Key Stats for Credo Stock

- Current Price: $302.52

- Target Price (Mid): ~$820

- Street Target: ~ $260

- Potential Total Return: ~170%

- Annualized IRR: ~23% / year

- Earnings Reaction: +1.28% (June 1, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Credo Technology Group (CRDO) closed up 11.29% on June 22, 2026, at $302.52, and the easy explanation is a fresh wave of analyst target hikes. That explanation is incomplete. The stock now trades well above the average Wall Street target of around $260, which means the analysts setting those targets are telling you, as a group, that the price has run past them. So the pop is not the story. The story is what investors are paying up to own: a company known for copper cables is building a second business in optics that management says will cross $600 million next year.

That reframes the debate. Bulls argue Credo is no longer a one-product company riding a single AI wave. Bears argue the valuation already assumes the optics business works flawlessly. The question the market cannot yet answer is whether the optical ramp arrives on management’s timeline, because that timeline separates a stock priced for greatness from one priced for perfection.

A Second Growth Engine Is Forming on Top of the First

Credo was built on active electrical cables (AECs), short copper cables with built-in signal processors that link GPUs to switches inside AI racks. That business is not slowing. What changed is what sits beside it. On May 28, 2026, Credo completed its acquisition of DustPhotonics for $750 million in cash plus stock, bringing silicon photonics (chips that move data using light) in-house.

At the Bank of America 2026 Global Technology Conference on June 4, CEO Bill Brennan said three optical lines, optical DSPs, silicon photonics chips, and ZeroFlap Optics, “will grow to more than $100 million, and all of them are growing faster than the company is growing,” totaling above $600 million. CFO Dan Fleming added that fiscal 2027 revenue should grow more than 80% while operating expenses grow roughly 50%, noting “there’s continuing leverage in the model.” A second engine scaling faster than the company, with expenses lagging revenue, is operating leverage at work.

Brennan rejected the idea that optics cannibalizes copper. “It’s going to be a heterogeneous world,” he said, because the two solve different parts of the network. He called reliability the company’s “North Star,” describing AECs as “1,000x more reliable than laser-based optics” on the no-redundancy links between GPUs and switches. Credo is selling reliability across the whole data center, not betting on one cable type winning.

