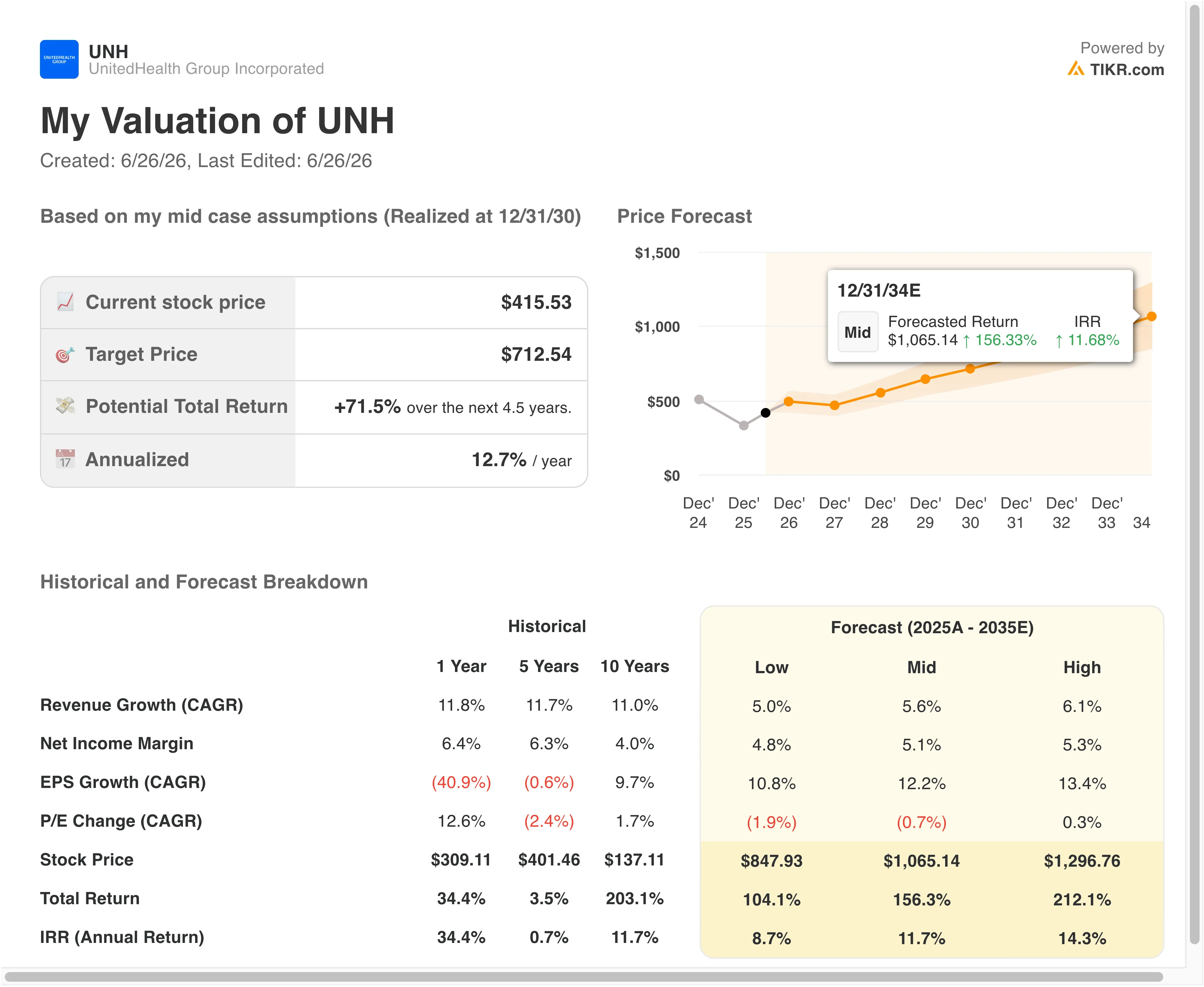

Key Stats for UNH Stock

- Past week’s performance: +5.22%

- 52-week range: $235 to $418

- Valuation model target price: $483

- Implied upside: +16.3% over 2.5 years

Value your favorite stocks like UnitedHealth with TIKR’s Guided Valuation Model (It’s free) >>>

Medical Costs, Lawsuits, and a Turnaround Still Being Earned

UnitedHealth Group Incorporated (UNH) has spent much of 2026 managing a narrative shaped by elevated medical costs and cascading legal developments. But June brought a notable shift in analyst tone. Bank of America upgraded UNH on June 4, citing improving medical cost trends. Medical loss ratio is the single most-watched metric for managed care insurers. When it falls, margins recover quickly given the company’s largely fixed cost base.

The upgrade came against a difficult backdrop. In late May, Massachusetts sued UnitedHealth’s insurance unit for allegedly defrauding the state’s Medicaid program. Medicaid is the government health insurance program for lower-income Americans. UnitedHealth administers Medicaid plans in multiple states as a managed care organization. Regulatory exposure in this segment has been a recurring concern for investors throughout 2025 and into 2026.

