Key Takeaways:

- AI Leadership: Microsoft’s Cloud revenue hit $49 billion in Q1 2026, up 26% year-over-year, driven by massive AI adoption.

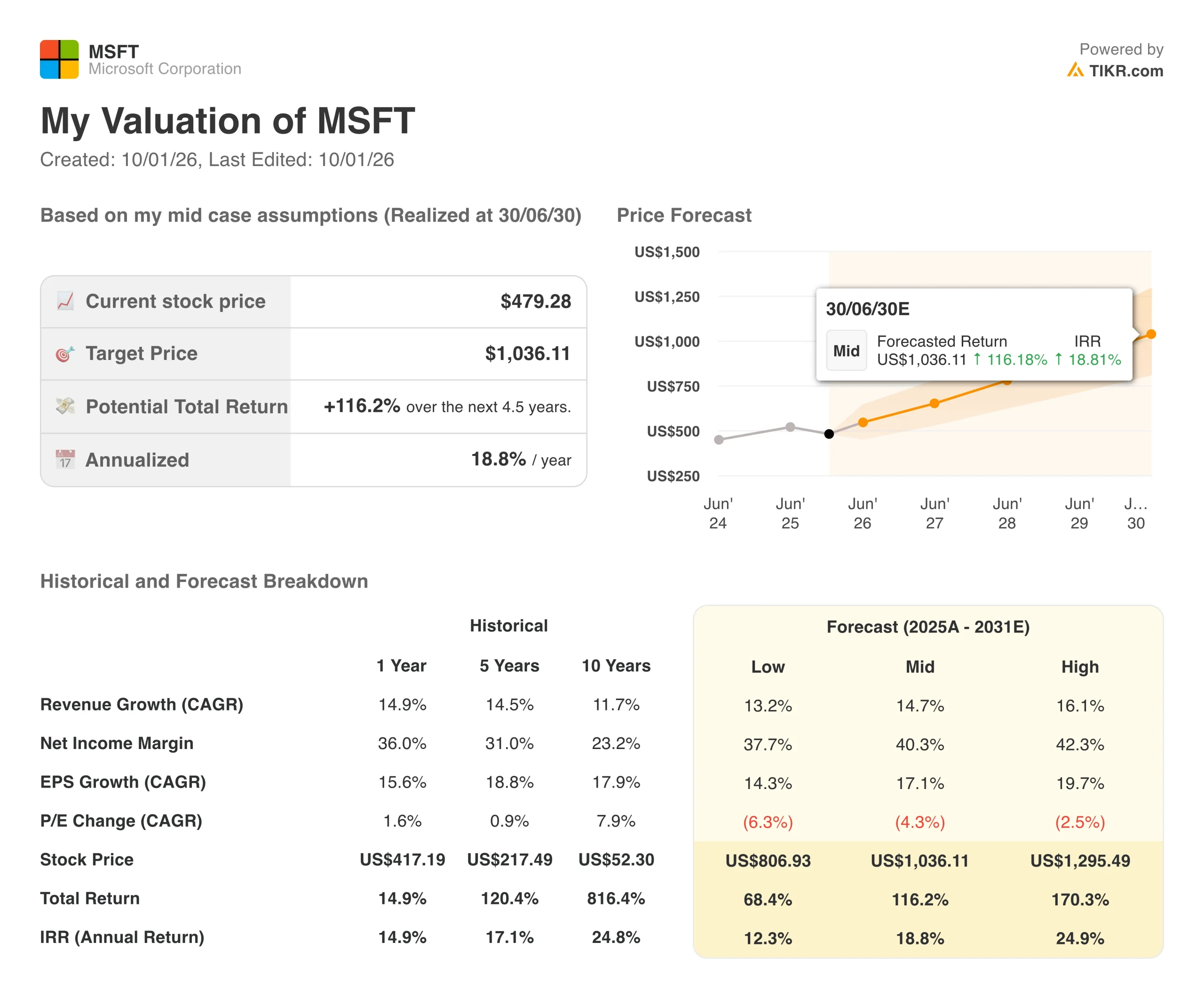

- Price Projection: Based on current momentum, the stock could reach $1,036 by June 2030.

