Key Stats for PSX Stock

- Past-Week Performance: 17%

- 52-Week Range: $91 to $164

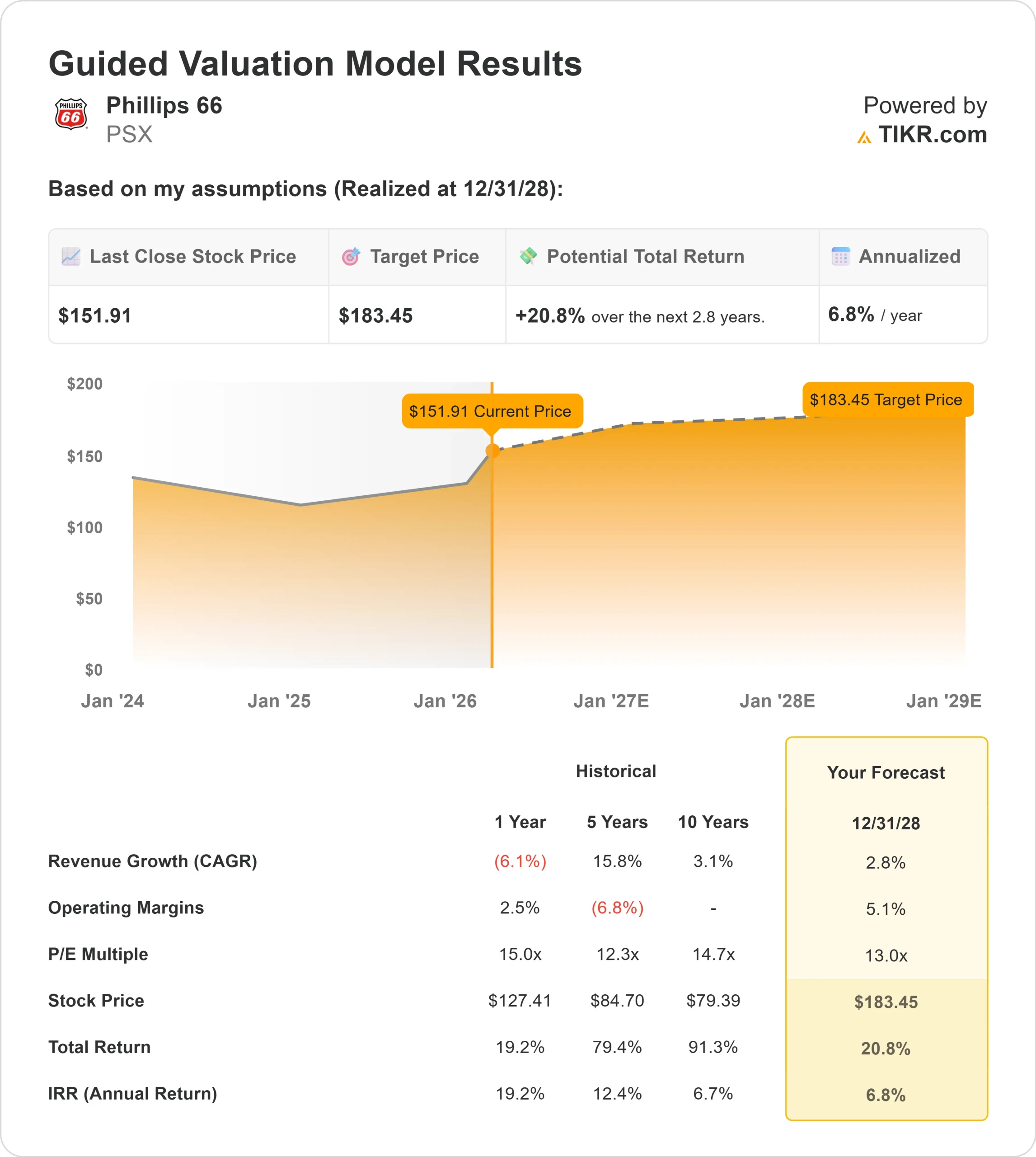

- Valuation Model Target Price: $183

- Implied Upside: 20.8%

Value your favorite stocks like Phillips 66 with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Phillips 66 stock is up about 17% over the past six months, recently trading near $152 per share as investors responded to stronger operating execution, rising Midstream visibility, and active institutional positioning.

The rally reflects growing confidence that earnings durability is improving into 2026 rather than peaking after a strong 2025.

The stock gained momentum following fourth quarter 2025 results that showed reported earnings of $2.9 billion, or $7.17 per share, and adjusted earnings of $1.0 billion, or $2.47 per share, alongside $2.8 billion of operating cash flow.

Midstream generated about $1.0 billion of adjusted EBITDA in the quarter and has increased EBITDA 40% since 2022, with management outlining a path to approximately $4.5 billion of run-rate Midstream EBITDA by year-end 2027.

CEO Mark Lashier called 2025 “a pivotal year for Phillips 66,” highlighting record NGL transportation and fractionation volumes and structural cost improvements in Refining.

Institutional activity reinforced the advance. Fiera Capital opened a new 41,651-share position valued at about $5.67 million, Stevens Capital Management initiated an 8,833-share stake worth about $1.20 million, and First National Bank of Omaha purchased 17,330 shares valued at about $2.36 million.

NEOS Investment Management increased its stake by 41.2% to 56,059 shares worth about $7.63 million, PNC Financial Services raised its holdings by 18.2% to 963,629 shares worth about $131.1 million, and Vanguard lifted its position by 11.6% to 51,724,558 shares, representing roughly 12.84% ownership valued at about $7.04 billion.

Analyst updates also drew attention. Scotiabank raised its FY2026 EPS estimate to $10.35 from $9.15 and projected FY2027 EPS of $11.95 while maintaining a $140 price target.

With institutions and hedge funds owning approximately 76.93% of the stock, earnings revisions, capital allocation execution, and Midstream growth visibility continue to influence sentiment heading into 2026.

See analysts’ growth forecasts and price targets for Phillips 66 (It’s free) >>>

Is PSX Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 2.8%

- Operating Margins: 5.1%

- Exit P/E Multiple: 13.0x

Revenue growth is expected to remain modest as refining normalizes, with incremental expansion supported by Midstream throughput growth, gas plant additions, and NGL infrastructure projects rather than unusually strong crack spreads.

Midstream execution remains a key earnings driver. The company has line of sight to approximately $4.5 billion of run-rate adjusted EBITDA by year-end 2027, supported by new gas plants, fractionation expansions, and pipeline capacity additions that diversify cash flow beyond pure refining exposure.

Refining performance is increasingly shaped by structural cost improvements and higher system utilization, including expanded crude capacity across multiple refineries and ongoing efforts to lower controllable costs toward long-term targets. These initiatives support earnings resilience even if commodity spreads fluctuate.

Capital allocation reinforces the thesis. With a secure dividend framework of roughly $2 billion annually, disciplined capital spending of about $2.4 billion, and excess operating cash flow allocated to debt reduction and share repurchases, the company maintains financial flexibility while enhancing per-share returns.

Based on these inputs, the valuation model estimates a target price of $183.45, implying about 20.8% total upside from current levels, suggesting Phillips 66 appears modestly undervalued, with 2026 performance likely driven by Midstream growth, refining reliability, and disciplined capital returns rather than aggressive top-line acceleration.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>