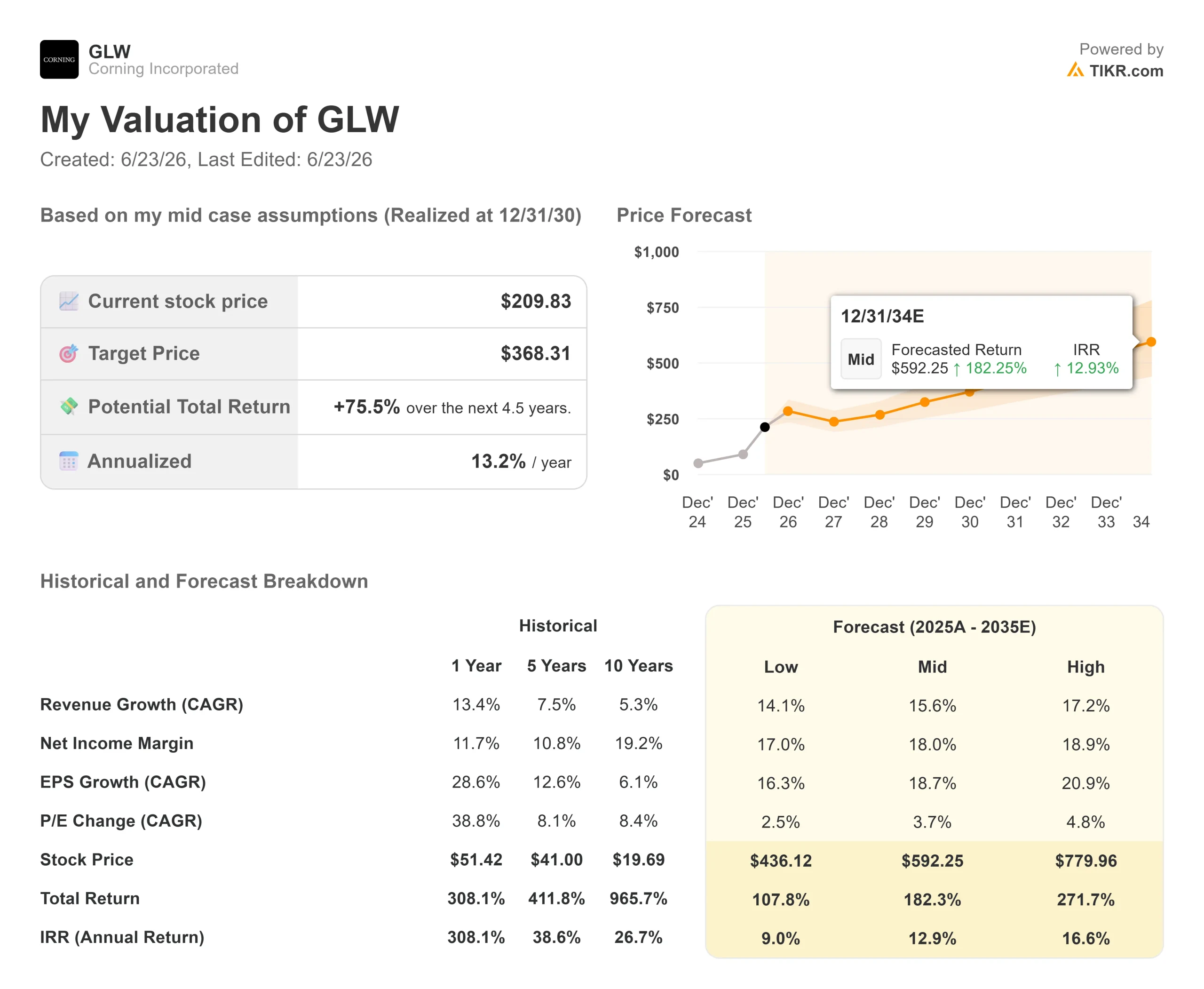

Key Stats for Corning Stock

- Current Price: $209.83

- Target Price (Mid): ~$370

- Street Target: ~$202

- Potential Total Return: ~76%

- Annualized IRR: ~13% / year

- Earnings Reaction: (0.75%) (April 28, 2026)

- Max Drawdown: 23.15% (March 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Corning (GLW) closed up 7.65% on June 22 at $209.83, near its record high. For a 175-year-old glass maker, that kind of day used to be unthinkable. In 2026, it is routine, and almost nobody argues that the business is bad anymore.

