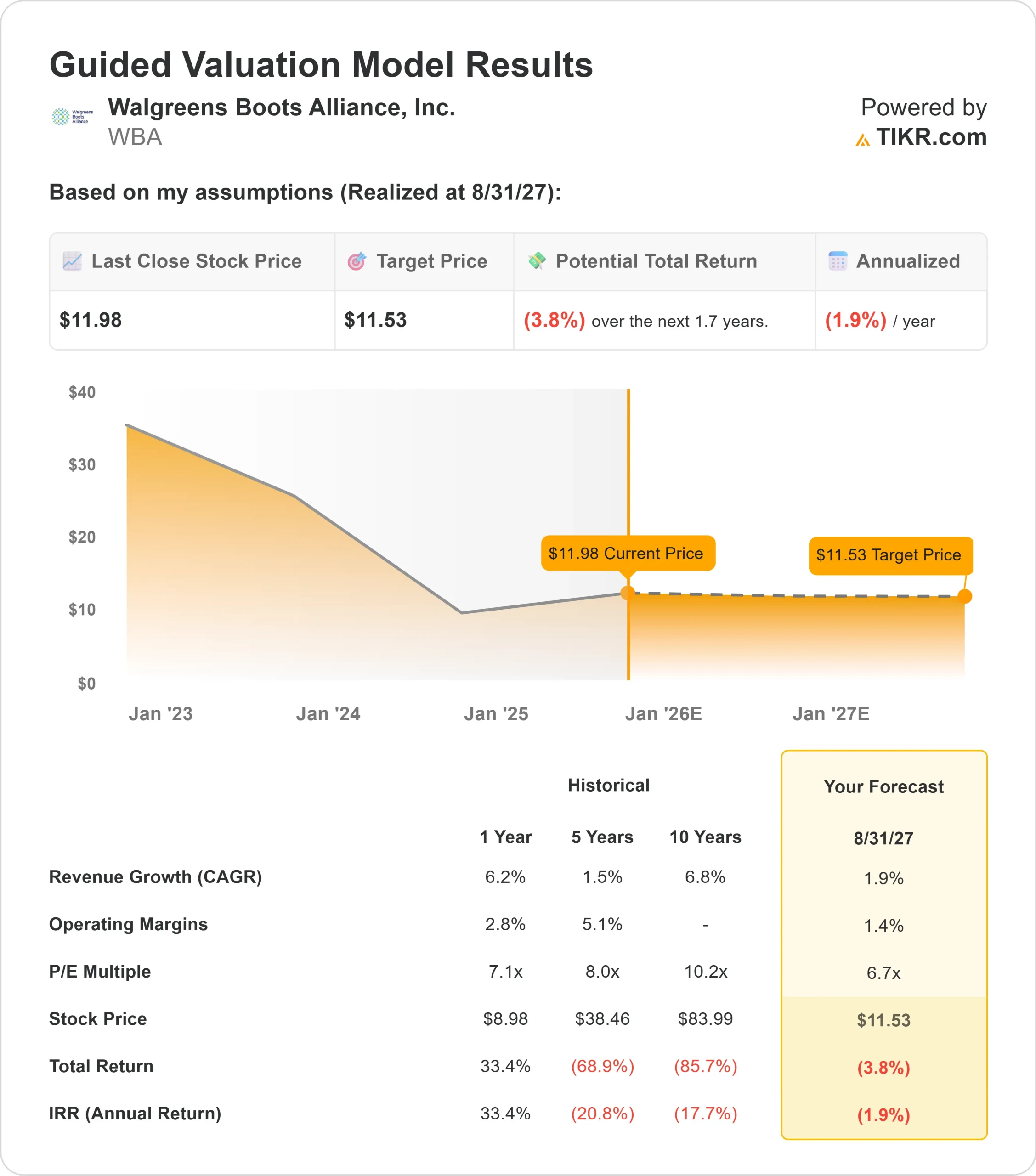

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 6.7x forward P E suggests about $12/share by 2027

- That implies a total return of about negative 4%, or roughly negative 2% annualized

These numbers suggest Walgreens is stabilizing, but not yet rebuilding meaningful earnings power. Growth is modest, profitability is thin, and valuation reflects uncertainty around long-term improvement. The stock looks inexpensive, but the low multiple alone is not enough without a clearer path to stronger performance.

For investors, Walgreens resembles more of a hold than a growth story. Returns are likely to stay limited unless management can deliver consistent margin recovery and rebuild the company’s long-term earnings trajectory.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Despite its challenges, Walgreens has taken steps that could support a gradual recovery. The company is executing deeper cost reductions, and management has already noted early financial benefits. Refocusing on core pharmacy operations and scaling back underperforming ventures has also helped reduce volatility and create a clearer strategic direction.

Leadership changes are also encouraging. The new CEO brings a more healthcare-centric approach and has emphasized disciplined execution and profitability. Investors view this as a constructive shift for a business that needs sharper focus and more consistent operating results.

While these actions do not guarantee a turnaround, they show that Walgreens is laying the groundwork for better stability. For investors, this creates a more balanced setup than in recent years, even if expectations remain low.

Bear Case: Structural and Competitive Pressure

Walgreens still faces meaningful obstacles. Pharmacy reimbursement pressure is intense, retail traffic has been inconsistent, and operating margins near 1% highlight how fragile the business remains. Rising labor and operating costs continue to challenge profitability.

Competition is another concern. CVS is expanding further into healthcare services, Amazon and online pharmacies continue to push into prescription fulfillment, and discount retailers are drawing cost-conscious shoppers. These forces make it difficult for Walgreens to regain share or meaningfully expand margins.

For investors, the bear case emphasizes slow progress rather than severe downside. The risk is that Walgreens may spend several years rebuilding profitability without generating material shareholder returns.

Outlook for 2027: What Could Walgreens Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests Walgreens could trade near $12/share by 2027. That represents a total return of about negative 4%, or roughly negative 2% annualized.

This outlook reflects a cautious stance and assumes no major improvement in margins or revenue growth. For Walgreens to deliver better returns, the company would need to show consistent progress in rebuilding earnings, improving pharmacy economics, and managing costs more effectively.

For investors, Walgreens appears to be a steady but limited story. The company is unlikely to deliver strong upside unless management exceeds today’s cautious expectations and restores durable earnings momentum.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>