Key Stats for Take-Two Stock

- This Week Performance: +4%

- 52-Week Range: $188.6 to $264.8

- Current Price: $207.3

What Happened?

Take-Two Interactive (TTWO) has shattered its own earnings ceiling, with net bookings of $1.76 billion blowing past the $1.6 billion guidance ceiling and pushing TTWO to $207.31 as the company’s mobile empire, NBA 2K franchise, and GTA Online all simultaneously outperformed expectations in Q3 FY2026.

Driving the immediate re-rating, Saudi Arabia’s Public Investment Fund transferred its 11.4 million-share stake worth roughly $2.4 billion to subsidiary Savvy Games Group on February 17, restructuring one of Take-Two’s largest institutional positions and signaling that sovereign wealth capital remains deeply committed to the GTA VI story.

The mechanics behind the surge run deeper than any single title, as recurrent consumer spending surged 23% to represent 76% of net bookings, with NBA 2K up 30%, GTA Online up 27%, and Toon Blast alone growing 43% while crossing $3 billion in lifetime net bookings across a portfolio firing on every cylinder simultaneously.

The market is rapidly repricing TTWO from a console-dependent publisher into a diversified, recurring-revenue entertainment platform, as management raised its full-year net bookings outlook to $6.65 billion to $6.7 billion, representing 18% growth and roughly $725 million above the initial guidance issued in May, while operating cash flow guidance nearly doubled from $250 million to $450 million.

Chairman and CEO Strauss Zelnick stated on the Q3 earnings call that “we are actively embracing generative AI” with “hundreds of pilots and implementations across our company, including with our studios,” signaling that AI-driven efficiency gains are already compressing production costs ahead of the GTA VI launch cycle.

Further reinforcing institutional conviction, Savvy Games Group formally received 11.4 million Take-Two shares per SEC filing on February 17, preserving the near-$3 billion sovereign position under a gaming-focused subsidiary structure that keeps one of the world’s most well-capitalized gaming investors anchored to TTWO’s November 19 GTA VI launch.

Looking out three to five years, Take-Two’s combination of a November 19 GTA VI launch, a 37% NBA 2K RCS growth trajectory, record mobile direct-to-consumer momentum, and AI-driven cost efficiency positions the company to establish an entirely new revenue baseline that could permanently separate it from every other traditional video game publisher competing for the same audience.

Wall Street’s Take on Take-Two Stock

Take-Two’s Q3 FY2026 earnings beat and raised full-year net bookings guidance to $6.65 billion to $6.7 billion, directly confirming that the GTA VI launch cycle is compressing into an accelerating revenue ramp rather than a speculative future event.

Beneath the headline beat, the fundamental trajectory is genuinely strengthening, with FY2026 revenue estimates pointing to 18.4% growth to $6.69 billion and EBITDA expanding 44.2% YoY to $1.09 billion, reversing years of margin compression as recurrent consumer spending scales toward 78% of net bookings.

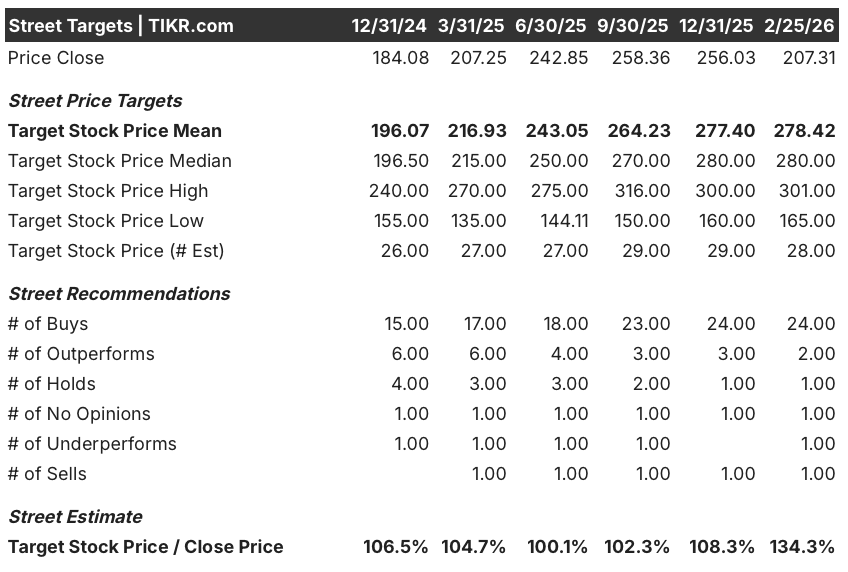

Wall Street firmly backs the move, with 24 buys and 2 outperforms against just 1 hold and 1 sell among 28 analysts, while the mean price target of $278.42 implies 34.3% upside from the current price of $207.31, a conviction level that has held and grown even as the stock pulled back sharply from its 52-week high of $264.79.

The spread between the analyst low target of $165 and the high of $301 is wide enough to demand attention, with the bear case hinging on GTA VI execution risk or a broader consumer spending pullback, while the bull case unlocks if GTA VI launches cleanly on November 19 and drives the recurrent consumer spending flywheel Wall Street is already pricing in.

What Does the Valuation Model Say?

Given the Q3 outperformance, raised cash flow guidance, and a GTA VI launch on the horizon, TIKR’s mid-case DCF model pricing TTWO at $384.61 with an 85.5% total return and a 16.3% annualized IRR over 4.1 years feels grounded in a business that is finally converting its creative pipeline into durable earnings power.

The single most consequential risk, however, remains GTA VI execution, as any delay or underwhelming launch would collapse the FY2027 net bookings baseline management is projecting, and the stock’s 21.8% P/E compression already visible in the valuation model’s low-case CAGR of negative 5.4% shows how quickly sentiment could reverse.

At $207.31, TTWO looks meaningfully undervalued relative to both analyst consensus and the DCF mid-case, with the November 19 GTA VI launch serving as the single most important event that will determine whether this stock reclaims its 52-week high or tests the low end of the analyst target range.

Should You Invest in Take-Two Interactive Software, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TTWO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Take-Two Interactive Software, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TTWO stock on TIKR for Free →