Automatic Data Processing (ADP) has been under pressure over the past year. Revenue growth has slowed, sentiment has softened, and payroll and HCM software names have cooled off. The stock trades near $255/share, reflecting concerns about demand trends and the broader macro environment. Even so, ADP remains one of the most established and consistent compounders in the industry.

Recently, ADP posted steadier results that helped restore confidence. The company maintained strong profitability, float income held up better than expected, and client retention and bookings improved. ADP also expanded its automation and AI driven features, reinforcing its position as a mission critical platform for businesses. These developments suggest ADP is still capable of delivering stable performance even as it works through a slower environment.

This article explores where Wall Street analysts think ADP could trade by 2028. We have pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

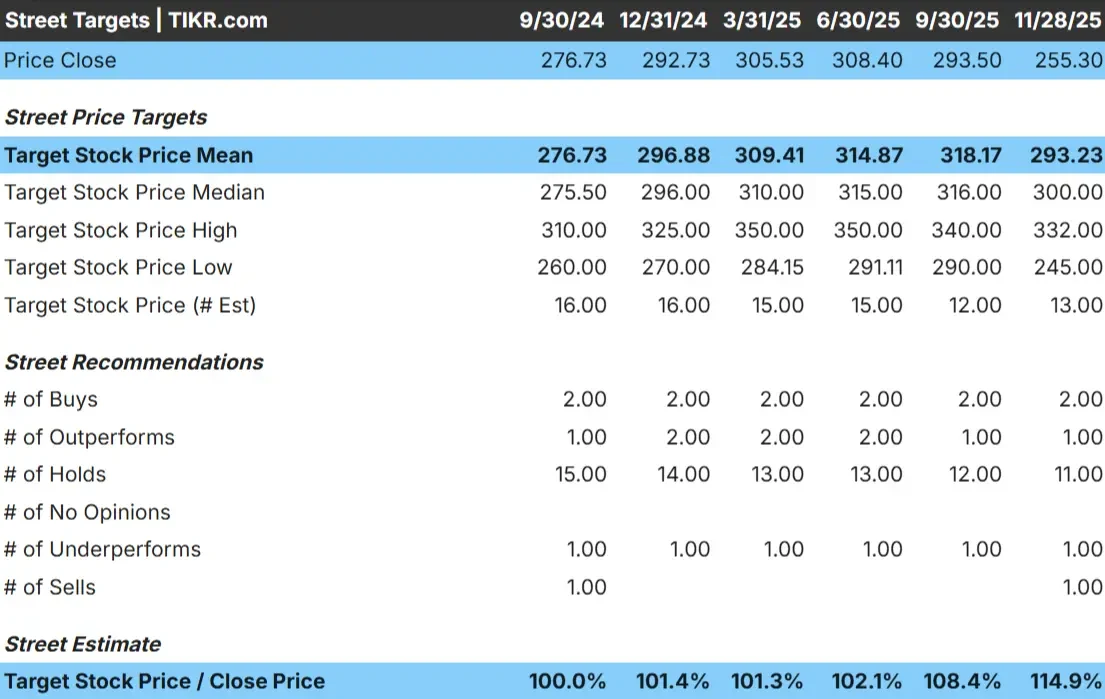

ADP trades near $255/share today. The average analyst price target is $293/share, which points to about 15% upside. This puts the stock in the modest upside category, suggesting that ADP could outperform slightly if earnings stay consistent or if labor market trends remain stable.

Here is the latest breakdown:

- High estimate: ~$332/share

- Low estimate: ~$245/share

- Median target: ~$300/share

- Ratings: 2 Buys, 1 Outperform, 11 Holds, 1 Underperform, 1 Sell

The tight range of forecasts shows that analysts generally agree on ADP’s near term outlook. For investors, this reflects a steady profile where most movement is likely to follow earnings rather than major sentiment shifts. The setup favors investors who prefer stability and predictable compounding.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

ADP Growth Outlook and Valuation

The company’s fundamentals appear stable and support a consistent long term outlook:

