Key Takeaways for Formula One Group Stock as of June 2026

- Analysts rate Formula One Group stock 11 Buys, 3 Outperforms, and 2 Holds, with a street mean target of $115 and a high target of $135, implying 29% and 51% upside respectively from the current price of $89.

- TIKR’s mid-case model values Formula One Group at $165 by December 2030, implying 84% total return from current levels, or 14% annualized over 4.5 years.

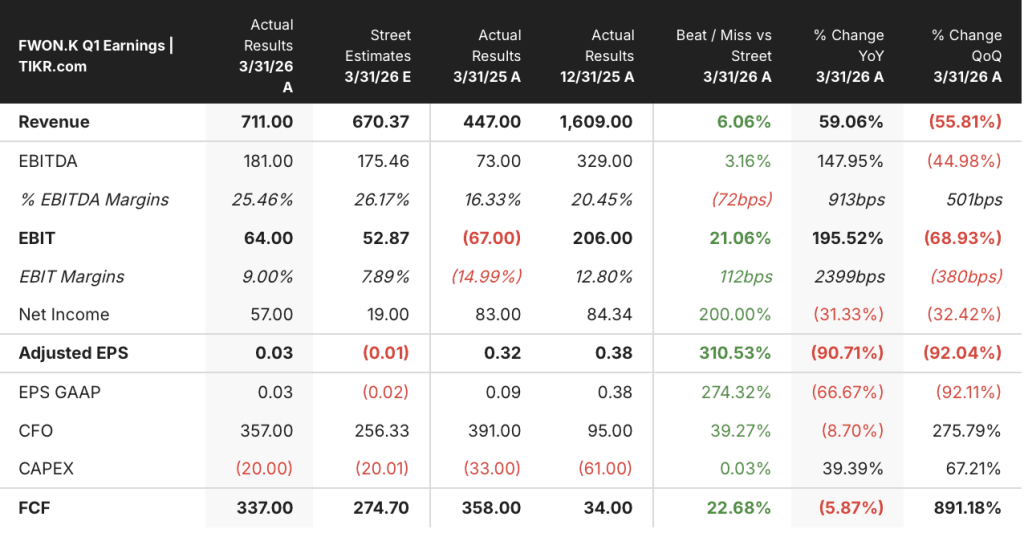

- Formula One Group stock beat Q1 2026 revenue estimates by 6%, posting $711 million against a $670 million consensus, as adjusted OIBDA more than doubled year over year to $181 million, yet the market is pricing a 22-race 2026 calendar as a structural impairment rather than a temporary disruption.

Formula One Group Stock Beat Q1 Estimates by 6% but the Market Is Pricing the Wrong Risk

Formula One Group (FWONK), the Liberty Media tracking stock that holds commercial rights to the FIA Formula One World Championship and MotoGP, reported Q1 2026 revenue of $711 million, up 59% year over year and ahead of the $670 million consensus estimate by 6%, following the Q1 earnings call.

Three races ran in Q1 2026 versus two in Q1 2025, with Japan added to the current-year period, and that calendar shift drove outsized recognition of season-based media rights and sponsorship revenue across every stream.

CFO Brian Wendling explained the mechanics directly on the Q1 call: “Revenue grew 53%. Adjusted OIBDA grew 102% driven by the extra race held and growth across all revenue streams from underlying contractual fee increases.”

Adjusted OIBDA reached $181 million for the quarter, more than doubling from $73 million in Q1 2025 and clearing the $175 million street estimate, as revenue growth outpaced the increase in team payments.

Formula One Group stock’s OIBDA margin expanded to 25%, up from 16% in Q1 2025, demonstrating the operating leverage that flows through the model when race count and contracted fee escalators align.

Sponsorship was a standout driver, with new partners including Standard Chartered, FanDuel, and Marsh added in the quarter, and CEO Derek Chang noted on the May 19 JPMorgan TMT conference that sponsorship revenue grew roughly 30% in 2025, with the renewal cycle running ahead of expiry dates as partners come back early.

