Key Stats for Verizon Communications Stock

- Past-Week Performance: 0.5%

- 52-Week Range: $38.4 to $50.5

- Current Price: $49.2

What Happened?

Verizon stock (VZ) sits at $49.23 after pulling back 1.3% on February 25, yet the more compelling story is the turnaround momentum building underneath the surface, as the company just delivered its highest quarterly postpaid phone net adds in six years at 616,000, signaling that new CEO Dan Schulman’s aggressive subscriber-growth strategy is already producing measurable results ahead of a transformational 2026.

The flashpoint driving renewed conviction is Schulman himself, who within his first 100 days authorized a Board-approved $25 billion share repurchase program, raised the annual dividend for the 20th consecutive year by $0.07 per share, and issued 2026 adjusted EPS guidance of $4.90 to $4.95, representing 4% to 5% growth and a more than 70% acceleration at the midpoint versus 2025 performance.

Powering the move is a multi-layered operational engine: Verizon closed its $20 billion Frontier acquisition on January 20, adding over 30 million combined fiber passings, securing a renewed long-term MVNO agreement with Comcast and Charter, and targeting $5 billion in 2026 OpEx savings alongside at least $1 billion in Frontier run-rate synergies by 2028.

Beyond the numbers, the market is beginning to re-rate Verizon from a stagnant dividend stalwart into a convergence growth story, as bundled fiber-plus-wireless customers churn 40% less than standalone mobility subscribers, giving the company a credible path to sustainable top-line acceleration as it targets 40 to 50 million fiber passings over the medium term.

CEO Dan Schulman stated on the Q4 earnings call that “we are targeting a range of 750,000 to 1 million postpaid phone net adds, approximately 2 to 3x our 2025 total and the highest since 2021,” contextualizing a subscriber growth ambition underpinned by Frontier cross-sell opportunities, a new value proposition targeting launch in the first half of this year, and a convergence strategy designed to structurally reduce churn.

On the institutional front, Mubadala Investment Co. PJSC fully dissolved its Verizon stake as of December 31, 2025, representing a notable exit by a sovereign wealth fund, while CFO Tony Skiadas took the stage at the Barclays Communications and Content Symposium on February 24 to reinforce free cash flow guidance of at least $21.5 billion, the company’s strongest projection since 2020.

Looking ahead, Verizon’s convergence build positions it as a structural competitor in the broadband market for the next three to five years, as its 50 million fiber passing target, AI Connect deals with hyperscalers, and disciplined capital allocation framework collectively signal a company transitioning from defensive income play to an offensive, cash-generating growth platform that its rivals will be forced to match.

Wall Street’s Take on Verizon Communication Stock

Verizon’s Frontier acquisition close on January 20 and its $25 billion buyback authorization directly translate into a materially stronger forward earnings trajectory, with convergence-driven churn reduction and $5 billion in 2026 OpEx savings now embedded in the company’s financial roadmap.

Underneath the headlines, the fundamentals confirm acceleration: consensus estimates project 2026 revenue reaching $144 billion, a 4.2% jump from $138.2 billion in 2025, while EBITDA margins expand to 36.8% and normalized EPS climbs to $4.91, a 4.3% year-over-year improvement after years of stagnation.

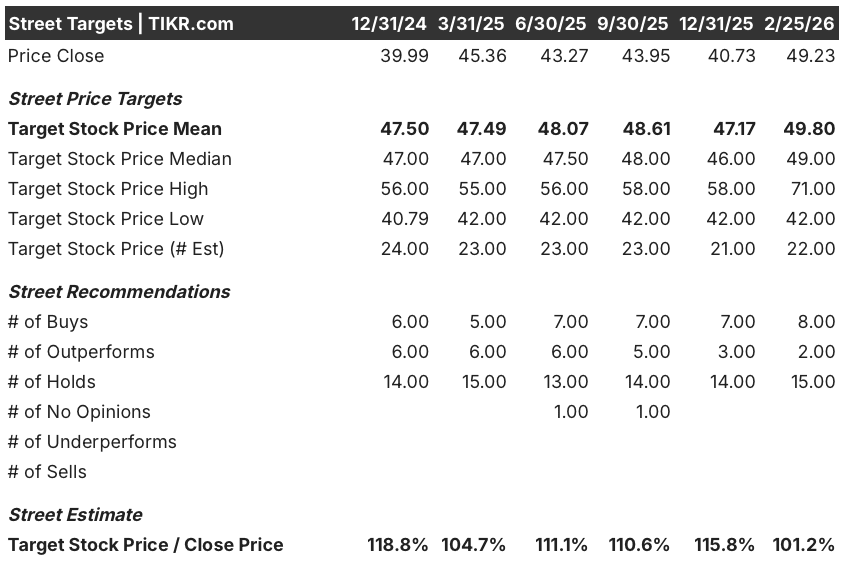

Wall Street currently shows 8 buys, 2 outperforms, and 15 holds against zero sells, with the mean price target sitting at $49.80, implying just 1.2% upside from the February 25 close of $49.23, suggesting analysts are holding conviction rather than aggressively upgrading into Schulman’s still-early turnaround.

The spread between the analyst low target of $42 and the high of $71 is wide enough to demand attention, with the bear case hinging on continued churn pressure and promotional cost overruns, while the bull case unlocks if convergence net add momentum and Frontier synergies exceed the $1 billion run-rate target by 2028.

What Does the Valuation Model Say?

Given that Verizon is now guiding to its strongest free cash flow since 2020 and accelerating EPS growth, TIKR’s mid-case valuation model prices VZ at $68.42, a 39% total return over 4.8 years at a 7% annualized IRR, a profile that looks credible if subscriber growth and margin expansion compound as management projects.

The most visible risk sits in the transition year revenue guidance itself: wireless service revenue is expected to remain flat in 2026 as Verizon laps roughly 180 basis points of prior price-increase headwinds, and any execution stumble on the new value proposition launch in the first half of this year could delay the volume-driven revenue inflection the bull case depends on.

Overall, Verizon looks modestly undervalued at $49.23 for patient investors, as the Frontier integration, $5 billion cost transformation, and buyback program provide a durable return floor, though the real re-rating hinges on the first-half value proposition launch and whether postpaid net adds track toward the 750,000 to 1 million target.

Should You Invest in Verizon Communication Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VZ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Verizon Communication Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VZ stock on TIKR for Free →