Key Takeaways for Synopsys Stock as of June 2026

- Analysts rate Synopsys stock 13 buys, 6 holds, and 1 underperform, with a mean target of $564, implying around 24% upside from the current price of $454.

- TIKR’s mid-case model values Synopsys at around $827 by October 2030, implying around 82% total return, or roughly 15% annualized.

- Synopsys stock looks undervalued at current levels, with EBITDA margins expanding sequentially each quarter through fiscal 2027 as Elliott-driven cost discipline accelerates synergy realization ahead of schedule.

- Synopsys raised full-year fiscal 2026 non-GAAP EPS guidance to a midpoint of $14.76 following a Q2 beat on revenue ($2.276B vs. $2.25B estimated), operating margin, and adjusted EPS ($3.35 vs. $3.15 estimated).

Synopsys Stock Beats Q2 on Revenue and EPS, Then Raises Guidance Across All Metrics

Synopsys (SNPS), the leading provider of electronic design automation (EDA) software, semiconductor intellectual property (IP), and multiphysics simulation, reported fiscal Q2 2026 results that beat guidance on every major metric and triggered a full-year raise across revenue, operating margin, EPS, and free cash flow.

That beat was broad-based: revenue came in at $2.276 billion against an estimate of $2.25 billion, adjusted EPS of $3.35 cleared the $3.15 consensus estimate by roughly 6%, and non-GAAP operating margin reached 39.5%.

Beneath the headline, the Design Automation segment generated approximately $1.822 billion in revenue, with EDA growing slightly over 8% year over year as hyperscalers scaled hardware-assisted verification workloads for complex AI chip designs.

The more important signal is IP. Design IP revenue reached $454 million in Q2, down roughly 6% year over year but up 12% sequentially from the Q1 trough, as Synopsys shifts custom-on-top (COT) hyperscaler engagements toward a use-fee-plus-royalty model rather than a legacy one-time license structure.

On the same day as earnings, CEO Sassine Ghazi addressed the demand environment directly on Q2 earnings call: “AI is scaling semiconductor demand, architectural diversity and complexity of both chips and the systems they power, driving increased demand across our portfolio.”

The bigger story, though, is Elliott Investment Management’s cooperation agreement, which added managing partner Jesse Cohn to the board effective June 1 and accelerated the committed $400 million in Ansys integration cost synergies, with roughly half now targeted for realization by fiscal year-end.

Full-year fiscal 2026 guidance now calls for revenue of $9.625 billion to $9.705 billion, non-GAAP operating margin of 41% at the midpoint, non-GAAP EPS of $14.72 to $14.80, and free cash flow of approximately $2 billion.