The Bahrain and Saudi Arabian Grands Prix were cancelled in April due to the Middle East conflict, reducing the full-year 2026 calendar to 22 races from 24 in 2025, and management flagged Q2 as the most structurally impaired quarter with only five races expected versus nine in Q2 2025.

Formula One Group stock fell from near $109 in January to as low as $80 on the race cancellations, and at $89 it sits 18% below its 52-week high, with the market pricing that impairment as durable rather than calendar-driven.

Chang also said on the Q1 call: “While that creates a near-term financial impact, it does not change our confidence in the long-term trajectory of this sport.”

Management simultaneously locked in multiyear commercial infrastructure across the quarter, including a five-year Sky broadcast extension covering the UK through 2034 and Italy through 2032, a Las Vegas Grand Prix contract extended to 2037, the Turkey Grand Prix return from 2027 under a new five-year agreement, the Fever ticketing platform partnership from 2027, and a Pirelli tyre supply extension to 2028.

That commercial activity is what makes the current price compelling. Formula One Group stock is trading on a 22-race 2026 calendar while the contracts being signed lock revenue through the early 2030s.

Wall Street Stays Structurally Bullish on Formula One Group Stock Despite the 2026 Calendar Headwind

Wall Street is not treating the 22-race 2026 calendar as a thesis-breaker for Formula One Group stock.

Of the 16 analysts covering Formula One Group stock, 11 rate it a Buy, 3 rate it an Outperform, and 2 rate it a Hold, with no Underperforms or Sells in the count, a distribution that reflects structural conviction rather than cyclical optimism about a single quarter.

The mean price target of $115 against a current price of $89 implies 29% upside, and the street high of $135 implies 51%, a spread that reveals where bulls and bears sit on the magnitude of the recovery, not whether one happens.

Formula One Group stock’s Q1 2026 revenue trajectory makes that positioning legible, with the $711 million actual reading representing 59% growth year over year, and Q2 2026 consensus estimates of around $970 million reflecting the mechanical recognition of a five-race quarter rather than any deterioration in the underlying commercial base.

Q3 2026 consensus estimates of around $1.24 billion represent 14% year-over-year growth even on a reduced calendar, with Q4 estimated at around $1.76 billion, a 9% gain that reflects the Concorde Agreement’s contractual fee escalators and the accumulated sponsorship additions.

EBITDA tracked the same direction, with Q1 2026 adjusted OIBDA reaching $181 million against a $175 million estimate, a 148% year-over-year increase, and consensus projecting around $250 million for Q2 and around $360 million for Q3, confirming that margin leverage remains intact even at reduced race counts.

Deutsche Bank trimmed its price target to $105 from $110 in early June and maintained its Buy, a target reduction that reflects the calendar math rather than any change in the long-term commercial thesis.

The 14 Buys and Outperforms against 2 Holds reflect a concrete split, where the Buy camp treats the 22-race 2026 calendar as a timing disruption the contracted revenue base will absorb, while the Hold camp wants proof that Q2’s five-race impairment does not widen through any further Middle East cancellations before upgrading conviction.

Is Formula One Group Stock Undervalued in 2026? TIKR’s $165 Model Says Yes

TIKR’s mid-case model values Formula One Group stock at $165 by December 2030, implying 84% total return from the current price of $89, or 14% annualized over 4.5 years.

The TIKR model is not pricing the 2026 race count. It is pricing the rights base and the commercial architecture that Formula One Group stock has been assembling throughout this impaired year.

The Sky broadcast extension to 2034 and 2032, the Apple TV partnership in its first full U.S. season, the Las Vegas contract to 2037, and the Fever ticketing platform from 2027 all lock in revenue streams that extend well beyond the current calendar disruption, and each of those deals arrived while the stock was trading near its 52-week low.

Formula One Group stock is undervalued at current levels. The TIKR model assumes around 7% annual revenue growth through the period, a deliberately conservative assumption against the 22.7% one-year trailing rate and the 31.4% five-year CAGR, meaning the target does not require any acceleration from the commercial base already in place.

Should You Invest in Formula One Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Formula One Group stock and you will see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Formula One Group alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FWONK stock on TIKR for Free →