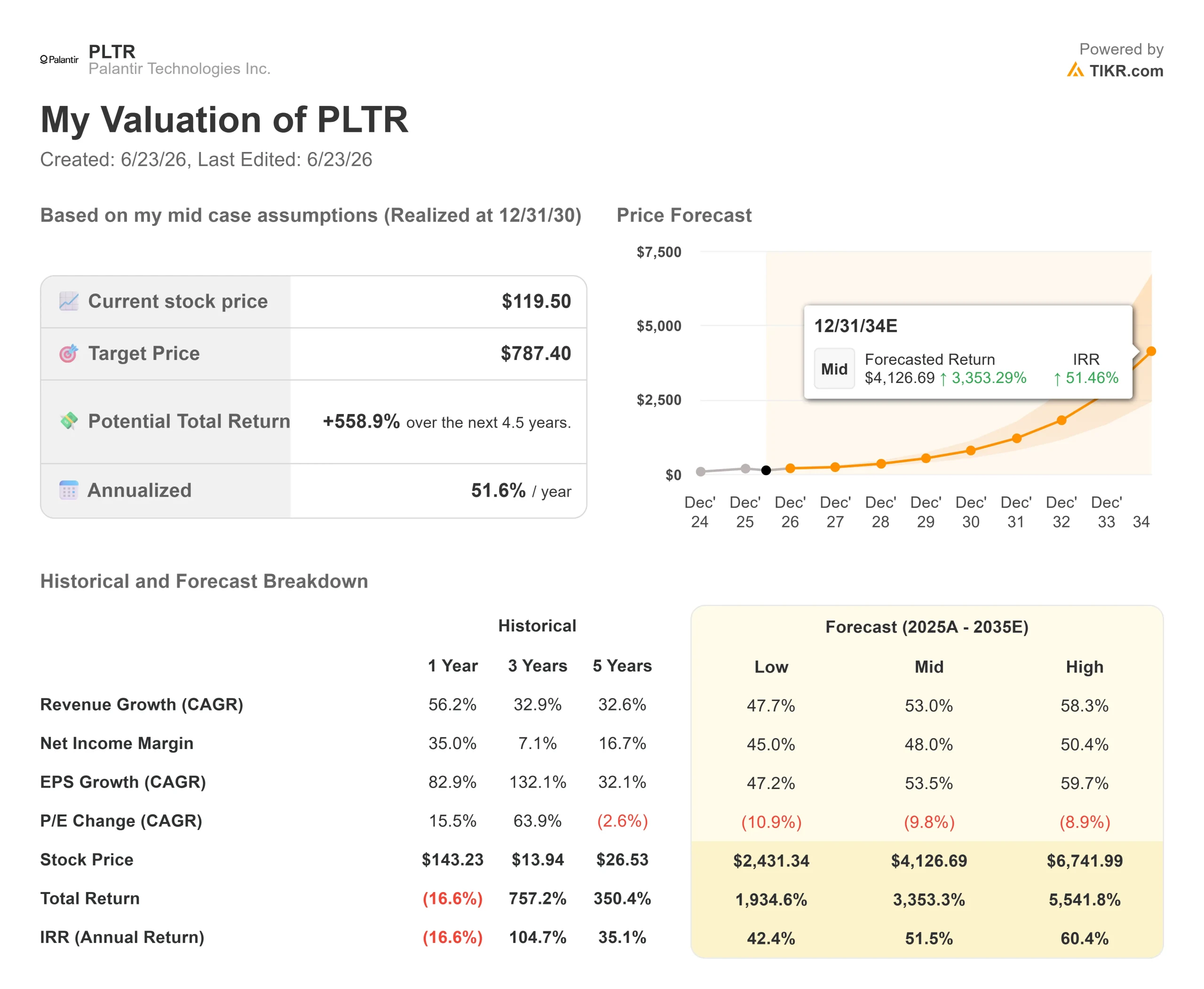

Key Stats for Palantir Stock

- Current Price: $119.50

- Target Price (Mid): ~$787

- Street Target: ~$183

- Potential Total Return: ~559%

- Annualized IRR: ~52% / year

- Earnings Reaction: -6.93% (May 4, 2026)

- Max Drawdown: 42.32% (June 22, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Palantir Technologies (PLTR) has spent all of 2026 testing the patience of the people who own it. The business keeps setting records, and the stock keeps falling. On June 22, shares dropped 6.98% to close at $119.50, leaving Palantir stock 42% below its November high of $207.52 and at its deepest drawdown in a year.

The bulls and bears have argued about valuation for months. This time, the bears have something concrete, and it is not a multiple. It is sovereignty.

