Paylocity Holding Corporation (NASDAQ: PCTY) has been under pressure over the past year. Growth has slowed, margins have eased, and sentiment across payroll and HCM software has softened. The stock trades near $147/share, well below its recent highs. Even with these challenges, Paylocity’s recurring revenue base and strong profitability continue to provide a solid foundation for long-term performance.

Recently, Paylocity delivered results that showed meaningful stabilization. Revenue growth held in the high single digits, operating margins remained strong, and customer retention stayed healthy. Management also introduced new automation and analytics enhancements aimed at reducing HR workload and improving the overall workflow experience. These improvements reinforce Paylocity’s position in a competitive market and highlight its continued focus on product innovation.

This article explores where Wall Street analysts believe Paylocity could trade by 2028. We pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

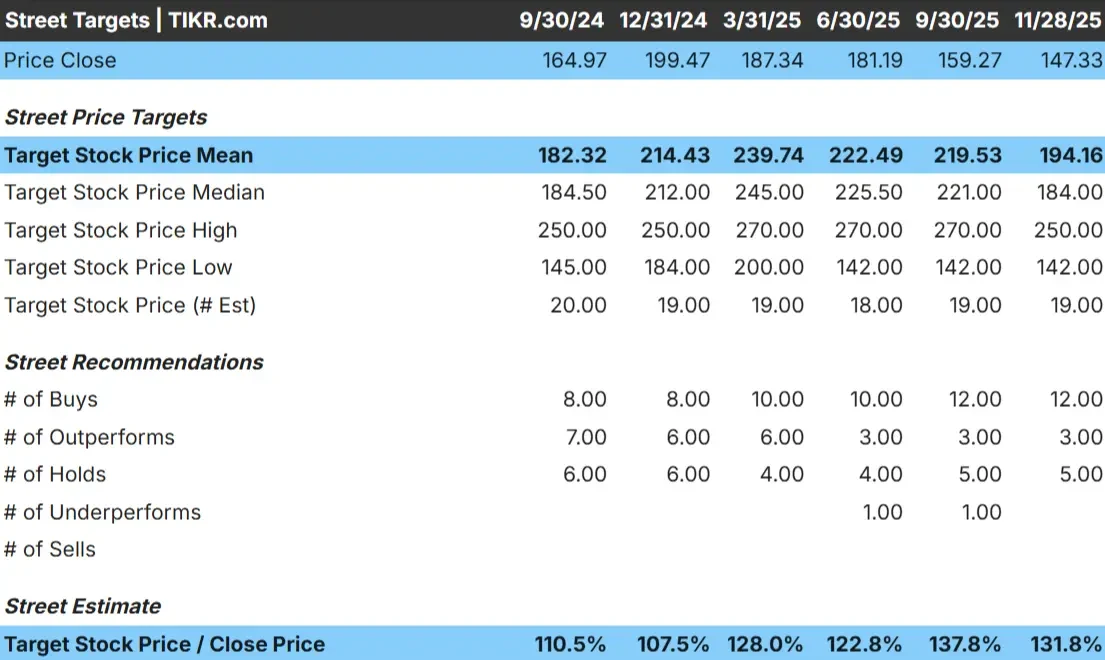

Paylocity trades around $147/share today. The average analyst price target is $194/share, which points to roughly 32% upside. This qualifies as meaningful upside and signals constructive sentiment from the analyst community.

- High estimate: $250/share

- Low estimate: $142/share

- Median target: $184/share

- Ratings: 12 Buys, 3 Outperforms, 5 Holds

The target range is relatively tight, which suggests analysts are aligned on a steady recovery outlook. For investors, this indicates that expected gains are grounded in balanced fundamentals rather than aggressive or overly optimistic assumptions. If execution remains consistent and sentiment strengthens in cloud payroll software, Paylocity has room to outperform the midpoint of these estimates.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Paylocity: Growth Outlook and Valuation

The company’s fundamentals appear steady and supported by recurring revenue and disciplined cost management.

- Revenue growth forecast: 9.3%

- Operating margin forecast: 31.1%

- Forward P E used: 19.7x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19.7x forward P E suggests about $196/share by mid 2028

- That implies roughly 33% total returns, or about 11.7% annualized

These inputs point to a consistent compounding profile, driven more by earnings expansion than a major rerating. Paylocity is valued more reasonably today than in past high-growth periods, which means expected returns are tied closely to its operating execution.

For investors, Paylocity looks like a steady software compounder rather than a high-volatility growth story. Returns will likely follow fundamentals, making the stock appealing for those who prefer predictable performance over aggressive upside swings.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Paylocity benefits from a strong recurring revenue base and increasing adoption of its HR and payroll modules. Customers often expand usage over time, which improves engagement and strengthens long-term retention. The company has also been focusing on automation and workflow improvements that make HR tasks easier, reduce manual processes, and enhance overall user experience. These enhancements deepen customer satisfaction and increase the appeal of the platform.

For investors, the optimism comes from Paylocity’s ability to maintain stable fundamentals even as the broader software market cools. Its product execution and ongoing platform improvements suggest the company has the tools to support consistent earnings growth over the coming years.

Bear Case: Slower Growth and Competitive Pressure

The biggest challenge for Paylocity is a slower growth environment. Demand from small and mid-sized businesses can be uneven, and the company faces a competitive landscape with large incumbents and newer cloud-first providers. If customers delay upgrades or hiring remains sluggish, revenue growth could remain below historical levels.

For investors, the bear case centers on the possibility that Paylocity maintains strong profitability but does not accelerate growth enough to justify a meaningfully higher valuation. A competitive industry backdrop and uncertain macro conditions could limit how much the stock rerates over the near term.

Outlook for 2028: What Could Paylocity Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19.7x forward P E suggests Paylocity could trade near $196/share by mid 2028. That represents roughly 33% total return, or about 11.7% annualized.

While this would be a healthy recovery, it already assumes stable execution and consistent margins. To deliver stronger upside, Paylocity would need improving SMB hiring trends, faster adoption of additional modules, or a clear competitive advantage that lifts growth above current expectations. Without those catalysts, investors should expect solid but controlled returns.

For investors, Paylocity appears to be a reliable long-term software compounder supported by recurring revenue and efficient operating leverage. The base case suggests meaningful and achievable upside, with the potential for further gains if the company outperforms today’s moderate outlook.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>