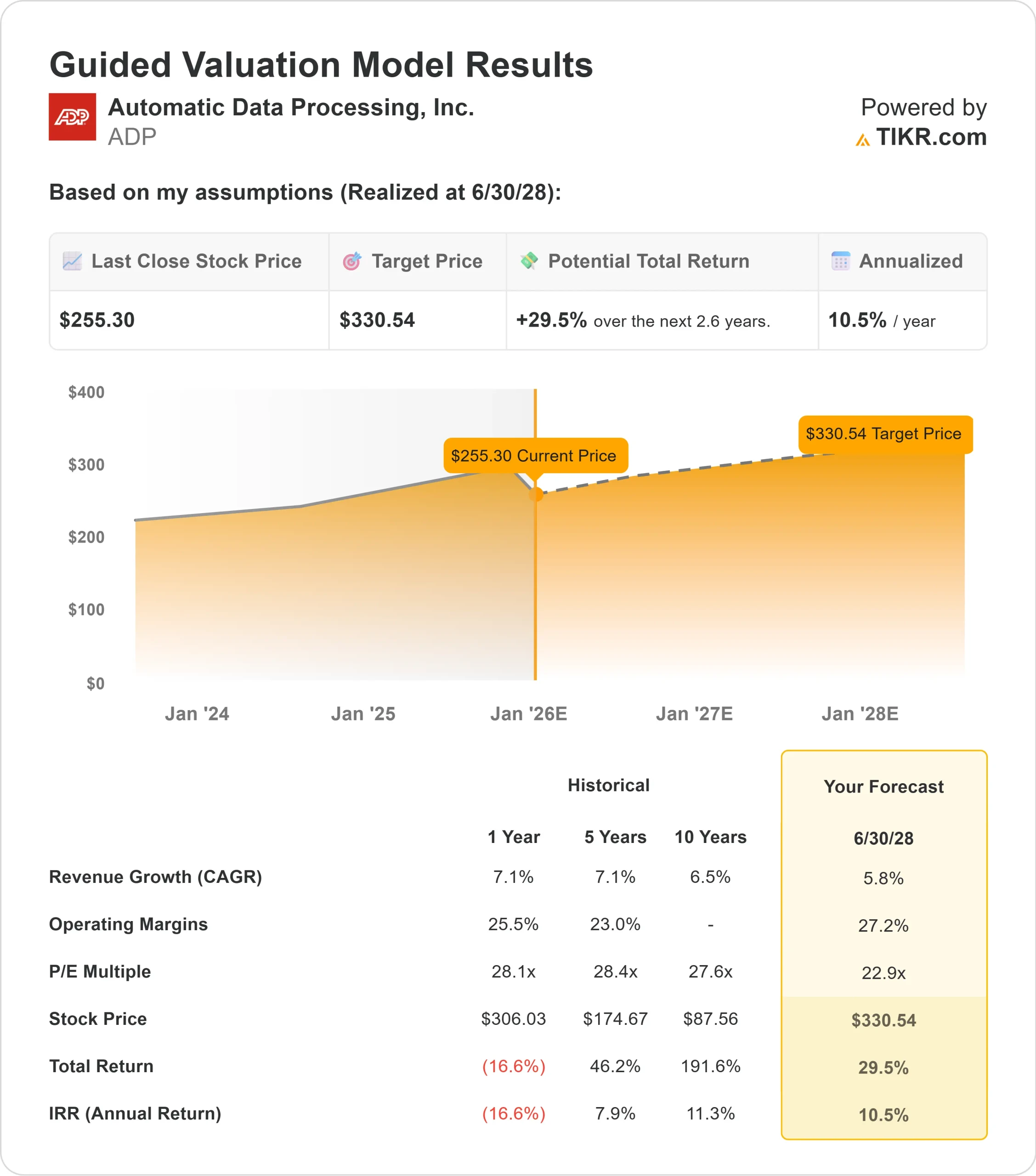

- Revenue is projected to grow 5.8%

- Operating margins are expected to reach about 27.2%

- Shares trade at roughly 23x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22.9x forward P E suggests about $331/share by mid 2028

- That implies 29.5% total upside, or around 10.5% annualized returns

These numbers indicate that ADP can continue compounding steadily, supported by strong margins, recurring revenue, and a business model that holds up well through different market cycles. Most of the expected returns come from consistent earnings growth rather than changes in valuation.

For investors, ADP looks like a dependable compounder rather than a high growth story. Its stability, predictable cash flows, and high client retention create a strong foundation for long term performance.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

ADP remains one of the most resilient companies in payroll and HR technology. Its services are mission critical for businesses, retention is high, and its recurring revenue base leads to predictable performance. The company continues enhancing its platform with automation and AI driven tools that help clients manage payroll, compliance, and workforce operations more efficiently.

These strengths give investors confidence that ADP can maintain stable growth even when economic conditions soften. The business is built for steady compounding rather than dramatic swings, which makes it appealing to long term investors.

Bear Case: Slower Growth and a Premium Multiple

The primary concern for ADP is a slowdown in revenue growth. Expectations call for only moderate expansion, which may not fully justify the stock’s premium valuation. If hiring slows, wage growth weakens, or float income declines, ADP’s earnings could come under pressure.

Competition is another factor to watch. Companies like Paychex, Workday, and UKG continue to invest in next generation HCM tools. As the landscape becomes more competitive, pricing power and customer acquisition may become more challenging. For investors, the risk is not business deterioration but the possibility that the market becomes less willing to support a premium multiple for slower growth.

Outlook for 2028: What Could ADP Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22.9x forward P E suggests ADP could trade near $331/share by 2028. From today’s price of about $255/share, this represents roughly 30% total upside, or around 10.5% annualized returns.

While this is a healthy return profile, it already assumes solid execution and a stable labor market. Faster revenue growth, stronger operating leverage, or a favorable rate environment would be needed to unlock additional upside.

For investors, ADP stands out as a dependable long term holding. Its consistent margins, recurring revenue base, and mission critical services create a strong backdrop for steady compounding. The potential for outsized gains depends on management outperforming expectations and continued adoption of ADP’s automation and digital tools.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>