Key Stats for Disney Stock

- 52-Week Range: $92.19 – $124.69

- Current Price: $102.45

- Street Mean Target: ~$130

- TIKR Model Target: ~$132

- Q2 FY2026 Revenue: $25.2B (+7% YoY)

- Q2 FY2026 Adjusted EPS: $1.57 (+8% YoY)

- Q2 FY2026 SVOD Operating Margin: 10.6%

- LTM Net Debt/EBITDA: 1.98x

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A 25% Drawdown on a Business That Just Beat Earnings

The Walt Disney Company (DIS) hit a max drawdown of 25% on March 27, touching levels not seen since late 2023. The sell-off was broad, driven by tariff uncertainty and a macro environment that indiscriminately punished consumer discretionary names. The stock has partially recovered but remains about 16% below its one-year high.

The earnings themselves told a different story. Revenue increased 7% in fiscal Q2 to $25.2 billion, adjusted EPS rose to $1.57 from $1.45 in the prior-year period, and management raised full-year adjusted EPS growth guidance to approximately 12%, excluding the impact of a 53rd fiscal week.

Experiences set a fiscal second-quarter record. The gap between the operating results and where the stock is sitting is the central question for investors.

See historical and forward estimates for Disney stock (It’s free!) >>>

Streaming Finally Profitable, Parks Still Compounding

The entertainment business has been Disney’s most consequential transformation of the last five years. Disney+ and Hulu’s combined streaming operations generated operating income of $582 million in fiscal Q2 2026, up 88% from the prior-year period, with streaming operating margin crossing 10% for the first time. Management expects to sustain at least a 10% streaming margin for the full fiscal year.

The EPS chart shows what the full-company earnings arc looks like: normalized EPS grew from $2.33 in fiscal 2021 to $5.93 in fiscal 2025, a period that absorbed the losses from building streaming from scratch.

Consensus now sees that figure reaching around $6.83 in fiscal 2026 and continuing higher, with the streaming profitability inflection embedded in every forward estimate. Experiences contributed $2.6 billion in segment operating income in Q2 alone, with per capita domestic park spending up 5% year over year.

The risks deserve acknowledgment. Free cash flow fell sharply in the first half due to higher capital expenditures on cruise ship expansion and new park attractions, as well as accelerated tax payments from California wildfire deferrals. The sports segment’s operating income declined 5% in the quarter on higher rights costs, and domestic park attendance dipped 1% year over year on softness in international visitation.

Management addressed the broader trajectory in the Q2 shareholder letter: “At an important moment of change for Disney, we remain focused on executing our long-term growth strategy. Our creative and operational momentum drove strong quarterly results, and we continue to expect growth to accelerate in the second half of the fiscal year.”

