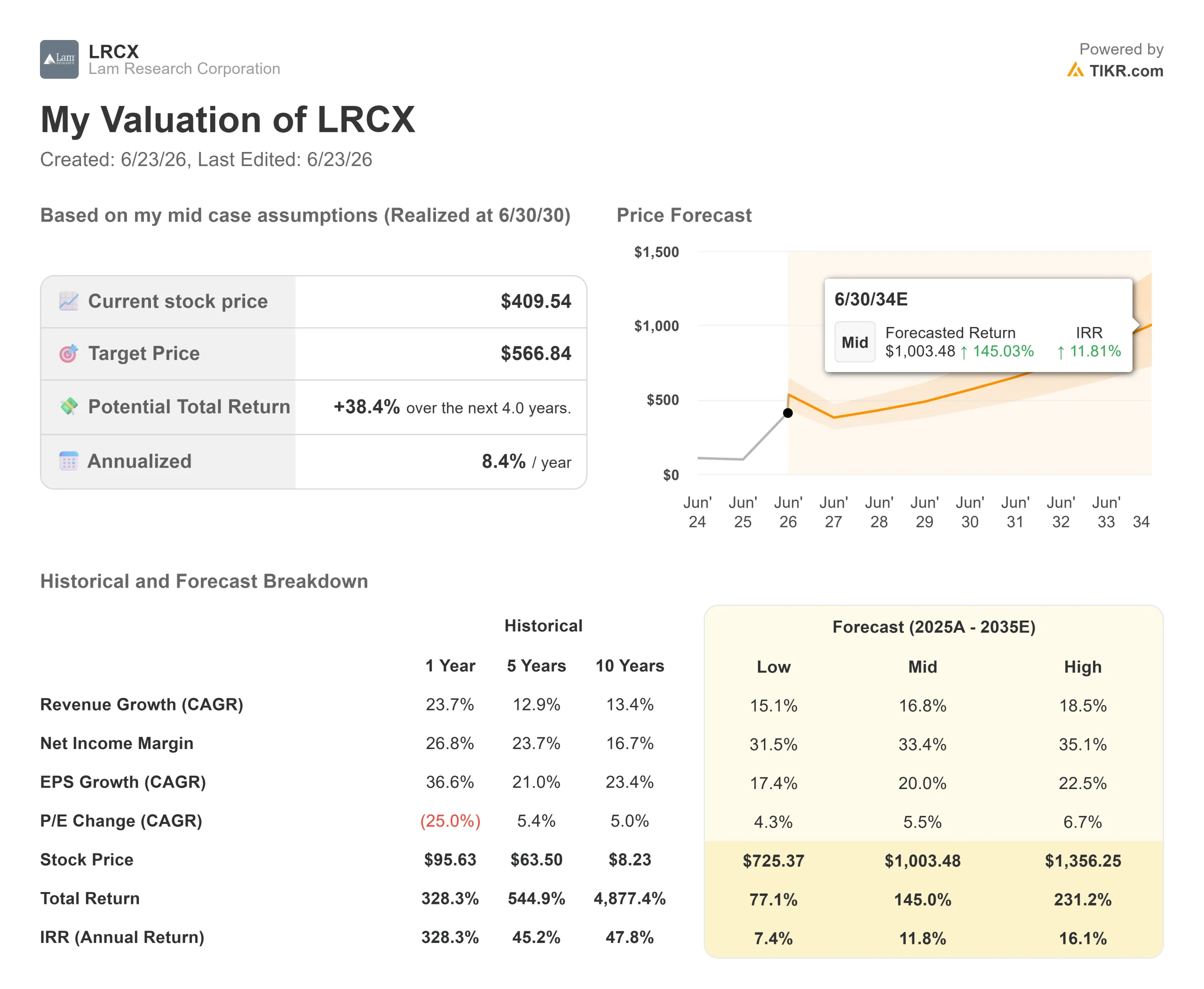

Key Stats for Lam Research Stock

- Current Price: $409.54

- Target Price (Mid): ~$570

- Street Target: ~$340

- Potential Total Return: ~38%

- Annualized IRR: ~8% / year

- Earnings Reaction: (2.63%) (April 22, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lam Research Corporation (LRCX) closed at a record $409.54 on June 22, up 5.27% on the day. That sets up the odd tension in this stock. The price keeps printing new highs, yet the open question is no longer whether Lam is a great business. It is whether there is room left above $400 after a year-to-date run that several outlets peg near 139%.

Monday’s move had a clear trigger. Wells Fargo raised its target to $450 from $365 and kept an Overweight rating, citing a higher forecast for wafer fabrication equipment (WFE), the tools chipmakers buy to build chips, in 2027 and 2028.

The Street spent two weeks catching up to the stock

That call was not alone. In early June, Lam already traded above consensus, and the bulls answered with target hikes. Citi went to $450 from $315 on June 17, Oppenheimer to $400, Cantor to $425, and Barclays to $335. Each raise chased a price that had already moved.

