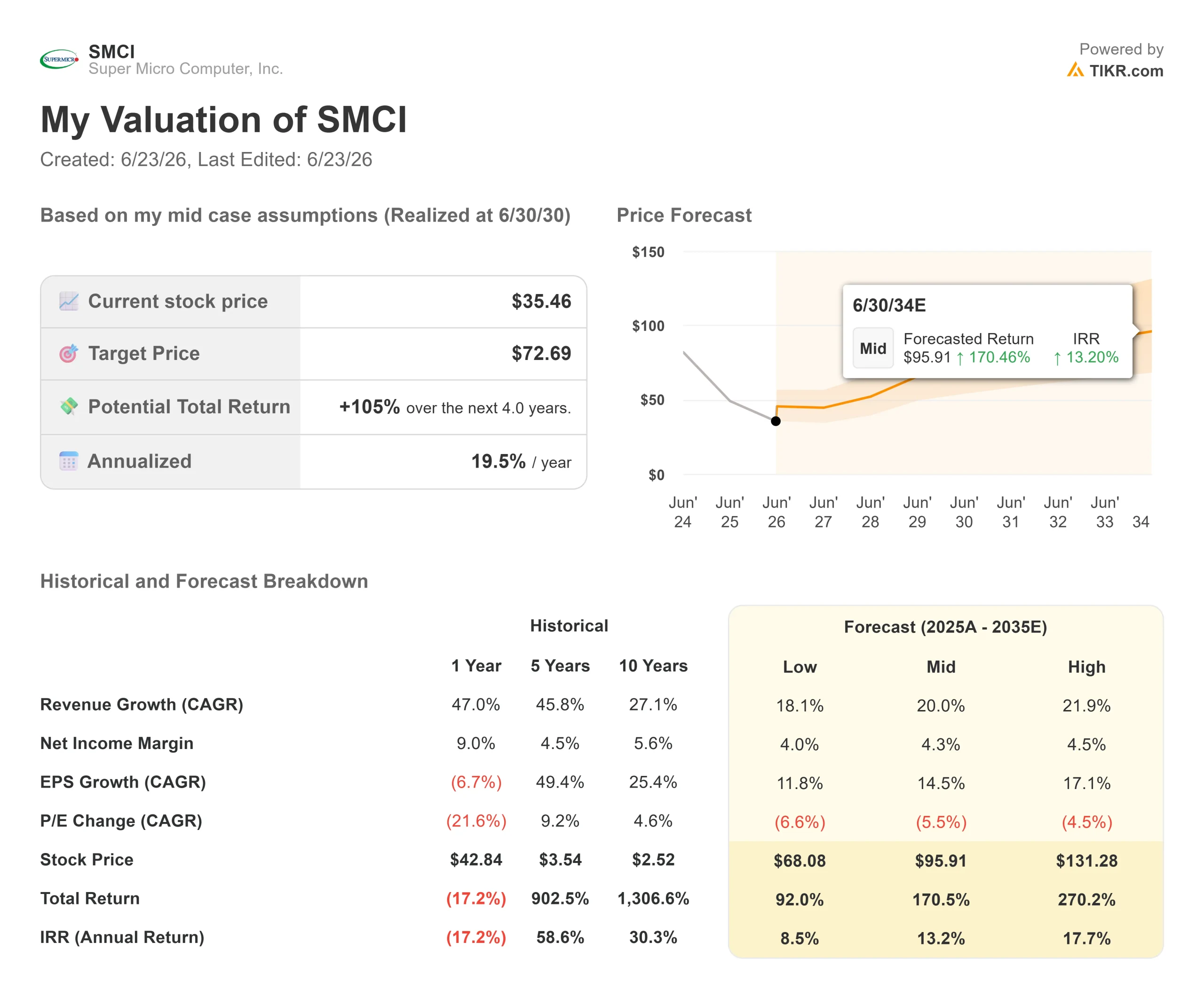

Key Stats for Super Micro Stock

- Current Price: $35.46

- Target Price (Mid): ~$73

- Street Target: ~$37

- Potential Total Return: ~105%

- Annualized IRR: ~20% / year

- Earnings Reaction: +24.54% (5/5/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Super Micro Computer (SMCI) finally got the one thing its rebound was missing. For weeks, the stock had bounced without a single analyst willing to back it. On June 22, 2026, one did. GF Securities upgraded SMCI from Hold to Buy, and the stock closed up 15.66% at $35.46, a one-day gain of $4.80.

