Key Takeaways for Zscaler Stock as of June 2026

- Analysts rate Zscaler stock 31 Buys, 8 Outperforms, and 8 Holds with a street mean target of $193, implying 56% upside from the current price of $124.

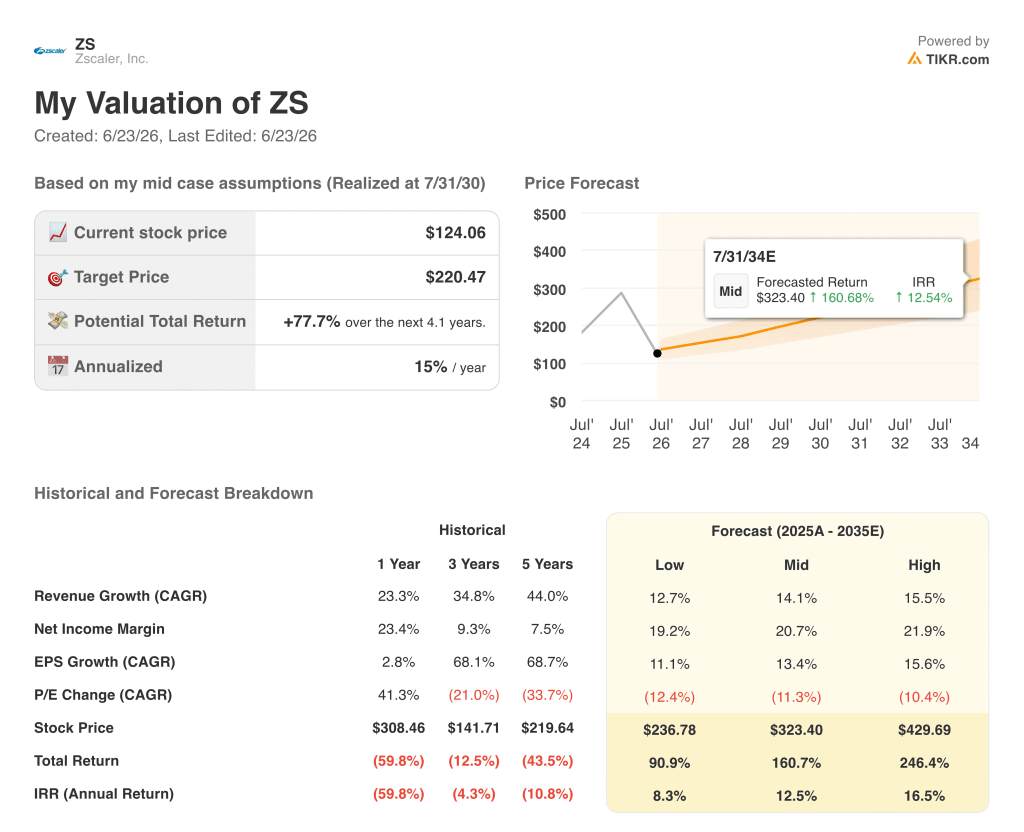

- TIKR’s mid-case model values Zscaler at $220 by July 2030, implying 78% total return from current levels, or 15% annualized.

- Zscaler stock fell 31% on May 27 despite Q3 revenue of $850.5 million beating the Street’s $835.4 million estimate, after management guided Q4 revenue of $875 million to $878 million below consensus and disclosed two senior sales leadership departures.

Zscaler Stock Fell 31% on a Beat: What the Market Is Getting Wrong About ZS

Zscaler (ZS) fell 31% on May 27 after reporting Q3 fiscal 2026 revenue of $850.5 million, a $15 million beat on estimates, and non-GAAP EPS of $1.08, a $0.07 beat, because management’s Q4 revenue guide of $875 million to $878 million landed just below the Street’s $878.6 million estimate.

