Key Takeaways for NVIDIA Corporation Stock as of June 2026

- Analysts rate NVIDIA stock 48 buys, 10 outperforms, 2 holds, 1 no opinion, and 1 sell, with a mean target of $301, implying around 56% upside from the current price of $193.

- TIKR’s mid-case model values NVIDIA at around $504 by January 2031, implying around 162% total return, or roughly 23% annualized.

- NVIDIA returned a record $20 billion to shareholders in Q1 FY27, raised its quarterly dividend from $0.01 to $0.25 per share, and announced an $80 billion share repurchase authorization.

NVIDIA Just Posted $82 Billion in Q1 Revenue as Agentic AI Demand Goes Parabolic

NVIDIA Corporation (NVDA), the dominant platform for AI infrastructure, reported Q1 FY27 revenue of $82 billion, up 85% year-over-year and 20% sequentially, marking the third consecutive quarter of accelerating growth and the 14th straight quarter of sequential expansion.

Data Center revenue of $75 billion, up 92% year-over-year, drove the quarter, as the GB300 NVL72 configuration achieved what management called the fastest product ramp in company history, with every major hyperscaler, AI cloud operator, and frontier model builder deploying Blackwell architecture at scale.

Colette Kress, Executive Vice President and CFO, stated on the Q1 FY27 earnings call that “the $13.5 billion sequential revenue increase was also a record,” a figure that lands in context: NVIDIA added more quarterly revenue in a single sequential step than most S&P 500 companies generate in a full year.

Free cash flow reached $49 billion, up from $35 billion in Q4, while NVIDIA returned $20 billion to shareholders, raised its quarterly dividend 2,400% to $0.25 per share, and announced an $80 billion incremental buyback authorization.

Beyond Blackwell, Vera, a purpose-built agentic CPU, opens a $200 billion TAM the company has never addressed before, with management guiding to nearly $20 billion in stand-alone CPU revenue this fiscal year and production shipments of Vera Rubin beginning in Q3.

Q2 FY27 guidance of $91 billion, plus or minus 2%, confirms demand is not decelerating, with management reaffirming $1 trillion in combined Blackwell and Rubin revenue visibility from calendar 2025 through 2027.

58 Analysts Cover NVDA With Near-Uniform Conviction and a $301 Mean Target

As of June 26, 58 analysts cover NVIDIA stock: 48 rate it a Buy, 10 rate it an Outperform, 2 rate it a Hold, 1 has no opinion, and 1 rates it a Sell.

The mean price target is $301, implying around 56% upside from the current price of $193, with the Street high at $500 and the low at $180.

Wall Street Projects NVIDIA’s Revenue to Sustain Above 80% Growth Into Q3 FY27

The consensus projects NVIDIA revenue of approximately $92 billion in Q2 FY27, up roughly 96% year-over-year, following the $82 billion Q1 print.

Estimates then model $103 billion in Q3 FY27, up roughly 81% year-over-year, and $116 billion in Q4 FY27, up roughly 70%, as Vera Rubin volume begins to layer on top of the Blackwell base.

Normalized EPS of approximately $2.08 in Q2 is expected to grow to roughly $2.35 in Q3 and $2.66 in Q4, with the consensus projecting free cash flow of approximately $49 billion, $54 billion, and $61 billion across the same three quarters.

The single threshold the Street is watching is China: management excluded all Data Center compute revenue from China in Q2 guidance with no visibility on whether H200 export licenses translate to actual imports, and any resolution there represents unmodeled upside to every quarterly estimate through FY27.

