Key Stats for SoFi Stock

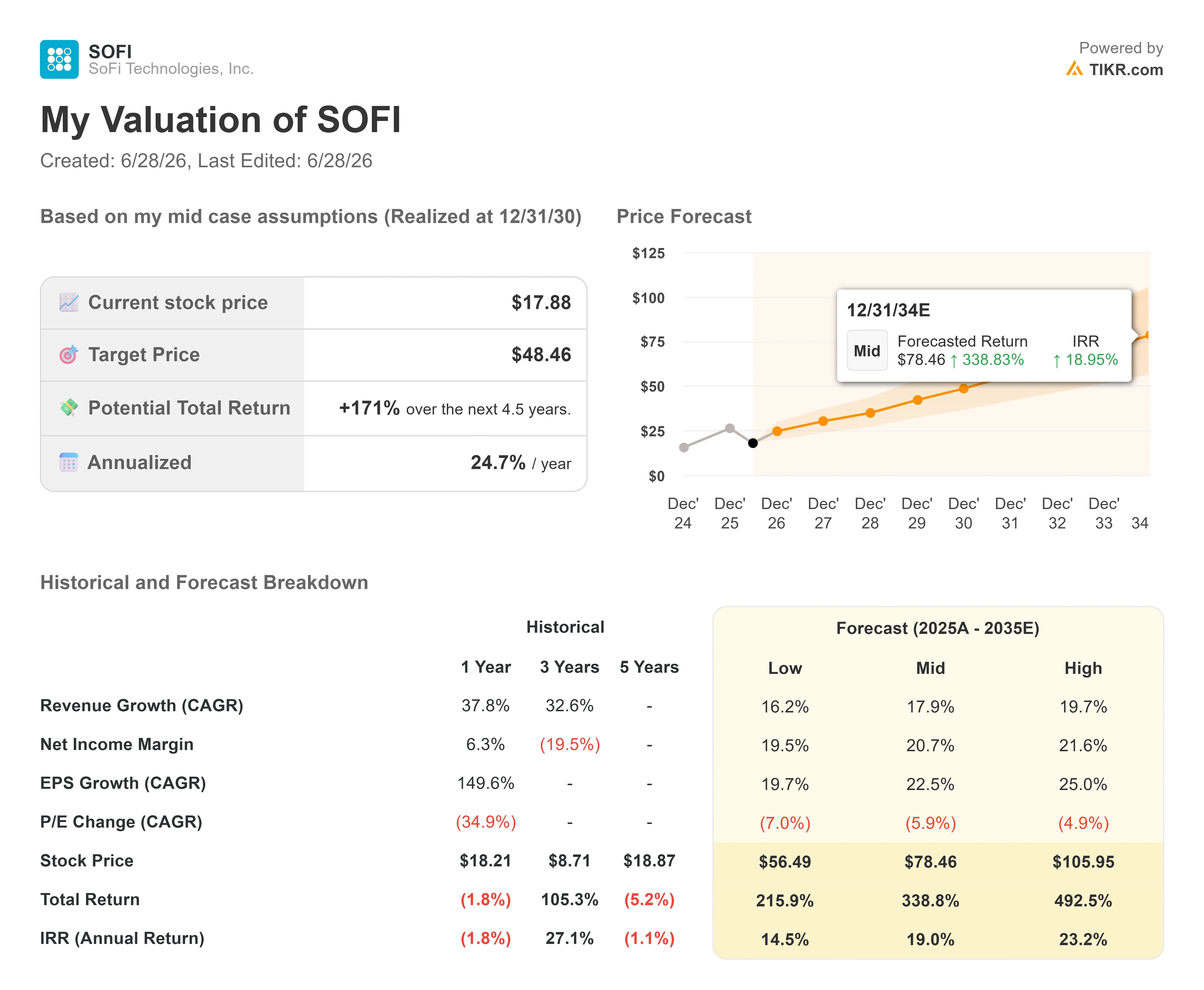

- Current Price: $17.88

- Target Price (Mid): ~$48

- Street Target: ~$21

- Potential Total Return: ~171%

- Annualized IRR: ~25% / year

- Earnings Reaction: -2.13% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

SoFi Technologies (SOFI) closed at $17.88 on June 26, down roughly 32% year to date, and the market still cannot decide what kind of company it is pricing. Bulls see a digital bank compounding revenue above 40% with record loan volumes. Bears see a richly valued lender with a short-seller report hanging over it and lending growth that may have already peaked. That tension has kept the stock trapped between the mid-$15s and $19 for weeks.