Two senior sales leaders under Chief Revenue Officer Mike Rich departed at the close of Q3, and management cited the transitions as a reason for taking a prudent approach to Q4 guidance, which amplified the market’s reaction.

The Q3 result itself was operationally clean: ARR grew 25% year over year to $3.525 billion, net new ARR of $166 million came in 24% above the prior-year quarter, and the remaining performance obligation of approximately $6.5 billion grew roughly 30%.

Non-GAAP operating margin reached an all-time high of 23%, a 140-basis-point improvement year over year, as sales and marketing leverage drove the expansion.

Zscaler also guided full-year ARR to $3.740 billion to $3.749 billion, reflecting roughly 24% growth, and raised its full-year revenue outlook to $3.3295 billion to $3.3325 billion, up from prior guidance of $3.309 billion to $3.322 billion.

The free cash flow margin outlook fell from 26.5% to 27% to 22.8% to 23.3%, driven by a decision to pull forward data center equipment purchases into Q4 ahead of expected hardware cost increases, taking fiscal 2026 capital expenditure to the high single digits as a percentage of revenue.

CEO Jay Chaudhry cited a direct tailwind from Anthropic’s Mythos frontier model, which enterprises report finds vulnerabilities at machine speed, generating urgent inbound demand for Zscaler’s core Zero Trust architecture: “Zero Trust has never been more important before.”

Management guided preliminary fiscal 2027 ARR and revenue growth of 16% to 17%, a deceleration that reflected new logo conservatism and uncertainty around the pace of uptake for the integrated Red Canary SecOps platform, not fundamental deterioration in the installed base.

Zscaler Stock Analyst Targets Hold at $193 Mean Despite the Selloff: The EPS Trajectory Explains Why

Wall Street kept its Buy-heavy conviction on Zscaler stock after the Q3 print, with 39 of 47 analysts rating it Buy or Outperform and a mean target of $193 as of June 22, implying 56% upside from $124.

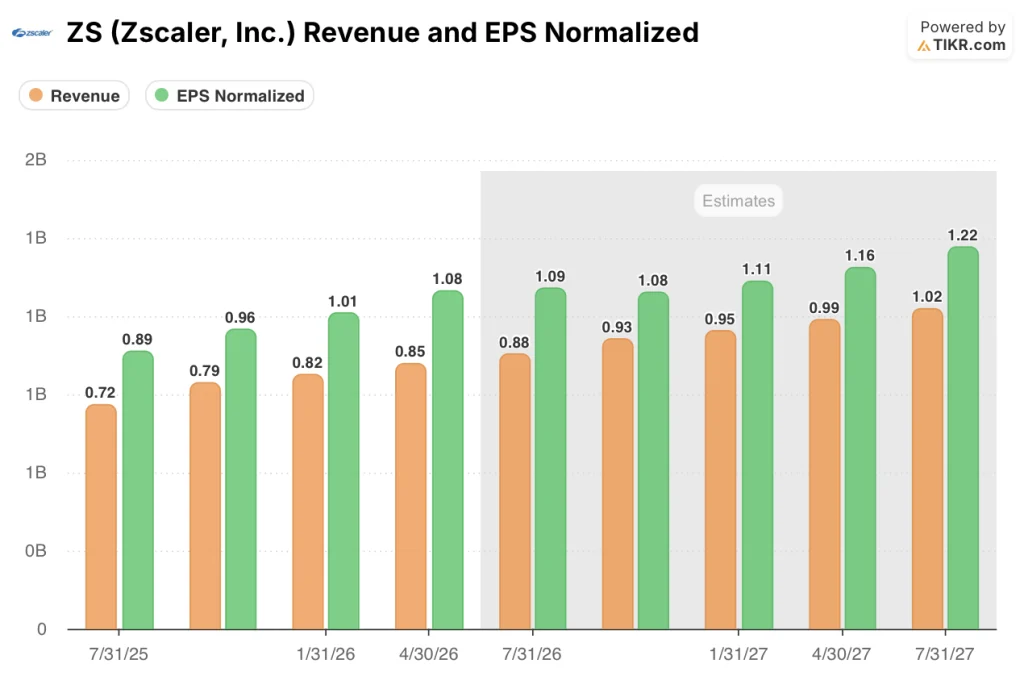

Zscaler stock’s Q4 revenue estimate consensus sits at $880 million, reflecting 22% year-over-year growth, and analysts project Q4 non-GAAP EPS of $1.09, up roughly 22% from the year-ago quarter’s $0.89.