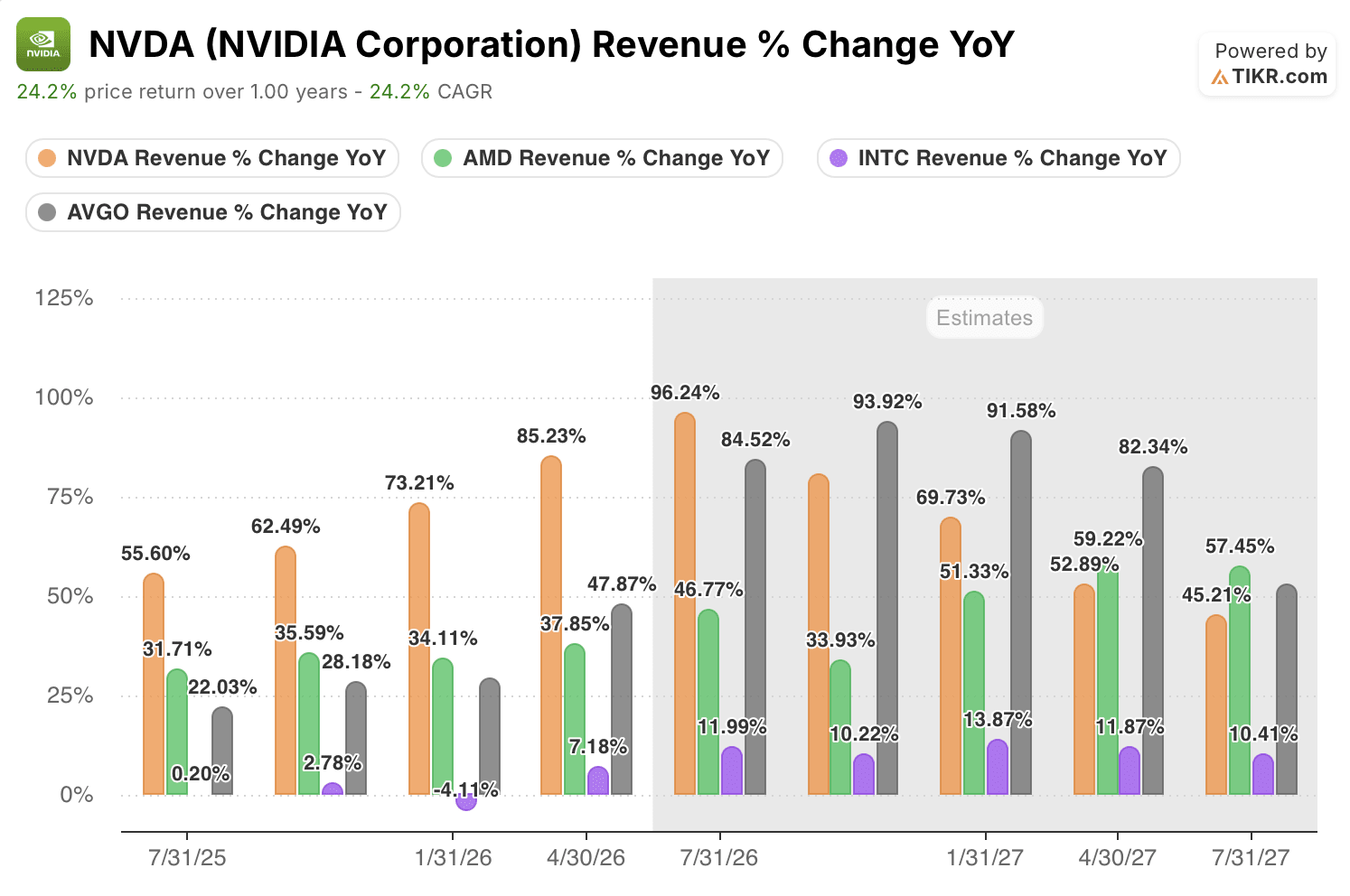

NVIDIA’s 96% Revenue Growth Leaves AMD, Intel, and Broadcom in a Different Race Entirely

NVIDIA’s estimated revenue growth of 96% year-over-year in Q2 FY27 runs at roughly double the pace of Broadcom (AVGO) at 84%, more than double Advanced Micro Devices (AMD) at 47%, and nearly ten times Intel (INTC) at 12%, a gap that reflects structural platform dominance rather than a cyclical timing advantage.

The divergence widens on a forward basis: consensus estimates have NVIDIA sustaining roughly 70% year-over-year growth through Q4 FY27, while Broadcom’s estimated growth decelerates toward 58% and AMD’s toward 34% over the same period, with Intel projected to remain in the low double digits throughout.

Is NVIDIA Stock Undervalued? TIKR’s $504 Target Implies 162% Upside by 2031

TIKR’s mid-case model values NVIDIA stock at around $504 by January 2031, implying around 162% total return from the current price of $193, or roughly 23% annualized over 4.6 years.

A 23% annualized return expectation from a company already generating $82 billion in quarterly revenue reflects both the scale of the opportunity ahead and the compounding effect of the $80 billion buyback authorization reducing share count over the model period.

The path to $504 runs through the same dynamics the Q1 print confirmed: Blackwell demand sustaining through the hyperscaler CapEx cycle, ACIE segment growth adding a structurally independent demand layer, Vera CPU revenue beginning to contribute from Q3, and free cash flow continuing to convert at roughly 53% to 60% of revenue as gross margins hold in the mid-70s.

Should You Invest in NVIDIA Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NVDA stock on TIKR for Free →