The unresolved question is simpler than the noise around it. Is SoFi still a consumer lender that deserves a lender’s multiple, or is it becoming a payments and banking infrastructure company that earns money in a structurally different way? The answer matters because one of those businesses is capital-intensive and credit-sensitive, and the other is neither.

The Business the Market Is Ignoring

While attention stayed on lending, SoFi launched four revenue streams that did not exist a year ago. The most important is SoFiUSD, a bank-issued stablecoin that became available to members inside the SoFi app on May 27, 2026. SoFiUSD, meaning a dollar-pegged digital token backed 1:1 by cash, is the first stablecoin issued by a U.S. national bank on a public blockchain.

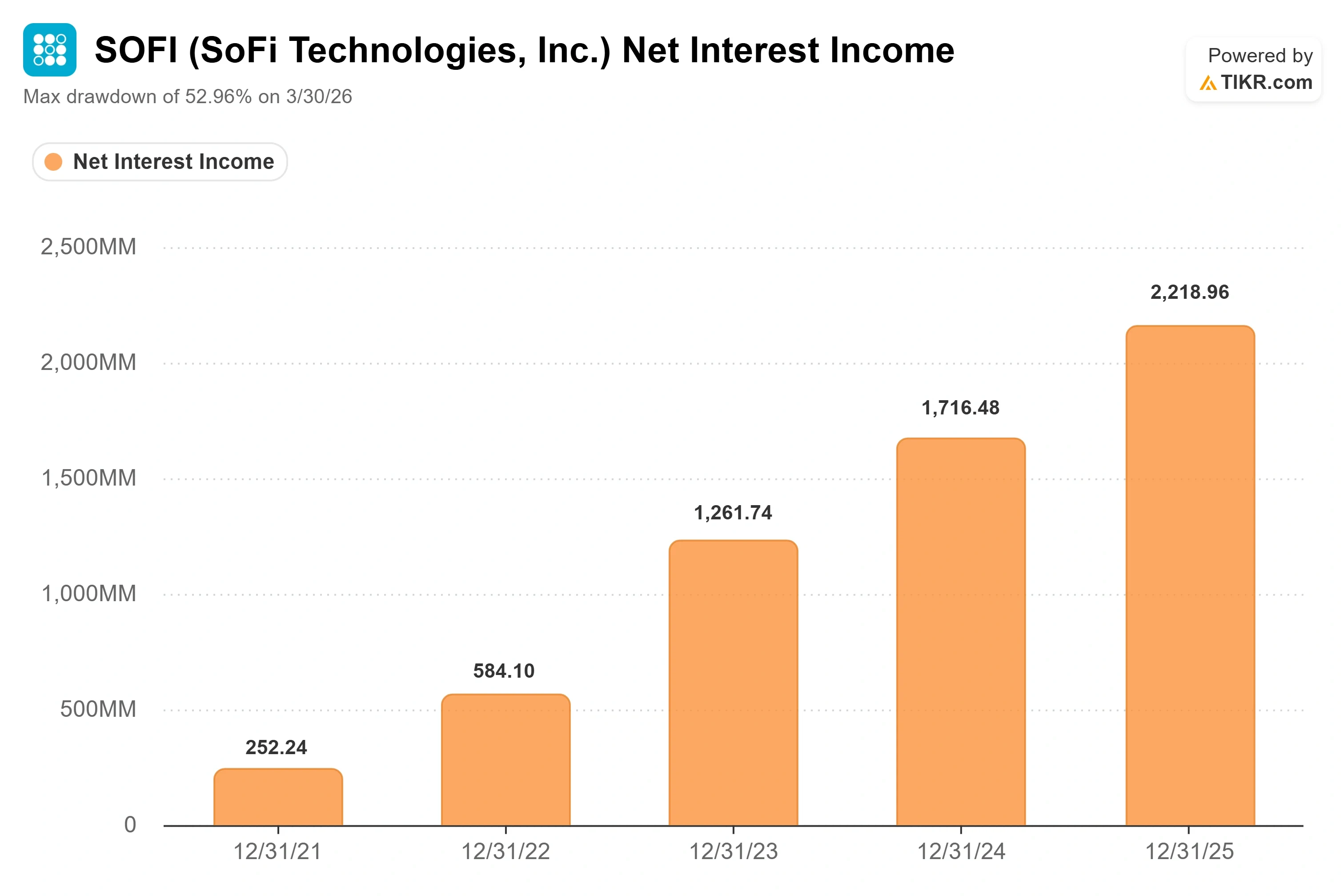

The mechanics are what make it different. CEO Anthony Noto explained the economics directly at the J.P. Morgan technology conference on May 19, 2026. He described SoFiUSD as a payment capability with stored value, where SoFi earns money “based on the net interest income it generates from it sitting in our Fed master account earning Fed funds without liquidity risk without credit risk and without duration risk, unlike any other stablecoin issuer to date.” That matters because it reframes a crypto product as a deposit-funding engine that avoids the credit exposure weighing on the lending thesis.

The reach is already being built. In March 2026, SoFi and Mastercard announced a deal to enable SoFiUSD as a settlement currency across Mastercard’s global network, supporting 24/7 settlement, where the card network currently settles only five days a week. SoFi processes around 8 billion transactions a year through Galileo, its payments technology platform, and Noto wants those transactions moving over SoFiUSD rails over time.

See historical and forward estimates for SoFi stock (It’s free!) >>>

A New Banking Layer Goes Live July 1

The second piece is Big Business Banking, which Noto said launches with APIs on July 1, 2026. APIs, meaning the software connections that let other companies plug in automatically, make the product fully agentic for enterprise clients that want it. SoFi can operate in both fiat and crypto as a national bank, a combination that Noto said crypto intermediaries specifically asked the company to build.

These businesses share one trait that the lending segment does not. As Noto put it, “they’re not capital-intensive businesses. They are high-margin, high-return businesses.” That distinction sits at the center of the bull case, because it implies returns can rise without the balance sheet risk that defines a traditional lender. SoFi also reinforced the AI side of its platform on June 23, 2026, announcing Composer by SoFi, an AI-powered investing tool acquired through Composer Securities.

