Range Resources Corporation (NYSE: RRC) trades near $38/share and has shown steady resilience as natural gas sentiment improves. Strong margins, disciplined spending, and a healthier balance sheet have helped support performance despite broader commodity volatility.

Recently, management highlighted improving volume trends and continued financial strengthening. Net debt remains low relative to earnings, and RRC has positioned itself more efficiently than peers as natural gas pricing begins to stabilize. These developments suggest the company is entering a more stable phase as it approaches 2026.

This article explores where Wall Street analysts expect the stock to trade by 2027. We combined consensus price targets and TIKR’s valuation model to outline RRC’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

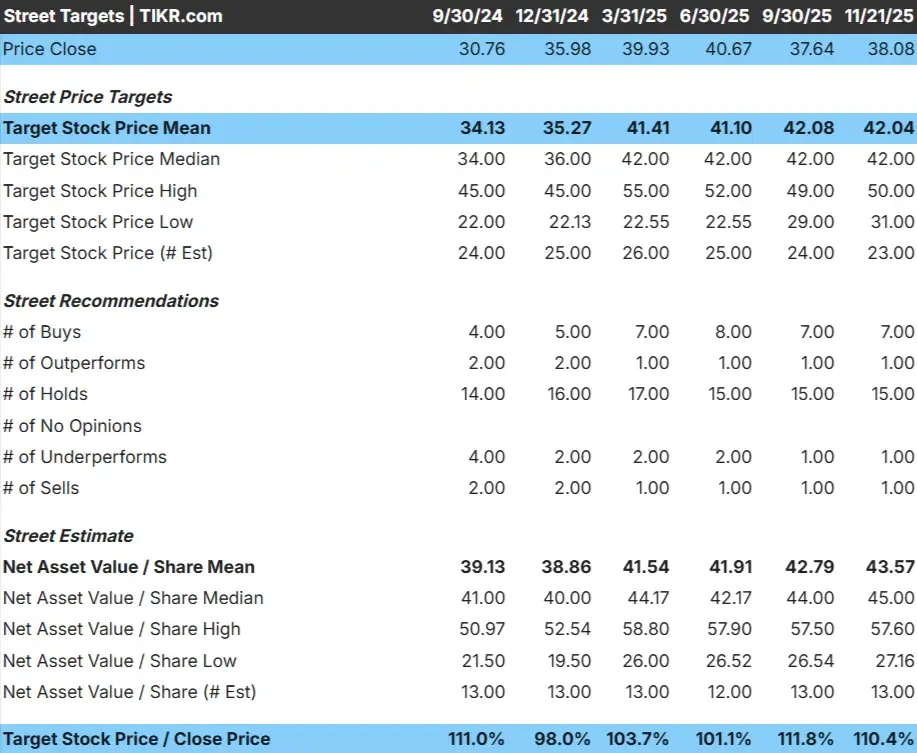

RRC trades around $38/share, and the Street’s average price target sits near $42/share, which points to modest upside over the next year. The tight cluster of estimates shows analysts generally agree on the company’s near term outlook.

Street Breakdown (11/21/25 data):

- High estimate: ~$50/share

- Low estimate: ~$31/share

- Median target: ~$42/share

- Ratings: 7 Buys, 1 Outperform, 15 Holds, 1 Underperform, 1 Sell

For investors, this suggests a steady setup. Analysts see some potential for gains, but most short term movement will depend on natural gas pricing and RRC’s ability to maintain consistent margins. The stock appears reasonably valued on a one year view.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