That matters for anyone buying today. TIKR data puts the mean Street target near $340, about 18% below Monday’s close. Even the new $450 high implies only roughly 10% upside over the next year. When the most bullish target on Wall Street offers low-double-digit upside, the easy repricing is likely behind us.

See historical and forward estimates for Lam Research stock (It’s free!) >>>

The business underneath the price is firing on every cylinder

None of this is a knock on the company. Lam’s March 2026 quarter set a record: revenue of $5.84 billion, up 24% year over year, and adjusted EPS of $1.47, above the top of guidance, marking another quarterly revenue beat. Foundry, the contract manufacturing of chips for other firms, made up 54% of systems revenue. The Customer Support Business Group (CSBG), Lam’s recurring service and spare-parts arm, crossed $2 billion in a quarter for the first time.

That recurring base is easy to underrate. On the Q3 FY2026 earnings call, CFO Douglas Bettinger said CSBG is “my favorite part of the business model.” Fabs run around the clock and consume spares and service whether or not anyone buys new tools. Bettinger noted industry utilization is running near 100%, which keeps that engine hot.

Why Bettinger sounded more bullish than usual

The bigger signal came at the Bank of America Global Technology Conference on June 2. Bettinger, a conservative voice, said customer conversations were “as strong as I’ve ever seen it, frankly, in all the time I’ve been in the industry.” For a CFO who picks words carefully, that is close to a maximum-confidence statement, and it explains why the demand story held through the rally.

The structural reason is simple. As Bettinger put it, “When things inflect in the third dimension, etch and deposition intensity grows. That’s all we do.” Gate-all-around transistors, taller NAND stacks, high-bandwidth memory (HBM, the stacked DRAM that feeds AI accelerators), and through-silicon vias in advanced packaging all push chip structures vertically. Each step adds more of exactly the work Lam’s tools perform. Management raised its 2026 WFE outlook to around $140 billion and expects 2027 to grow again as clean-room capacity frees up.

The risk the rally is choosing to ignore

One problem the upgrade wave has talked about is China. TIKR’s segment data shows China generated about $6.2 billion of Lam’s fiscal 2025 revenue, roughly 34% of the total. In late April, the U.S. Department of Commerce ordered Lam and its peers to halt shipments of certain tools to Hua Hong, China’s second-largest chipmaker. That is a direct restriction on a meaningful slice of revenue, and export rules have only tightened over time.

So the picture is two-sided. On one side: the clearest AI-capex beneficiary in equipment, a recurring revenue engine, and a CFO sounding the most optimistic of his career. On the other: a stock at 54x forward earnings, trading above its own consensus, with about a third of revenue exposed to a policy lever Washington can pull again.

How the valuation compares to peers

On forward earnings, Lam trades at 54.49x next-twelve-months P/E, above tool peer Applied Materials at 43.44x and near KLA at 56.54x. On NTM EV/EBITDA, Lam sits at 46.48x versus 37.03x for Applied Materials and 46.81x for KLA. The premium to Applied Materials is defensible given Lam’s leadership in etch and its exposure to the memory and packaging inflections driving this cycle. But it is a premium, not a discount, so the market is already paying up for Lam’s positioning rather than offering it cheaply.

See how Lam Research performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $409.54

- Target Price (Mid): ~$570

- Potential Total Return: ~38%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for Lam Research stock (It’s free!) >>>

On the mid-case, TIKR’s model points to a target of around $570 by mid-2030, a total return of about 38% over four years, or roughly 8% per year. That is positive but modest, and the reason is the entry price. The business keeps executing while the starting multiple works against the buyer.

Two drivers carry revenue: continued WFE growth from AI-driven foundry and leading-edge logic, and the memory recovery in DRAM and HBM as 3D structures lift Lam’s content per wafer. The margin driver is the recurring CSBG mix plus pricing discipline, with gross margin guided near 50%. The mid-case assumes a revenue CAGR of around 17% and a net income margin near 33%.

The primary risk is China, where a wider export-control freeze on roughly a third of revenue would pressure both growth and the multiple.

The upside case: AI capex stays unconstrained into 2027, and Lam’s share gains push results to the high end.

The downside case: a China shock or memory pause turns an 8% annual return flat or negative from here.

Conclusion

The next real test is Lam’s fiscal Q4 report, expected in late July. Management guided to $6.6 billion in revenue and EPS of $1.65 with a 50.5% gross margin. Hitting that confirms the demand bulls are paying for. The number that will move the stock, though, is China. Watch the commentary on the Hua Hong restrictions and any change to the China revenue mix. Clean guidance with no China downgrade keeps the premium intact. Any cut to the second-half outlook does not. You will know by the end of July.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lam Research?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lam Research, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lam Research on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!