SoFi’s premium to peers is the crux of the debate. On the TIKR Competitors page, SoFi trades at around 28x NTM P/E, against Ally Financial at around 8x, SLM Corporation at around 10x, and Upstart Holdings at around 13x. That premium is indefensible if SoFi is only a lender. It is far easier to justify if the stablecoin and banking-infrastructure layer scales into the high-margin, fee-and-NIM business management is describing, since none of those peers carry a bank charter wired into on-chain settlement.

See how SoFi performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

The TIKR model uses its mid-case scenario, which prices SoFi at a target of around $48 by the end of 2030, implying around 171% total return from $17.88, or roughly 25% annualized over the next 4.5 years.

See analysts’ growth forecasts and price targets for SoFi stock (It’s free!) >>>

Two drivers support the revenue CAGR of around 18% in the mid case. The first is cross-sell across the member base, where 70% of SoFi Invest members already come from existing members, lifting lifetime value without new acquisition cost. The second is the expanding non-lending mix, where Financial Services, SoFiUSD, and Big Business Banking add fee and net interest income outside the lending balance sheet.

The margin driver is operating leverage, with the mid-case projecting net income margins expanding to around 21% by 2030 from 15% in Q1 2026 as fixed costs spread across a larger revenue base. The primary risk is credit deterioration: if personal loan charge-off rates rise materially, fair value marks on the loan portfolio compress and the margin path stalls, pulling the multiple toward the 8-to-10x range that traditional lenders command.

The upside is a stock approaching around $48 by 2030 if credit holds and the non-lending businesses scale as management describes. The downside is a re-rating toward lender multiples if the stablecoin and banking layer stay small and lending growth slows, a scenario that would leave the premium stranded.

Conclusion

The single number that resolves this thesis is the back-half EBITDA margin. Consensus expects margins to climb from 31% in Q1 toward roughly 37% to 38% in the second half of 2026, and management has kept full-year guidance unchanged despite a record Q1. Watch SoFi’s Q2 2026 results, expected July 27. A guidance raise alongside margins tracking toward that 37% range would signal the operating leverage is real and hand bulls the catalyst they have waited for. Flat guidance again, or margins stuck near 31%, would tell investors the caution is structural, not conservative. July 27 begins to answer which one it is.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SoFi?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SoFi, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SoFi alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!