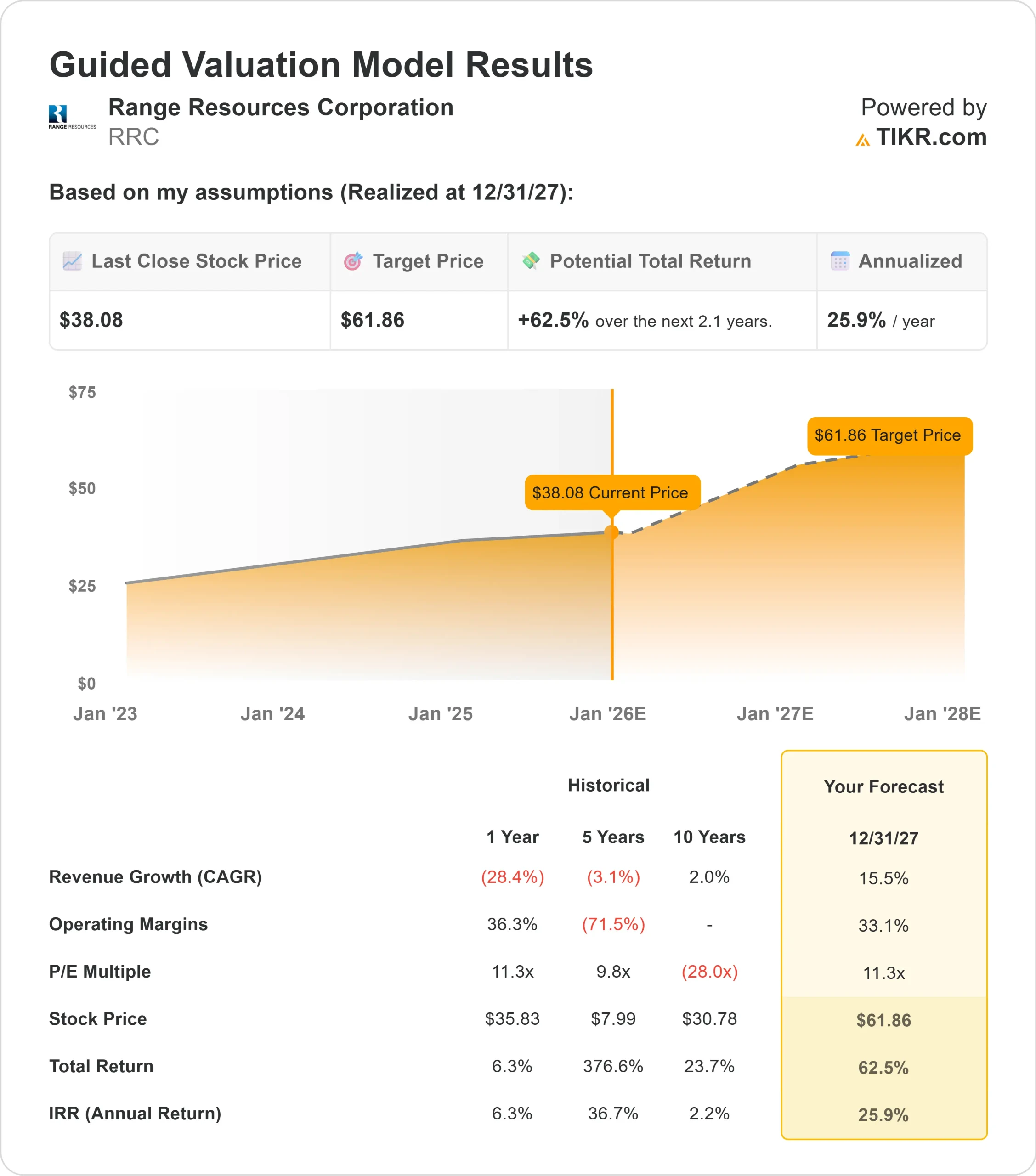

RRC Growth Outlook and Valuation

The company’s fundamentals appear solid and support a constructive long term outlook:

- Revenue is projected to grow 15.5% through 2027

- Operating margins are expected to hold near 33.1%

- Shares are valued at 11.3x forward earnings in the model

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11.3x forward P E suggests about $62/share by 12/31/27

- That implies approximately 62% upside, or about 26% annualized returns

These assumptions point to steady compounding supported by margin stability and disciplined capital allocation. The stock does not require aggressive pricing assumptions for the model to work. Instead, the outlook depends on consistent execution and maintaining today’s operating profile.

For investors, RRC screens as a more earnings driven compounder rather than a purely commodity dependent name, with long term returns shaped by stable fundamentals.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Several qualitative factors support the more constructive long term outlook. RRC continues to operate efficiently, with management keeping a tight focus on costs and disciplined capital allocation. Its asset base remains competitive, and operational consistency has helped build confidence in the company’s ability to deliver steady results.

The broader natural gas environment is also improving. As demand stabilizes and pricing becomes less volatile, RRC is positioned to capture more of the upside through its efficient operations. For investors, these strengths help create a clearer path to sustained earnings momentum.

Bear Case: Volatility and Execution Risk

Despite the positives, RRC remains sensitive to natural gas pricing. The company has experienced significant revenue swings in past years, highlighting how quickly fundamentals can change in the energy sector.

There is also execution risk. Maintaining strong margins requires continued discipline and stable production trends. If costs rise or operational performance weakens, the earnings trajectory could fall short of expectations. For investors, this means long term results depend on consistent execution in an environment that can shift rapidly.

Outlook for 2027: What Could RRC Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests RRC could trade near $62/share by 12/31/27. That represents about 62% total upside, or roughly 26% annualized returns from current levels.

While this outlook is appealing, it already assumes stable margins and consistent execution. For RRC to deliver stronger upside, the company would likely need firmer natural gas pricing or notable production outperformance. Without that, investors should expect a steady, earnings driven compounding path rather than dramatic gains.

For investors, RRC stands out as a well positioned operator with solid long term potential. The valuation suggests meaningful upside, but the strength of that upside will depend on natural gas conditions and the company’s ability to maintain operational discipline over the next two years.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>