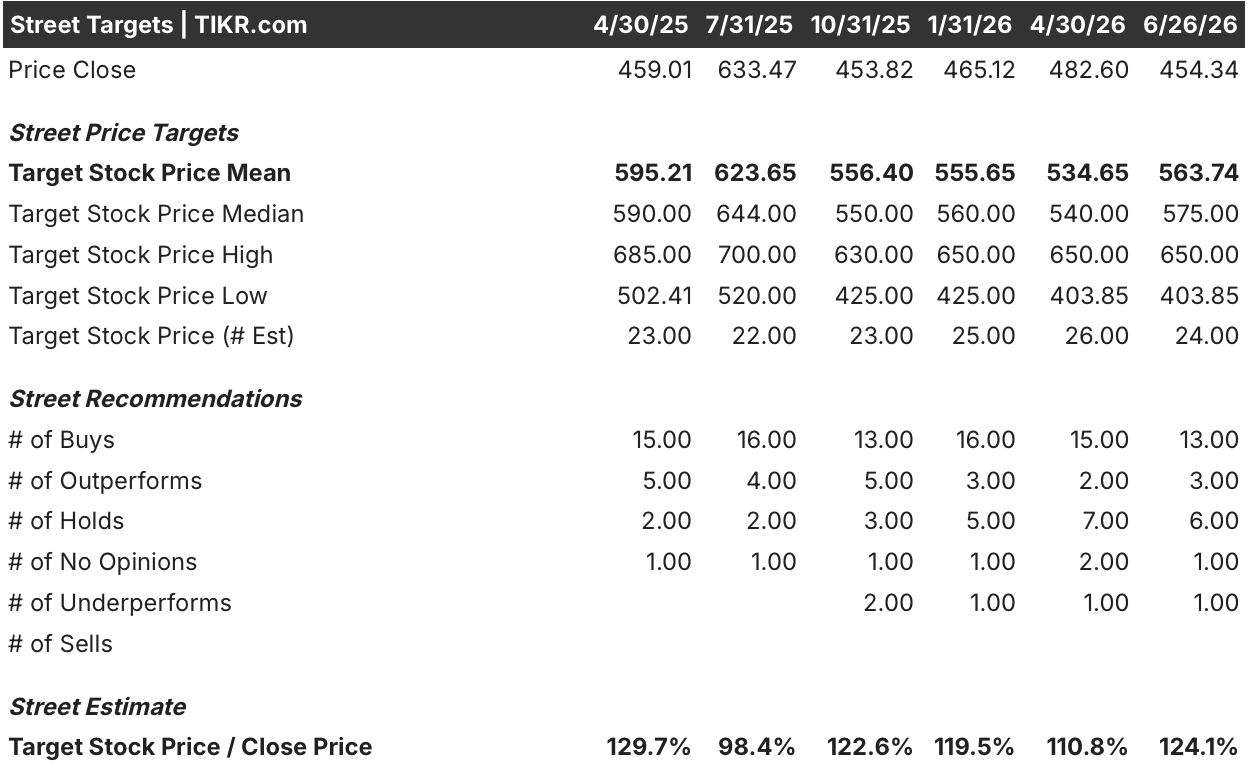

Wall Street Rates Synopsys Stock a Buy, With the Mean Target Implying 24% Upside

Wall Street rates Synopsys stock a buy, with 13 buy-equivalent ratings, 6 holds, and 1 underperform among the 24 analysts covering the stock as of June 26, 2026.

The mean price target stands at $564, implying around 24% upside from the current price of $454, with the median at $575 and the high target at $650. Following Q2 results, JPMorgan described the guidance as conservative, reinforcing the existing buy-skewed coverage despite the stock’s underperformance relative to the Nasdaq’s year-to-date gain.

Wall Street Expects Synopsys Stock’s EBITDA Margins to Expand Past 48% by Early Fiscal 2027

Synopsys delivered Q2 fiscal 2026 EBITDA of around $0.95 billion, representing a margin of 41.9%, up from 38.4% in the prior quarter. That Q2 figure already marked a meaningful step up in operating profitability following the Ansys acquisition, and consensus expects the expansion to continue without interruption.

For Q3 2026, analysts estimate EBITDA of around $1.03 billion, implying a margin of roughly 42%, with Q4 fiscal 2026 estimates reaching around $1.12 billion and a margin near 44%. The trajectory reflects both accelerating Ansys integration synergies and tighter cost discipline across the combined entity, with management confirming roughly half of committed synergies will be realized by fiscal year-end.

The longer-range picture sharpens further. By Q1 fiscal 2027, consensus estimates EBITDA of around $1.28 billion, implying a margin of roughly 49%, a level that would bring Synopsys’s operating profitability within reach of the mid-40s non-GAAP operating margin the company has targeted and Elliott has pushed to accelerate.

The unresolved condition the Street is waiting on: whether the royalty-based IP monetization model and consumption-based EDA licensing for agentic workflows, both flagged by management as emerging inflection points, produce contract wins with material fiscal 2027 revenue impact before the September 30 Investor Day.

Synopsys Stock Is Outpacing Cadence on EBITDA Growth While Keysight Fades

Synopsys leads the peer group on EBITDA growth YoY, posting 47% in Q2 fiscal 2026 against Cadence Design Systems’ (CDNS) 28% and Keysight Technologies’ (KEYS) 69%, with Keysight’s spike driven by a easy compare rather than structural acceleration.

The forward picture widens the gap further. Consensus estimates SNPS EBITDA growth of around 45% in Q3 fiscal 2026 against Cadence’s around 28%, with Keysight expected to normalize sharply toward the low single digits by fiscal 2027.

What that means for investors is that Synopsys stock is capturing Ansys-driven EBITDA expansion at a pace neither peer can match on a structural basis through the estimate period.

TIKR’s $827 Target on SNPS Stock Holds If the Margin Trajectory Reaches the Mid-40s

TIKR’s mid-case model values Synopsys at around $827 by October 2030, implying around 82% total return from the current price of $454, or roughly 15% annualized.

That return requires an active margin expansion case: the mid-case assumes around 11% annual revenue growth and net income margins expanding to roughly 32%.

The September 30 Investor Day, where management committed to presenting the royalty monetization framework and long-term financial model, is the catalyst that confirms or pressures that case.

Should You Invest in Synopsys, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Synopsys stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Synopsys stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SNPS stock on TIKR for Free →