On June 16, French Prime Minister Sébastien Lecornu announced that France’s domestic intelligence agency will drop Palantir’s data tools in favor of a French firm, ChapsVision. France, he said, “cannot accept new strategic dependencies in the digital sphere.” Days earlier, a UK parliamentary committee urged ministers to walk away from Palantir’s £330 million NHS contract. For a company guiding to 71% revenue growth, the question is now sharp: is Europe closing a door, or is the market pricing a regional setback as a structural break?

What Actually Happened in Europe

The French decision stings partly because of timing. Palantir renewed its three-year contract with the DGSI in December 2025, and six months later, that same agency is preparing to leave. Because the deal was just renewed, the migration is expected to take several years, which limits how fast revenue is actually at risk.

The UK situation is further along politically. Britain’s Science, Innovation and Technology Committee called Palantir’s role in NHS infrastructure an “unacceptable point of weakness” and urged the government to use a February 2027 break clause. Palantir is pushing back. UK executive vice-chair Louis Mosley called the opposition “ideologically motivated,” citing more than 110,000 additional NHS procedures since the platform went live.

That is the bear case at its sharpest: international government revenue, already the slow part of the story, now faces a coordinated political headwind. Bulls counter that Europe was never where the growth was.

The Numbers the Selloff Is Ignoring

Here is the disconnect. In Q1 2026, reported May 4, Palantir grew revenue 85% year over year to $1.633 billion, its fastest as a public company. US revenue crossed 100% growth for the first time, up 104% to $1.282 billion. US commercial revenue, the engine of the thesis, grew 133% to $595 million. The stock fell 6.93% the next day anyway.

The segment Europe threatens is the smallest piece. International commercial revenue grew just 26% to $179 million, and international government revenue grew 51% to $172 million. CEO Alex Karp told investors the real constraint is the opposite problem: “Our biggest problem currently is demand in the U.S. … we just cannot meet demand.” When a company is supply-constrained in its core market, losing a slow-growing foreign contract reads differently than it would for a business fighting for every deal.

CTO Shyam Sankar tied the AI cost collapse to Palantir’s favor. Cheaper models, he argued, mean more tasks handed to AI, which means more room for error, which is exactly what AIP, the company’s platform for running AI inside live operations, is built to govern. “More tokens means more slop,” he said. If he is right, falling model costs grow Palantir’s market rather than shrink it. That directly answers 2026’s loudest bear thesis, that commoditized AI erodes Palantir’s premium, with the quarter to back it.

