Key Stats for Toast Stock

- Past-Week Performance: -1%

- 52-Week Range: $24.99 to $49.7

- Current Price: $25.07

What Happened?

Toast stock (TOST) has spent recent weeks absorbing a paradox that defines its current investment case: a company posting record 30,000 net location adds, 33% recurring gross profit growth, and $633 million in adjusted EBITDA while still trading down 34.2% over the past 12 months, with shares closing at $25.07 on February 23.

Sentiment cracked immediately after the February 12 earnings report, when RBC Capital flagged that slightly lower payments ARR and the FY26 adjusted EBITDA guidance range of $775 million to $795 million fell short of elevated market expectations, sending shares down 1.8% to $25.58 in premarket trading on February 13.

The specific pressure point was the guidance itself, as Toast’s FY26 recurring gross profit growth outlook of 20% to 22% and an additional 150 basis points of hardware margin headwind from surging memory chip costs introduced uncertainty that overshadowed a clean Q4 revenue beat of $1.6 billion against the $1.6 billion consensus estimate.

However, the market’s mental model of Toast is quietly shifting from a pure payments processor narrative toward a vertically integrated AI platform story, as ToastIQ’s adoption by over 50% of all Toast locations within four months of launch signals that software monetization, not just payment volume, will increasingly drive the company’s valuation multiple.

CEO Aman Narang stated on the Q4 earnings call that “we are positioned to drive durable growth from over $2 billion in the ARR today to $5 billion and $10 billion and beyond,” framing Toast’s long-term expansion across retail, international, and enterprise markets as a structural re-rating opportunity rather than a near-term earnings story.

Adding institutional weight to that long-term thesis, Bernstein upgraded Toast to Outperform from Market-Perform on February 16, while ValueAct Holdings raised its stake to 8.0 million Class A shares as of December 31, signaling that sophisticated long-term investors view the current price dislocation as an entry opportunity rather than a structural breakdown.

Over the next three to five years, Toast’s simultaneous expansion into retail, international markets, and enterprise drive-thru, combined with an AI platform capable of replacing fractional restaurant operators in marketing, payroll, and bookkeeping, positions the company to convert its current 20% U.S. SMB market share into a dominant, multi-vertical operating system for the global hospitality industry.

Wall Street’s Take on TOST Stock

Despite the post-earnings selloff that dragged shares to $25.07, Toast’s record 30,000 net location adds, 26% ARR growth, and $608 million in free cash flow signal that the business engine is accelerating precisely when the stock price suggests the opposite.

The fundamental case sharpens further when examining the earnings trajectory, as normalized EPS flipped from a $0.44 loss in FY2023 to $1.01 in FY2025, with Street estimates projecting $1.28 in FY2026, representing 26.7% growth on top of an already profitable base.

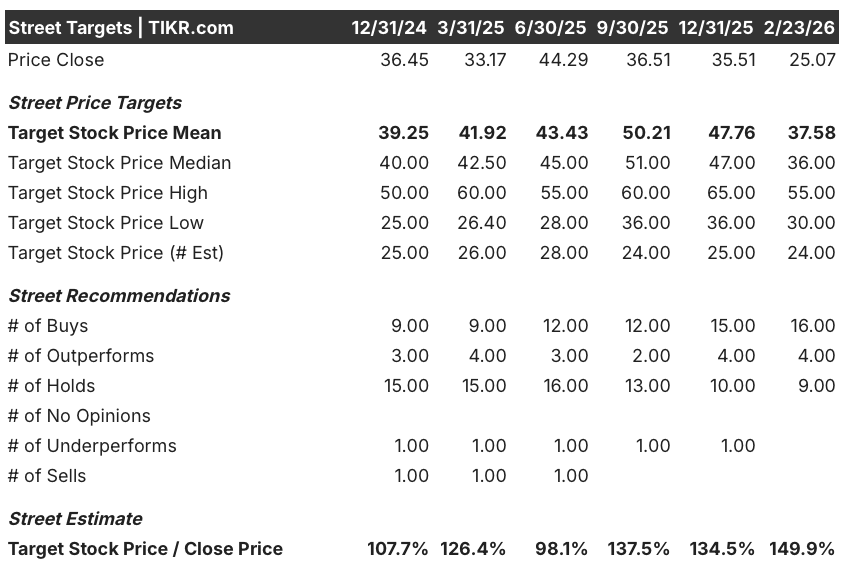

Wall Street’s conviction remains firmly bullish, with 16 buys and 4 outperforms against only 9 holds and zero sells, and the current mean price target of $37.58 implies 50% upside from the February 23 close of $25.07.

The target spread reinforces the asymmetry, as the Street’s low target of $30.00 still implies 19.7% upside from current levels while the high target of $55.00 implies 119.4% upside, framing $25.07 as a range where even the bears expect appreciation.

What Does the Valuation Model Say?

Anchoring that Wall Street optimism to a bottom-up framework, a mid-case valuation model built on 15.4% revenue CAGR and 11.0% net income margins prices Toast at $50.36 by December 31, 2030, representing a 100.9% total return and a 15.5% annualized IRR from today’s beaten-down price.

The credible bear case, however, centers on the FY26 guidance embedding 150 basis points of hardware margin pressure from memory chip cost inflation, and on a P/E multiple that the model itself projects will compress at a 8.8% CAGR annually through 2030, meaning earnings growth must outrun multiple contraction to deliver returns.

At $25.07, Toast looks materially undervalued relative to its fundamentals, its analyst consensus, and its long-term model, making the current price an opportunity driven by short-term guidance noise rather than any structural deterioration in the business.

Should You Invest in Toast, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Toast stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Toast, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TOST stock on TIKR for Free →