The debate has moved somewhere harder to settle. At $210, Corning stock 2026 trades at about 101 times trailing earnings and 62 times forward earnings. Those are multiples the market reserves for software, not a capital-intensive maker that pours fiber and bends glass. Bulls say the AI buildout has re-rated the company for good. Bears say a materials maker has been handed a valuation it cannot keep. The question is not whether Corning grows. It is whether it grows fast enough and turns that growth into cash cleanly enough to justify what investors already pay.

What the rally is pricing in

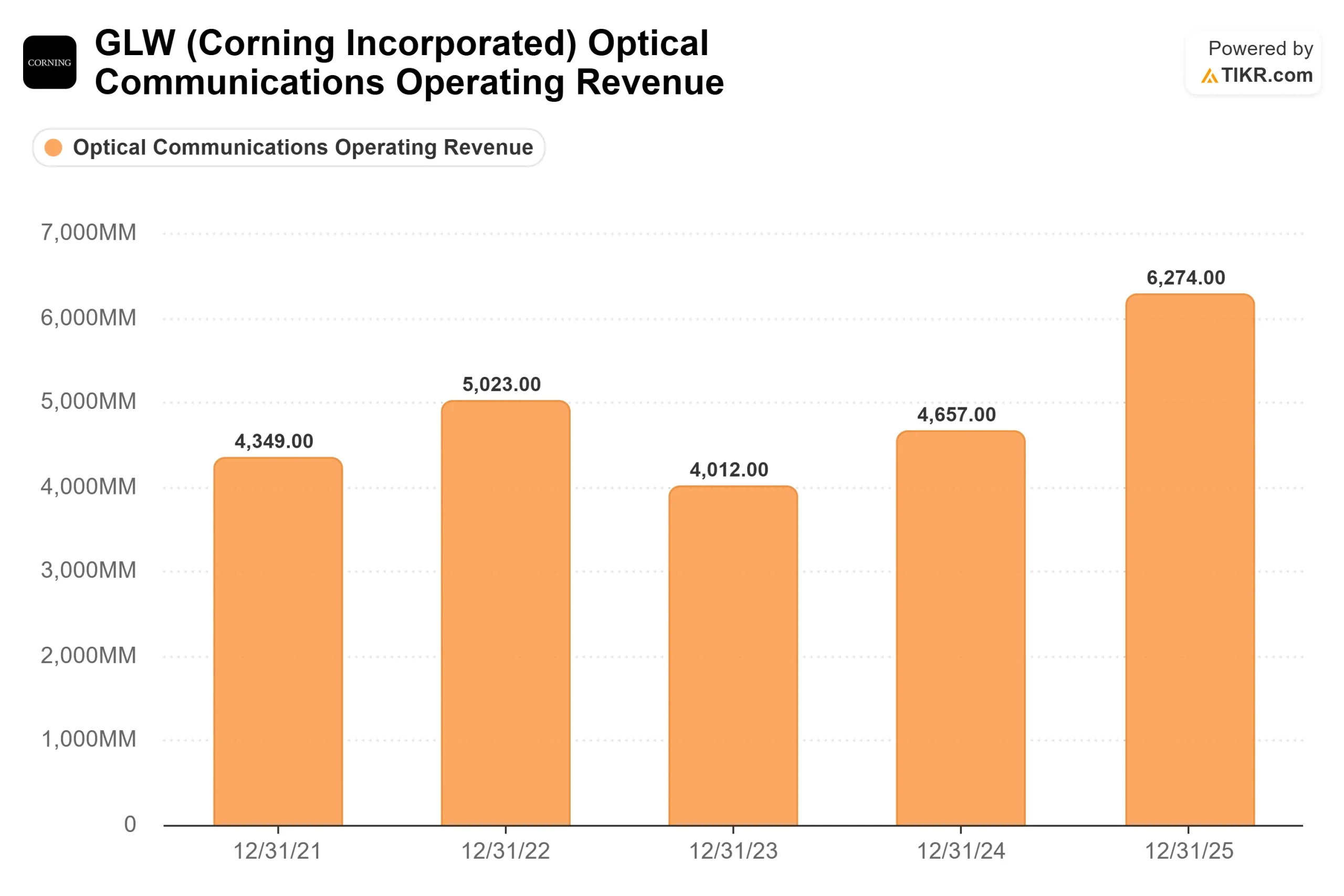

One number sits under every recent move: $40 billion in revenue by the end of 2030. Corning calls its growth plan Springboard, a framework to fill the capacity it already built and let volume drop through to margins. At the May investor event, management extended the runway to roughly a $30 billion sales run rate by 2028 and $40 billion by 2030, with a high-confidence band of $35 billion to $40 billion.

The engine is Optical Communications, which sells passive optics into data centers. The segment grew 36% year over year in the first quarter, and management expects the enterprise piece to grow at 1.3 to 1.5 times the rate of GPU growth. As clusters scale past 130,000 GPUs, the network adds a third switching layer, and Corning’s content rises with it.

See historical and forward estimates for Corning stock (It’s free!) >>>

Signatures, not just forecasts

What re-rated the stock was contracts. On June 8, Amazon agreed to a multibillion-dollar deal for Corning to supply optical fiber, cable, and connectivity for its U.S. data centers, adding 1,000 jobs in North Carolina. It followed the up-to-$6 billion Meta agreement in January and the NVIDIA partnership in May.

These are not ordinary supply contracts. CFO Edward Schlesinger explained the structure at the J.P. Morgan conference on May 19: “NVIDIA is actually providing a multibillion dollar prepayment to support that capital deployment and they’re making an equity investment.” That is the difference between a backlog and a hope. Customers fund the capacity they have agreed to fill, which lowers the risk that Corning builds plants and waits for demand.

Why the stock is still controversial

Because price has outrun proof, and the Street knows it. Analysts are split: of 15 covering the stock, 10 rate it a Buy, but 5 hold and 2 are bearish, and the average target near $202 sits just below today’s $209.83. Consensus sees the stock as roughly fairly valued, not cheap. On valuation, Corning’s 34 times forward EV/EBITDA towers over the peer group’s median of 22 times, and its 62 times forward P/E sits far above the median of 24 times. A premium can be earned. The question is whether this one is already spent.