That matters because it signals a turn in sentiment, not just price. SMCI spent most of 2026 absorbing downgrades as governance and margin worries piled up, so the first upgrade in months is a real crack in that consensus. The question now: is the Street starting to come around, or is one firm calling a bottom too early?

Why one upgrade moved the stock so much

The upgrade did not arrive alone. The same morning, Super Micro unveiled a Vera Rubin NVL4 data center blueprint at the ISC 2026 conference in Hamburg. It is built on Nvidia’s newest GPU platform and scales to 1,152 Nvidia Rubin GPUs in liquid-cooled racks, with deployments planned for the second half of 2026. A named, scheduled roadmap tied to Nvidia’s next chip generation pushes back directly on the fear that SMCI’s growth might stall.

GF Securities analyst Jeff Pu argued the recent selloff went too far. His $48 target implies more than 55% upside from the level shares traded at when the note dropped. Pu’s view is that the company’s $7 billion capital raise removed an overhang rather than created one, because it funds the components needed to deliver a roughly $39 billion AI server backlog. The stock had fallen close to 28% after that raise, so the upgrade reframed the same event as a reason to buy.

The margin debate that decides the stock

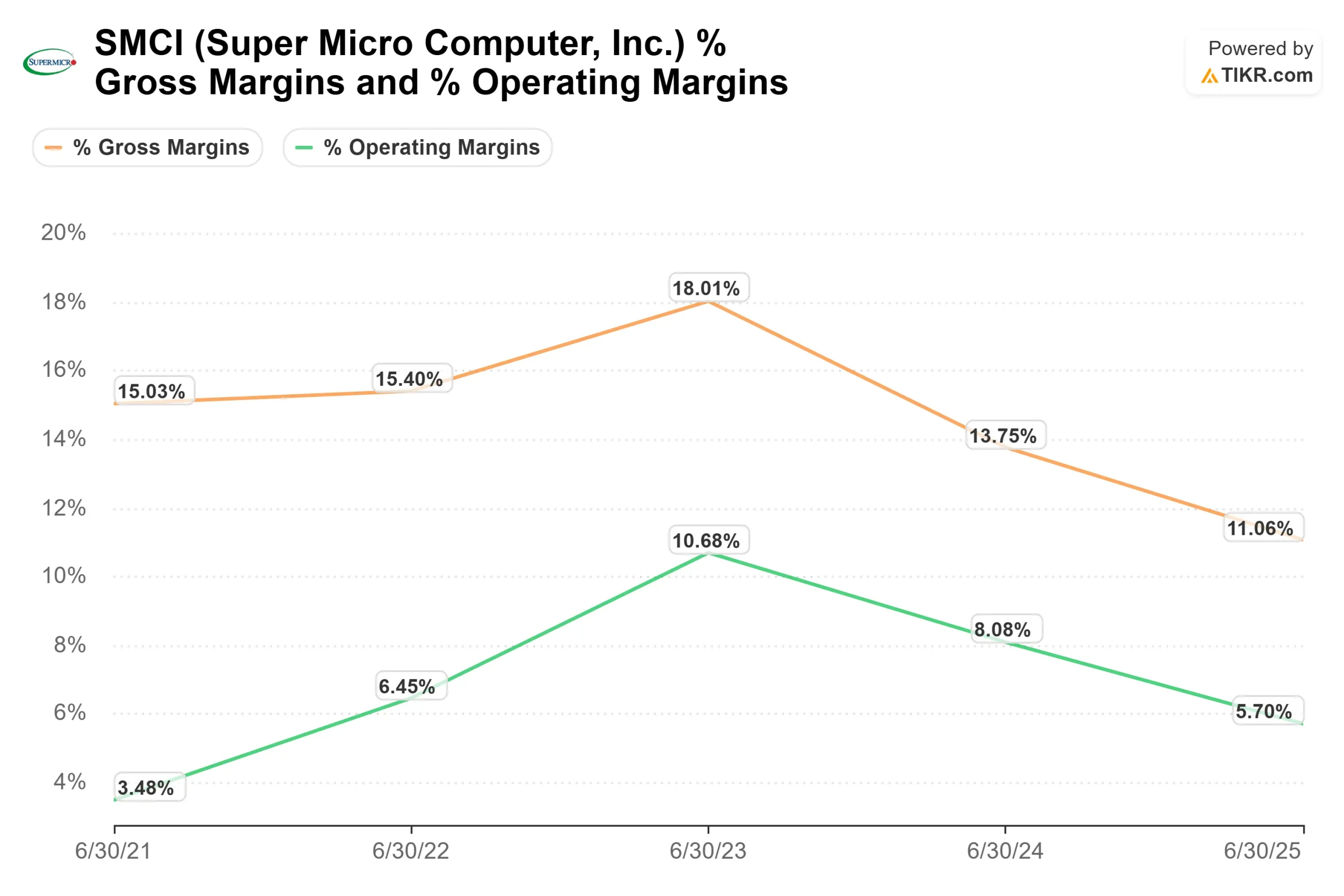

The real argument is about profit, and management keeps making it directly. At the Bank of America Global Technology Conference on June 2, Michael Staiger, Senior Vice President of Corporate Development, described the company’s full data center packages as “margin accretive” and said SMCI is “working on getting to a higher margin run rate as we exit the calendar year and into ’27.” That is the crux of the bull case: selling complete systems rather than bare servers should lift profit per deal.

The skeptic’s rebuttal sits in the numbers. Gross margin ran at just 8.4% over the trailing twelve months, a thin cushion for hardware scaling this fast. Few doubt SMCI can grow revenue. The doubt is whether that revenue turns into durable profit.

See historical and forward estimates for Super Micro stock (It’s free!) >>>

Cheaper than its peers, for reasons that are fading

The valuation gap is hard to ignore. SMCI trades at roughly 0.63 times next-twelve-months (NTM) enterprise value to revenue and about 12 times forward earnings. Dell sits near 1.70 times revenue and 23 times forward earnings, and Hewlett Packard Enterprise near 1.65 times and 13 times, per TIKR’s Competitors page. SMCI grows faster than both, yet trades at a fraction of their revenue multiples.