See historical and forward estimates for Credo stock (It’s free!) >>>

The Valuation Question Investors Keep Circling

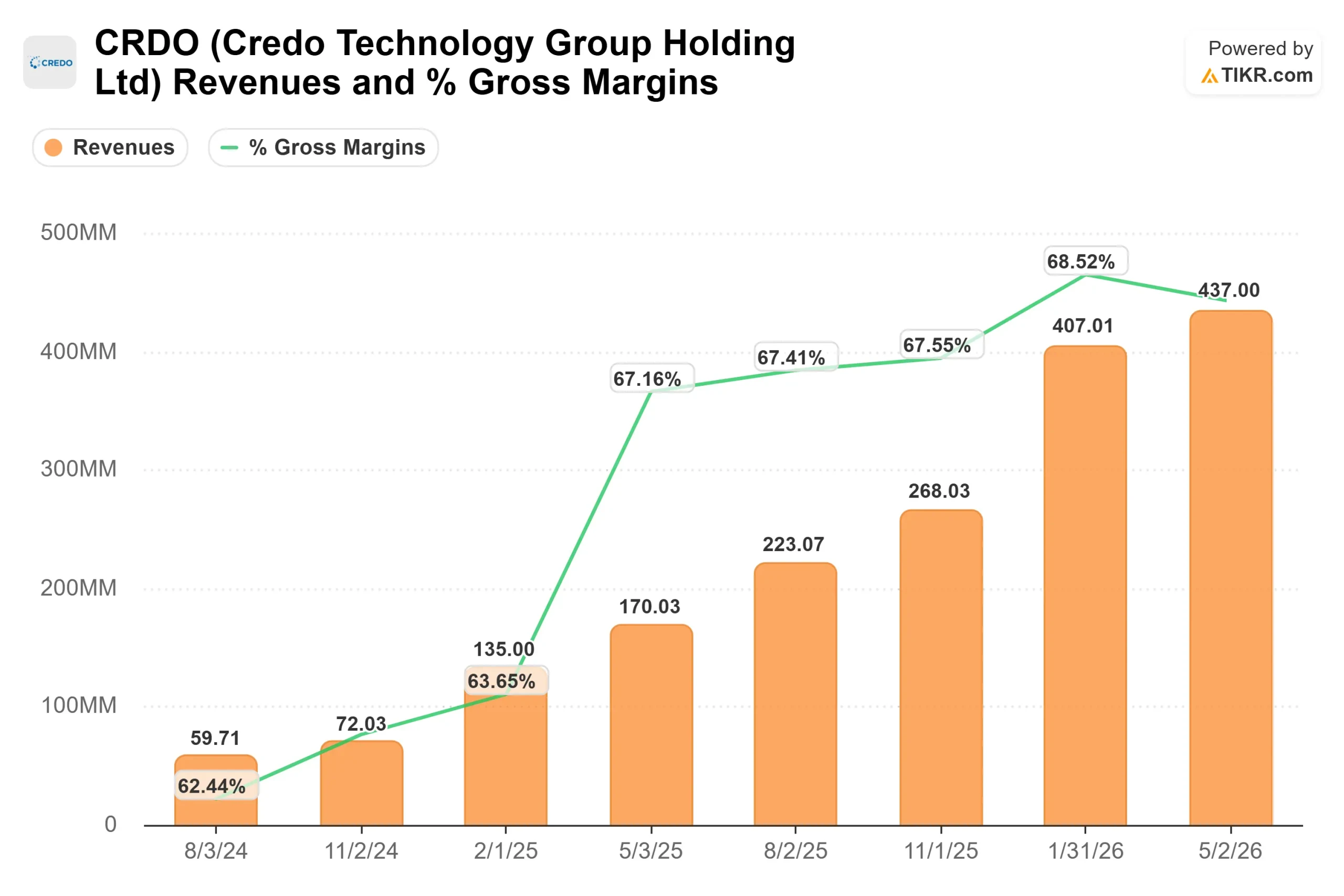

Credo’s results are not in doubt. Fiscal 2026 revenue reached $1.34 billion, up around 206% year over year, with free cash flow of $407 million and a net cash balance sheet. The debate is about price.

The premium is large. Credo trades at an NTM EV/EBITDA of around 42x, against a semiconductor peer mean of around 35x. Marvell, its closest connectivity rival, sits near 54x on the same measure, while NVIDIA trades near 17x. On forward revenue, Credo’s roughly 22x dwarfs the peer mean of near 12x. Is the premium justified? On growth, the case holds: Credo’s forward two-year revenue CAGR of around 65% is faster than any large-cap peer in the group. A company tripling revenue while holding 68% gross margins earns a multiple. The risk is that any deceleration, even from extraordinary to merely strong, compresses that multiple hard, and a stock already above its average target has little cushion if the optical ramp slips a quarter.

See how Credo performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

The TIKR Valuation Model uses the mid-case scenario, realized at fiscal year-end April 30, 2031. It points to a target of around $820, a total return of around 170% over 4.9 years, and an annualized IRR of around 23% per year from the current price.

See analysts’ growth forecasts and price targets for Credo stock (It’s free!) >>>

Two revenue drivers carry the model: AEC growth as neocloud operators broaden the customer base, and the optical inflection, where DSPs, silicon photonics, and ZeroFlap each scale past $100 million. The margin driver is operating leverage, with the model assuming a mid-case net income margin around 49%. The primary risk is customer concentration, since a handful of hyperscalers still drive most revenue, so any single deferral creates lumpiness that the multiple will punish. The upside is the optical ramp arriving on schedule; the downside is it taking longer, growth normalizing, and the premium unwinding.

Conclusion

The number that matters next is the optical mix in the fiscal first-quarter 2027 report, due September 2, 2026, with revenue guided to $465 million to $475 million. Good looks like a print above $475 million, gross margins holding in the high 60s, and management quantifying early optical revenue against the $600 million-plus goal. Bad looks like a revenue guide-down, a margin slip toward the mid-60s, or optical commentary that pushes the ramp into the second half. A stock above its average Street target does not get the benefit of the doubt twice. September tells you whether the $600 million engine is real or still a slide.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Credo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Credo, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Credo alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!