Q1 2026 results showed revenue of $111.7 billion, beating the consensus of $109.6 billion by nearly 2%. Adjusted EPS came in at $7.23, ahead of expectations. Management raised full-year EPS guidance to greater than $18.25. The company also eliminated most prior authorization requirements across its plans. Prior authorization is the insurer’s gatekeeping process that approves procedures before they happen.

UNH reinstated its Q2 2026 dividend of $2.32 per share, signaling financial stability. Bernstein separately raised its price target in late May, citing improved Medicare Advantage prospects. If UNH continues attracting analyst upgrades on improving claims data, the recovery thesis gains real credibility despite ongoing litigation.

See analysts’ growth forecasts and price targets for UNH (It’s free) >>>

Is UnitedHealth Stock Cheap After Peak Decline?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 2.6%

- Operating Margins: 6.1%

- Exit P/E Multiple: 18.3x

The model estimates a target price of $483, implying 16.3% total upside from the current price of $416 and a 6.2% annualized return over the next 2.5 years.

A 6.2% annualized return is modest for a stock down more than 40% from its five-year peak. But the model inputs reveal the real tension. The operating margin assumption of 6.1% sits above the current last-twelve-month EBIT margin of 4.2%. That margin reflects a period of elevated medical costs and one-time legal charges. Historically, UnitedHealth has sustained margins closer to 8% to 9% in favorable claims environments. A return toward that historical range would significantly improve the model’s implied return.

The revenue growth assumption of 2.6% is also conservative. UnitedHealth’s last-twelve-month revenue growth ran at 11.8%, and its decade-long compound growth rate sits near 11%. The model stress-tests a scenario where growth slows sharply, which is appropriate given Medicaid volume uncertainty and potential Medicare Advantage reimbursement changes. Medicare Advantage is the private-insurance alternative to traditional Medicare and represents UnitedHealth’s most growth-sensitive segment.

At $416, UNH trades at a last-twelve-month P/E of 31x but an NTM P/E of 21.8x. That compression between trailing and forward earnings is exactly what a margin-recovery thesis looks like in real time. The market is pricing in improvement, not yet fully visible in reported results.

Model UnitedHealth’s fair value scenarios in under 60 seconds (Free with TIKR) >>>

UnitedHealth vs. Cigna and Elevance Health

UnitedHealth Group is the largest managed care organization in the United States by revenue. Yet its stock’s relative performance in 2026 has lagged peers that avoided similar headline risk. Cigna Group (CI) and Elevance Health (ELV) are the two most direct comparisons.

Cigna trades at approximately 11x forward earnings, a steep discount to UnitedHealth’s 22x NTM P/E. Cigna’s revenue mix is more heavily weighted toward pharmacy benefit management through Express Scripts, giving it different margin dynamics. But Cigna’s operating margin runs higher than UnitedHealth’s managed care segment on a standalone basis.

Elevance Health, formerly Anthem, trades at roughly 14x to 16x forward earnings. Elevance has also faced elevated medical costs in 2025 and 2026. However, analysts at Cantor and Mizuho noted in May 2026 that the entire health insurer sector could see margin recovery over the next two to three years as the industry digests the post-pandemic claims spike. That view supports the thesis that UnitedHealth’s margin compression is cyclical rather than structural.

UnitedHealth retains a structural advantage neither peer can fully match: vertical integration through Optum, its health services and pharmacy subsidiary. Optum generates revenues exceeding $60 billion annually and operates at higher margins than the insurance segment. That diversification is why UnitedHealth historically commanded a premium multiple, and it remains the strongest argument for re-rating once the claims environment stabilizes.

Find out why investors are still reassessing UnitedHealth after Berkshire sold out >>>

What’s Driving UNH Stock Going Forward?

The Q2 2026 earnings report, scheduled for July 16, 2026, is the most important near-term catalyst. Investors will focus on the medical loss ratio for the quarter and whether management updates its full-year guidance. A stable or declining claims trend in Q2 would validate the BofA upgrade thesis and could trigger meaningful multiple expansion.

Medicare Advantage reimbursement rates are a second key driver. The Centers for Medicare and Medicaid Services sets payment rates annually. Any upward revision for 2027 would directly support UnitedHealth’s largest and most margin-sensitive segment.

Legal and regulatory exposure remains the primary risk. The Massachusetts Medicaid fraud lawsuit and any new state-level actions could keep sentiment subdued even if the underlying business improves. Management has not yet addressed the Massachusetts filing directly in public commentary.

The prior authorization rollback has real financial implications. Removing those gatekeeping steps could temporarily increase claims costs as more procedures get approved. But it may also reduce the administrative burden that has weighed on the stock’s reputation. Management commentary on July 16 will be the first opportunity to quantify that cost impact and frame the full-year outlook.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in UnitedHealth?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UNH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UNH stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!