CVS Health Corporation (NYSE: CVS) has been working through a challenging period marked by margin pressure, rising medical costs and slower growth in parts of its healthcare services segment. The stock now trades near $80/share after rebounding from last year’s lows. Even with ongoing volatility, CVS remains a major presence across pharmacy, insurance and retail, which keeps analysts cautiously optimistic.

Recently, CVS reported steadier operating trends. Management highlighted improving medical cost patterns in its insurance division, while stronger cash flow supported continued debt reduction. The company also accelerated store modernization and expanded its digital pharmacy tools to improve customer engagement and long term profitability. These developments suggest that CVS is capable of rebuilding momentum even as it navigates a competitive healthcare landscape.

This article looks at where Wall Street analysts believe CVS could trade by 2027. These figures reflect current analyst expectations and are not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

CVS trades around $80/share today. Analysts place the average price target at $91/share, which points to about 13% upside. The spread of estimates shows a balanced but cautious outlook:

- High estimate: ~$102/share

- Low estimate: ~$77/share

- Median target: ~$93/share

- Ratings: 17 Buys, 6 Outperforms, 5 Holds

This falls into the modest upside category. Analysts see room for gains, but expectations remain measured. For investors, the stock could rise if CVS continues stabilizing margins and strengthening cash flow, although conviction remains moderate until earnings trends improve more consistently.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

CVS: Growth Outlook and Valuation

The company’s fundamentals appear steady, but not especially strong:

- Revenue growth is projected at 5.7% through 2027

- Operating margins are expected to remain near 3.7%

- Shares trade at roughly 9.3x forward earnings

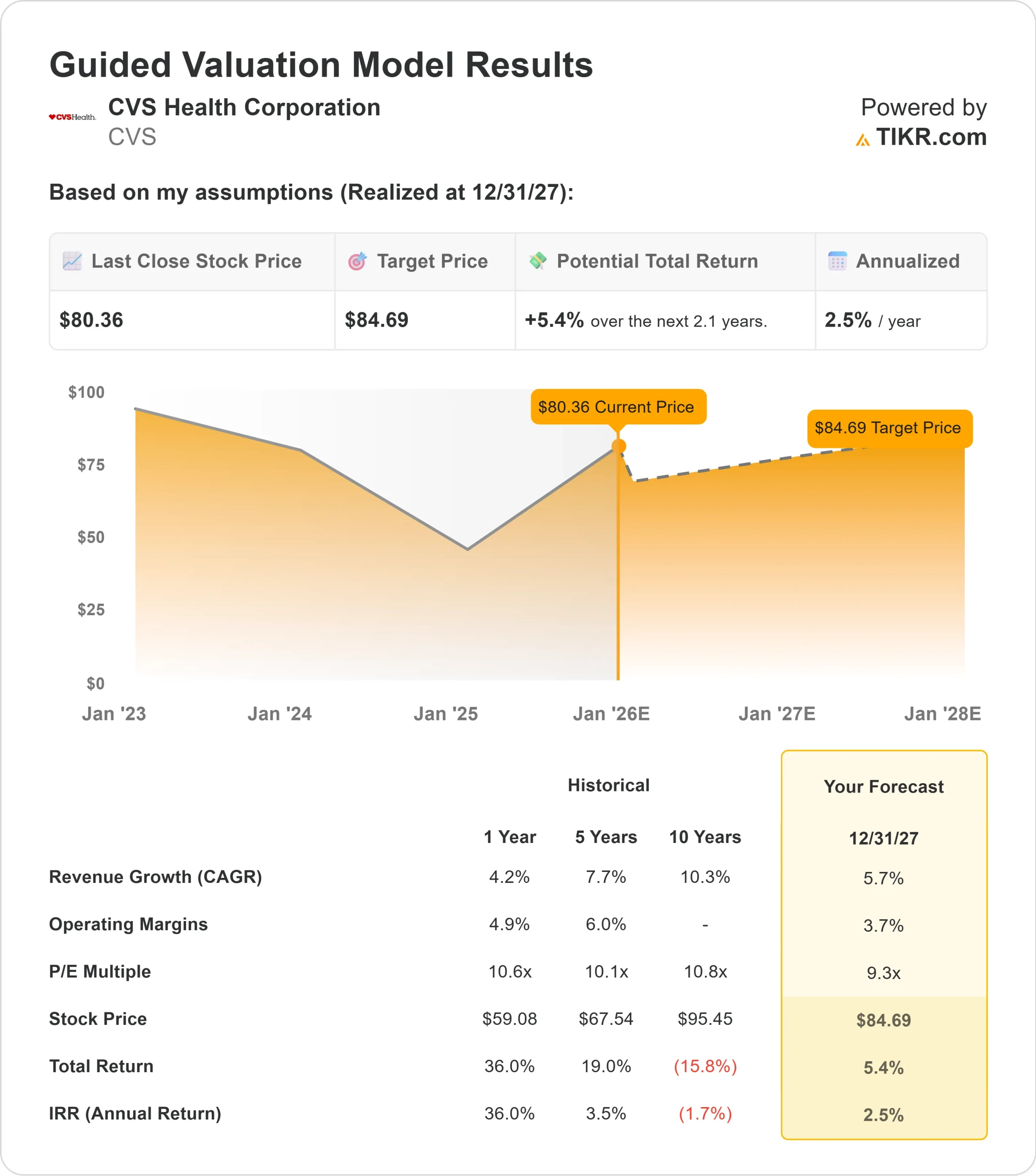

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 9.3x forward P E suggests about $85/share by 2027

- That implies roughly 5% total return, or around 2% annualized

These numbers suggest CVS can deliver stable but moderate performance as earnings gradually rebuild. The valuation is already pricing in much of the expected recovery, which limits near term upside unless margins improve faster than anticipated.

For investors, CVS looks more like a steady healthcare compounder than a high growth story. Returns are likely to track earnings rather than sentiment, making consistency and execution the key drivers to watch.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

CVS continues to benefit from its scale and breadth across pharmacy, insurance and care delivery. Its integrated model supports stable demand and provides multiple revenue streams that help reduce volatility. Recent stabilization in medical cost trends has also lifted sentiment, since this was one of the largest sources of uncertainty.

Management’s focus on debt reduction, operating efficiency and digital improvements is another supportive factor. CVS has been investing in technology, retail modernization and service expansion, all of which strengthen customer relationships and improve competitiveness. For investors, these actions show that the company is building a stronger foundation for long term earnings stability.

Bear Case: Margins and Competitive Pressure

Challenges remain even with recent improvements. Profitability is still below its historical range, and the insurance segment remains sensitive to shifts in medical costs. Retail pharmacy reimbursement pressure continues to weigh on results, making sustained margin improvement difficult.

Competition is also increasing as large retailers, insurers and digital platforms expand into similar services. For investors, the key risk is that CVS may struggle to grow earnings fast enough to move the stock meaningfully higher, especially if margin progress slows or competitive pressures intensify.

Outlook for 2027: What Could CVS Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model using a 9.3x forward P E suggests CVS could trade near $85/share by 2027. That represents a total return of about 5%, or roughly 2% annualized, indicating that expectations are already largely reflected in the current price.

Analyst targets are more optimistic, averaging $91/share, or around 13% upside from current levels. This places CVS in the modest upside category, where gains depend heavily on consistent execution. Stronger medical cost control, more efficient operations and continued improvements across health services would be needed for the stock to outperform expectations.

For investors, CVS appears to offer stable but measured return potential. It remains a reliable long term holding in healthcare, with upside tied to the company’s ability to steadily rebuild margins and strengthen its financial profile.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>