See historical and forward estimates for Palantir stock (It’s free!) >>>

Where Valuation Meets the Fear

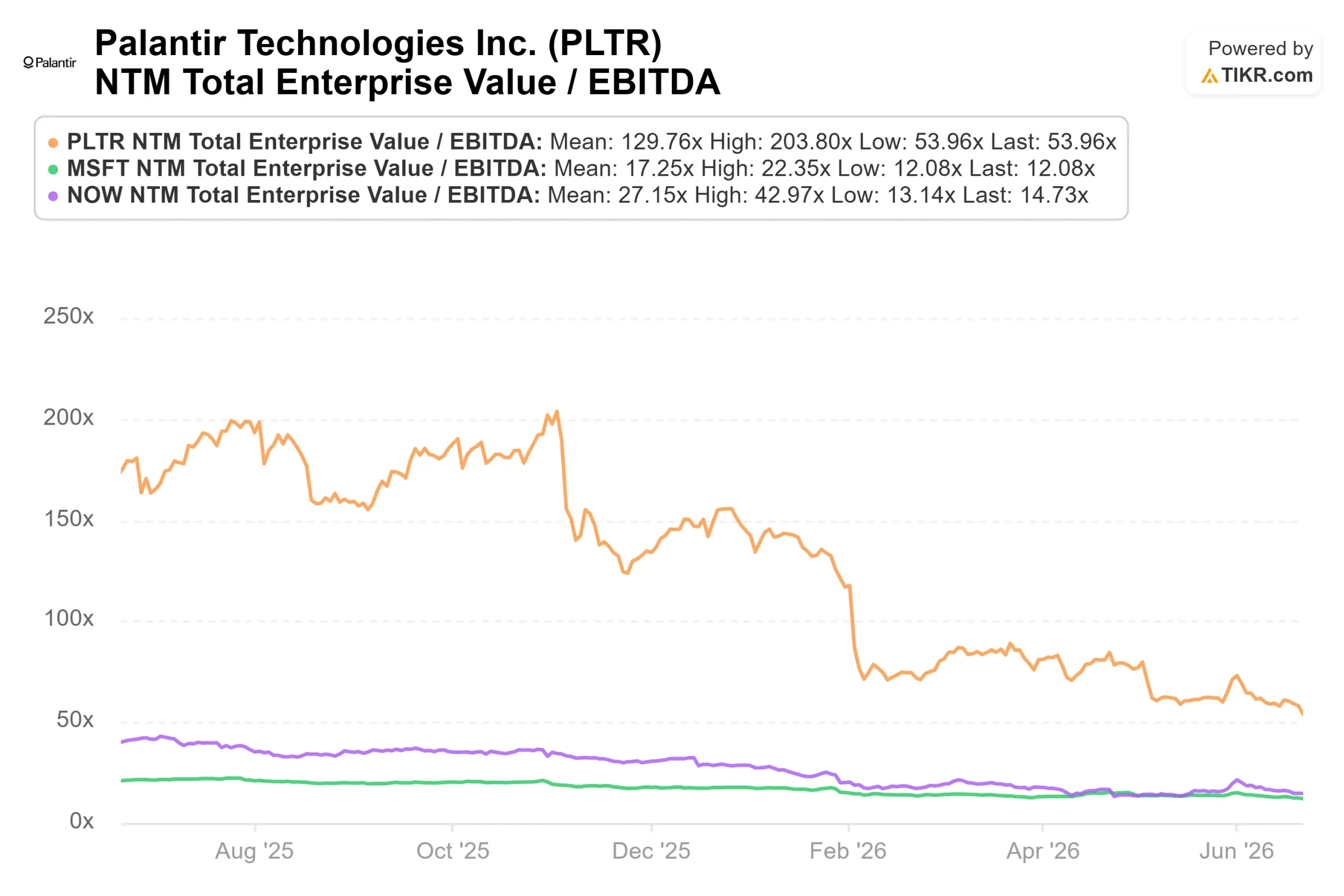

None of this makes the stock cheap, and that is where the tension lives. Even after a 42% drawdown, Palantir trades near 54x NTM EV/EBITDA and about 33x NTM revenue. Per TIKR’s Competitors page, the software peer median sits near 11x EV/EBITDA, with Microsoft at 12x and ServiceNow at 14x. Palantir’s premium is categorical, not incremental, and it only holds if US growth keeps running at a pace no peer can match. The growth rate arguably justifies the premium, but justified is not safe. A premium that large leaves no room for a US stumble.

The cash profile is what bears underweight. Palantir generated $925 million in adjusted free cash flow in Q1 at a 57% margin, and management raised full-year adjusted free cash flow guidance to $4.2 billion to $4.4 billion. A business compounding at 70%-plus while throwing off roughly $4 billion in cash is rare. The risk is not that the cash machine breaks. It is that the market keeps compressing the multiple it will pay for that cash, which is the whole story of 2026: the business has won, and the stock has lost.

See how Palantir performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $119.50

- Target Price (Mid): ~$787

- Potential Total Return: ~559%

- Annualized IRR: ~52% / year

See analysts’ growth forecasts and price targets for Palantir stock (It’s free!) >>>

The mid case is used because it captures the central debate: even if growth normalizes well below today’s pace, the math still points sharply higher from a 42%-off entry. The model rests on two revenue CAGR drivers: continued triple-digit US commercial growth as AIP converts pilots into production, and durable US government demand anchored by programs like Maven. The margin driver is operating leverage, with adjusted operating margin already at 60%. The primary risk is multiple compression: returns depend on the market sustaining a premium for years, and any US growth stumble re-rates the stock before revenue actually slows.

The upside: if US commercial holds its pace, the target of $787 is reachable. The downside: if the European backlash spreads to commercial demand or a US quarter decelerates, the premium evaporates, and the model’s far-lower low case becomes the live scenario.

Conclusion

The sovereignty story is real, but it targets the smallest part of Palantir’s business, and the migrations it threatens are measured in years, not quarters. The valuation risk is the one that can break the stock, and it is answered in the US, not Europe.

Watch US commercial revenue on the Q2 2026 earnings date, expected August 3. Management guided full-year US commercial above $3.224 billion, with at least 120% growth. With $595 million booked in Q1, the remaining quarters need to average roughly $877 million each to clear that floor. Above $750 million in Q2, and the bear thesis loses its footing. Below $550 million and the first US deceleration in over a year lands at the worst possible moment for a stock priced for perfection. The number to watch is not what France does. It is what American companies keep spending.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Palantir?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Palantir, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palantir alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Palantir on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!