The cash side sharpens the doubt. Corning’s free cash flow fell over the past year as capital spending climbed to fund the optical ramp, with 2026 capex estimated near $1.7 billion. A near-perfectly priced growth stock converting less profit to cash, not more, is exactly what bears point at. Management’s answer is timing. Schlesinger said most of the incremental net income “should grow faster than sales, which will convert to cash at almost 100%.” If that holds, today’s weak conversion is temporary. If it slips, the multiple has nothing to lean on.

See how Corning performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $209.83

- Target Price (Mid): ~$370

- Potential Total Return: ~76%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Corning stock (It’s free!) >>>

Two revenue drivers carry the case: enterprise optical growing above the GPU build rate as clusters add switching layers, and the carrier and photonics ramp, with early co-packaged optics expected to contribute around 2027. The margin driver is mixed, with higher-value optical products lifting net income margin toward 18%. The primary risk is timing, because the model assumes contracted capacity converts to revenue on schedule, and a premium multiple gives back the most when it does not.

The upside: optical adoption runs faster than planned, and Corning’s prepaid capacity captures it.

The downside: AI spending cools, legacy display demand stays soft, and a triple-digit trailing multiple compresses hard.

Conclusion

The deals are signed, and the prepayments are real. What is unproven is whether revenue and cash arrive fast enough to justify a price that already assumes they will. The test comes with second-quarter earnings, expected in late July. Watch the Optical Communications growth rate. It grew 36% last quarter, and a print holding in the low-to-mid 30s would confirm the contracts are converting on schedule. A clear slowdown, paired with another light free-cash-flow quarter, would say the June surge ran ahead of the fundamentals. At 101 times earnings, Corning does not get the benefit of the doubt for long.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Corning?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Corning, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Corning alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Corning on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!