See how Disney performs against its peers in TIKR (It’s free!) >>>

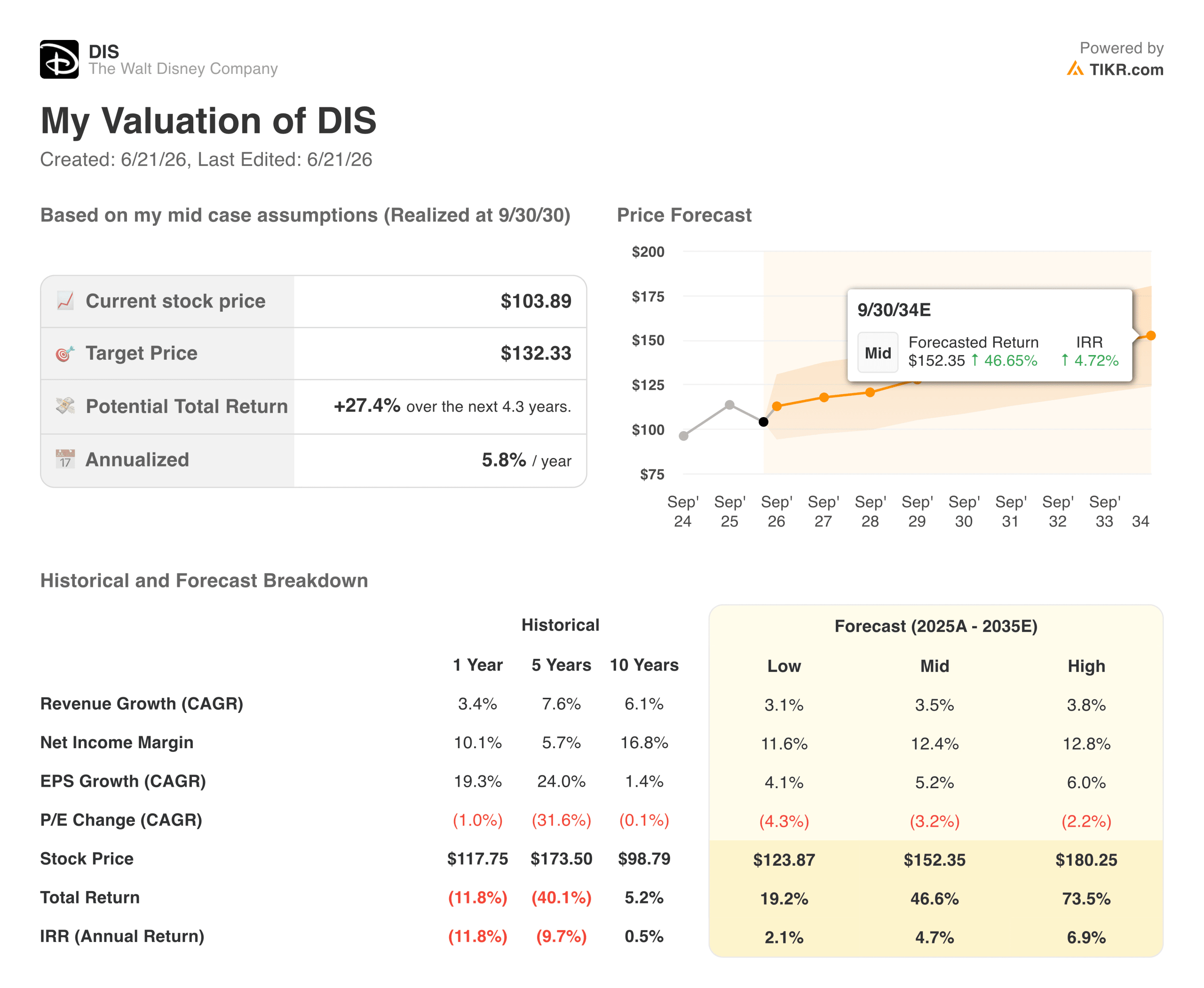

What Does the Valuation Model Say?

TIKR’s valuation model targets around $132 for The Walt Disney Company stock at approximately 6% annualized return through 2030, assuming mid-case revenue growth of around 3 to 4% and net income margins expanding toward 12%.

The Street mean target of around $130 sits in a similar range, which is relatively unusual and suggests both frameworks are anchored to the same moderate growth assumptions.

The return scenario is driven by EPS growth of around 5% per year, with the P/E multiple compressing modestly as Disney transitions from a growth rerating story to a mature compounder. The scenario range runs from around $124 in the low case to around $180 in the high case.

At roughly 14 times forward earnings, the valuation is not demanding. But the 6% annualized mid-case return reflects a business that is steady rather than explosive.

Should You Invest in The Walt Disney Company?

Disney has spent five years absorbing the cost of becoming a streaming company. The investment is now producing results: streaming is profitable, Experiences is growing, and EPS is compounding. A franchise pipeline that includes The Mandalorian & Grogu, Toy Story 5, and Avengers: Doomsday gives the IP flywheel more fuel than it has had in several years.

The question is not whether the business is working. It is whether a 6% annualized return over four years is enough to hold the stock through the volatility that Disney consistently delivers.

Put up The Walt Disney Company stock and access years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, and how the valuation compares to peers at TIKR for free.

See analysts’ growth forecasts and price targets for Disney stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!