The deceleration visible in the Q4 guide is genuine: Zscaler stock’s organic net new ARR growth, excluding the Red Canary acquisition that added roughly $127 million of ARR, runs at 14% year over year in Q3 and the company’s own preliminary FY27 framework targets 9.5% organic net new ARR growth in Q4.

Revenue growth of roughly 17.5% in the October 2026 quarter and 16.9% in the January 2027 quarter reflects sequential moderation from the 25% pace that defined fiscal 2026, which is the core tension the market is now pricing.

Against that deceleration, Zscaler stock’s EPS Normalized continues to compound: analysts estimate $1.09 in Q4 FY26, $1.08 in Q1 FY27, and $1.11 in Q2 FY27, a trajectory that puts full-year EPS growth in the low teens even on a deceleration path.

The 39 Buys against 8 Holds reflects a real analytical divide: bulls treat the selloff as an overshoot driven by manageable headwinds, primarily sales transitions and hardware capex timing, while the Hold camp awaits evidence that new logo growth actually inflects before lifting targets.

The next proof point is the Q4 FY26 report, due September 1, 2026: if net new ARR on an organic basis holds above $140 million and management reports the second sales leadership role filled, the Hold camp’s primary condition for conviction is satisfied.

Zscaler Stock Is Decelerating Faster Than CrowdStrike and Palo Alto on Revenue Growth

Zscaler stock posted revenue growth of 26% in the April 2026 quarter, matching CrowdStrike’s (CRWD) 26% and trailing Palo Alto Networks’ (PANW) 31%, marking the first quarter where PANW’s revenue growth rate overtook ZS.

Estimates show the gap widening through fiscal 2027: Zscaler stock’s revenue growth decelerates to 22% in the July 2026 quarter and then to the high teens across the October 2026 through July 2027 range, while CrowdStrike holds in the 22% to 23% band and Palo Alto sustains roughly 29% to 32% through the first half of fiscal 2027.

At 17% projected revenue growth by October 2026, Zscaler stock’s deceleration is the steepest in this peer set, and the market’s current discount to both PANW and CRWD on growth rate is the primary variable the September earnings report needs to narrow.

Is Zscaler Stock Undervalued in 2026? TIKR’s $220 Target Makes the Case

TIKR’s mid-case values Zscaler at $220 by July 2030, implying 78% total return from the current price of $124, or 15% annualized over the next 4.1 years.

The model’s 14% revenue CAGR assumption through 2035 is consistent with management’s 16% to 17% FY27 preliminary guidance and reflects a gradual deceleration from the 25% pace of fiscal 2026, not a structural collapse.

Zscaler stock’s margin structure supports the target: non-GAAP operating margin already hit 23% in Q3, and the EPS Normalized CAGR of 13.4% in the mid-case extrapolates existing operating leverage without requiring margin expansion beyond recent levels.

The hardware capex acceleration that cut the FY26 free cash flow margin guidance is a timing dynamic, not a structural drag, with management guiding only 200 basis points of CapEx-as-a-percentage-of-revenue increase in FY27 versus FY26 levels.

At $124, Zscaler stock is undervalued relative to the TIKR framework, with the $220 target requiring a revenue CAGR that management’s own preliminary guidance for FY27 effectively brackets at the low end.

Should You Invest in Zscaler, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Zscaler, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Zscaler, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ZS stock on TIKR for Free →