That gap has a clear source. In March 2026, the Department of Justice unsealed an indictment charging three individuals formerly tied to Supermicro, including co-founder Yih-Shyan “Wally” Liaw, with conspiring to divert AI servers with restricted Nvidia GPUs to China. The company itself was not named as a defendant. An independent, board-led investigation continues, and Staiger said on June 2 he expected it to wrap up “in reasonable short order.” Until it closes, part of the discount is simply unresolved risk being priced in.

The last earnings report gave bulls a foothold. On May 5, the stock jumped 24.54% in a session as gross margin beat fears, even though revenue of $10,243.01 million missed the $12,454.20 million consensus. Adjusted earnings of $0.84 beat the $0.62 estimate. Management blamed the revenue shortfall on customers lacking the power and networking to accept shipments on time, not on weak demand.

See how Super Micro performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $35.46

- Target Price (Mid): ~$73

- Potential Total Return: ~105%

- Annualized IRR: ~20% / year

See analysts’ growth forecasts and price targets for Super Micro stock (It’s free!) >>>

This is the mid case, used because it sits between a low case, still worth around 92% total return, and a high case near 270%, so it frames the base expectation rather than the best outcome. Two revenue drivers anchor it: AI server demand feeding the roughly $39 billion backlog, and the shift toward fuller rack-scale deployments that carry more content per order. The margin driver is a higher gross margin run rate, with mid-case net income margin modeled around 4%. The primary risk is margin durability: if gross margin stalls near 8%, the earnings power never arrives.

The upside is straightforward: SMCI holds around 20% revenue growth, margins climb as full-system sales scale, and the multiple rerates as the legal cloud lifts. The downside is just as clear: margins stay compressed, the new shares weigh on per-share value, and the governance overhang lingers.

Conclusion

One upgrade does not settle the debate, but it points to where the answer lives. GF’s $48 target sits above the Street’s mean near $37 and well below TIKR’s roughly $73 mid-case, so the gap between bull and bear is unusually wide. The number that narrows it is gross margin, reported when SMCI posts fiscal Q4 in August 2026. A step toward double digits confirms the margin story and likely pulls more analysts off the sidelines. A slip back toward 8% hands the bears their proof and stalls the rerating. August is when the question gets an answer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Super Micro?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Super Micro, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Super Micro alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Super Micro on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!