Key Stats for UNH Stock

- Past week’s performance: Consolidating

- 52-week range: $235 to $404

- Valuation model target price: $427

- Implied upside: +9.8% over 2.6 years

Value your favorite stocks like UNH with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

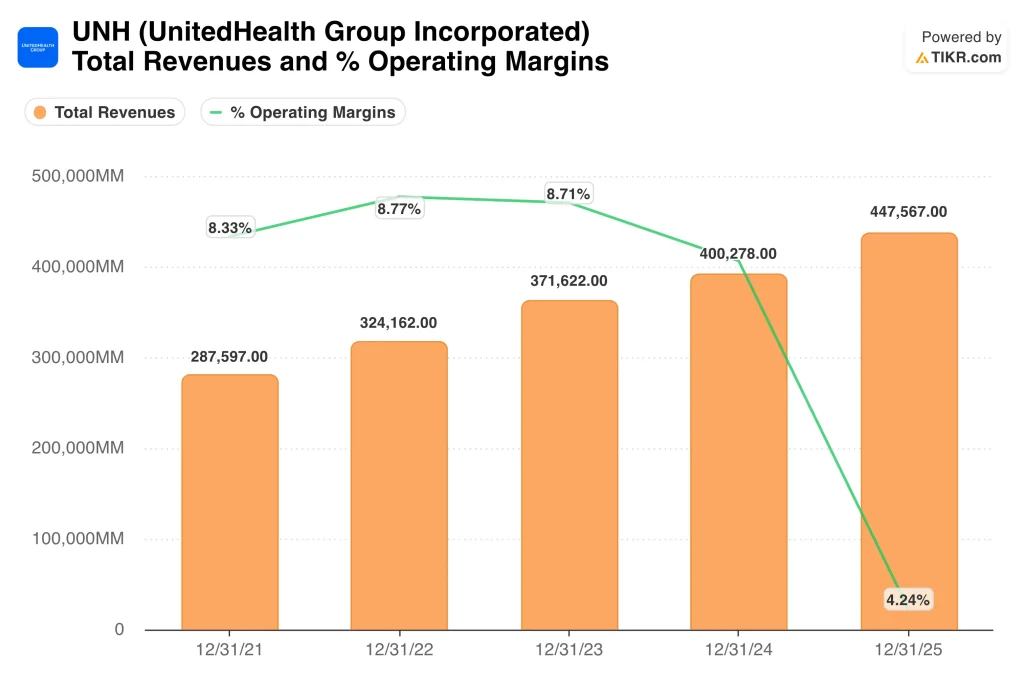

UnitedHealth (UNH) reported Q1 2026 revenue of $111.7 billion, beating the analyst consensus of $109.6 billion. However, operating income fell 1% to $8.99 billion, signaling that cost pressures are still weighing on profitability.

Operating income is the profit earned from core business operations before accounting for interest and taxes. Investors welcomed the revenue beat but remained cautious about the margin picture, and the stock has largely traded sideways near recent levels.

Berkshire Hathaway disclosed in mid-May that it had fully exited its UnitedHealth position. Berkshire is widely followed as a benchmark for long-term quality investing, so the disclosure drew significant market attention.

Warren Buffett’s firm also sold stakes in Amazon and Visa during the same period, suggesting a broader portfolio repositioning. But UNH shares still slipped on the news, as investor confidence in the health insurer remained fragile.

UnitedHealthcare announced it would cut prior authorization requirements for approximately 30% of healthcare services by the end of 2026. Prior authorization is the process by which insurers must approve certain treatments before they are covered, and it has drawn significant regulatory scrutiny.

Reducing this burden could improve patient outcomes and lower administrative friction for providers. However, investors are watching closely whether eliminating more approvals increases medical claims spending and adds further pressure to margins. Analysts at Cantor and Mizuho separately noted they see a path to margin recovery for health insurers over the next few years.

Going forward, UNH stock will hinge on whether medical cost ratios stabilize and margins begin recovering toward historical levels.

See analysts’ growth forecasts and price targets for UNH (It’s free) >>>

Is UNH Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 4%

- Operating Margins: 4.2%

- Exit P/E Multiple: 23x

Based on these inputs, the model estimates a target price of $427, implying 9.8% total upside from the current share price and a 3.6% annualized return over the next 2.6 years.

A 3.6% annual return falls well below what most equity investors consider attractive. So the model positions UnitedHealth as fairly valued rather than compellingly cheap at current prices. The operating margin assumption of 4.2% reflects the compressed environment the company is navigating today.

This implies no meaningful margin expansion over the forecast period, which is a conservative but realistic baseline given ongoing medical cost pressures.

The revenue CAGR of 4.0% is consistent with forward analyst estimates, which project approximately 1.0% two-year revenue growth. UnitedHealth operates two large segments: UnitedHealthcare, the insurance business, and Optum, a diversified health services unit covering pharmacy, care management, and data analytics.

Revenue growth depends on membership trends, plan pricing adjustments, and Optum’s ability to expand its client base and care delivery footprint across the country.

The exit P/E of 23.0x implies moderate multiple expansion from today’s NTM P/E of approximately 20.5x. For that expansion to occur, investors would need to see medical cost ratios stabilize and the margin recovery narrative gain credibility with evidence.

Peer insurers like CVS Health are also navigating elevated medical costs. But UnitedHealth’s Optum diversification may provide a structural advantage in working through this part of the cycle.

What’s Driving UNH Stock Going Forward?

Medical cost trends are the most critical near-term driver for UNH. The company’s LTM EBIT margin is 4.2%, reflecting elevated claims spending in recent quarters. If utilization rates moderate as expected, margins can recover toward historical levels near 8%. Management’s ability to reprice insurance plans and control care costs will determine the pace of that recovery.

The prior authorization changes carry both risk and opportunity. Cutting approvals for 30% of services could increase near-term medical spending. However, it may also reduce the regulatory pressure that has weighed on the business in recent periods.

Optum Rx also launched a transparent fee-based pharmacy care model for PBM clients. PBM stands for pharmacy benefit manager, which is an intermediary that negotiates drug prices on behalf of insurance plans. Optum’s growth trajectory is a key long-term value driver. This health services segment generates more stable, fee-based revenue than the core insurance business and earns better margins.

Expanding Optum’s care delivery and analytics capabilities is central to management’s multi-year strategy. A growing Optum could provide a meaningful structural offset if the insurance segment faces continued cost headwinds.

Q2 2026 results, expected in July, will be a critical moment for investor confidence. Updated guidance on medical cost ratios and margin trajectory will be closely scrutinized. Analysts at Cantor and Mizuho see a path to improvement over the next few years. But concrete evidence of stabilization is needed before broader investor sentiment on UNH turns more constructive.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in UnitedHealth Group Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UNH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UNH stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!