- Potential Gains: This target implies a total return of 116% from the current price of $479.

- Annual Return: Investors could see roughly 19% growth per year over the next 4.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Microsoft (MSFT) isn’t just riding the AI wave—it’s building the infrastructure that powers it. With 90% of Fortune 500 companies now using Microsoft 365 Copilot and commercial bookings surging 112% in Q1 2026, the tech giant has transformed from a software company into an AI platform powerhouse.

The results speak for themselves. Microsoft Cloud revenue topped $49 billion last quarter, growing 26% year-over-year.

Even more impressive, the company’s remaining performance obligations hit nearly $400 billion, up 51% from the prior year. These aren’t just numbers—they represent signed contracts from customers eager to deploy AI at scale.

Despite this momentum, MSFT stock is trading at $479, well below what our analysis suggests it’s worth. This gap creates an opportunity for investors who understand where Microsoft is heading.

See analysts’ full growth forecasts and estimates for MSFT stock (It’s free) >>>

What the Model Says for MSFT Stock

We analyzed Microsoft’s future through the lens of its “AI factory” strategy. By building planet-scale infrastructure and deploying Copilot agents across information work, coding, and security, Microsoft is becoming the essential layer between AI models and enterprise customers.

Using a forecast of 15% annual revenue growth and 47% operating margins, our model projects the stock will rise to $1,036 within 4.5 years. This assumes a 25x Price-to-Earnings (P/E) multiple.

That might seem conservative given Microsoft’s current P/E of 29x. But as the company scales AI infrastructure and matures its Copilot business, some multiple compression is reasonable. The real value comes from sustained earnings growth, not multiple expansion.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MSFT stock:

1. Revenue Growth: 15.6%

Microsoft is successfully moving from license sales to recurring cloud revenue. This shift, combined with AI adoption, drives predictable growth.

Azure Momentum: The cloud platform grew 40% in Q1 2026, even while capacity-constrained. Management expects to remain supply-limited through fiscal 2026.

Copilot Expansion: Daily active users doubled quarter-over-quarter. Large customers like PwC deployed 200,000 seats and credited Microsoft with saving millions of employee hours.

Multi-Product Strategy: Customers using multiple products (M365, Azure, Dynamics, Security) create stickier relationships and higher lifetime value.

2. Operating margins: 46.7%

Microsoft’s margin profile is improving as AI workloads scale, despite massive infrastructure investments.

Efficiency Gains: The company increased token throughput for GPT-4.1 and GPT-5 by over 30% per GPU using software optimization. This means more revenue per dollar of infrastructure.

Smart Capital Allocation: About half of Q1 spending went to short-lived assets (GPUs and CPUs) that match contract durations. The other half funds long-lived data centers with 15+ year useful lives.

First-Party Leverage: Microsoft’s own applications (Copilot, GitHub, Security) run on the same infrastructure as third-party Azure customers. This shared fleet drives higher utilization and margins.

3. Exit P/E Multiple: 25x

The market currently values Microsoft at 29x earnings. We chose 25x for our exit multiple to stay conservative.

Quality Premium: Microsoft deserves a premium to the market average due to its recurring revenue model, margin expansion, and AI leadership position.

Deceleration Factor: As the company matures and revenue growth moderates from current levels, some multiple compression is natural.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Software growth can be volatile. Here is how Microsoft stock might look in different scenarios through 2030:

- Low Case: If revenue growth slows to 13% and margins plateau at 38%, the stock still offers a 12% annual return.

- Mid Case: With 15% growth and 47% margins (our base assumptions), we expect a 19% annual return.

- High Case: If AI adoption accelerates and Microsoft captures 40% margins while growing at 16%, returns could hit 25% annually.

See what analysts think about MSFT stock right now (Free with TIKR) >>>

The range of outcomes reflects different AI adoption curves. In the low case, enterprises adopt AI slowly due to governance concerns or disappointing ROI.

In the high case, agent-based workflows become the new standard for knowledge work, and Microsoft captures most of that value through its platform.

How Much Upside Does Microsoft Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!