Key Stats for Lumentum Stock

- 52-Week Range: $808.8 to $45.65

- Current Price: $764.7

- Street High Target: $1,040

What Happened?

Lumentum Holdings (LITE) cleared $665.5 million in quarterly revenue for February 3, setting a company record for the second straight quarter, as Nvidia committed $2 billion to the photonics maker on March 2 under a multi-year strategic partnership that includes a separate multi-billion dollar purchase commitment for advanced laser components used in artificial intelligence data centers.

On March 2, Nvidia signed multi-year, non-exclusive agreements with Lumentum that pair the $2 billion equity investment with capacity access rights and a multi-billion dollar purchase commitment for indium phosphide lasers, the semiconductor-based components that carry data through light rather than electrical signals and sit at the center of next-generation AI chip interconnects, accelerating a Needham price target raise to $850 from $550 on March 4.

Lumentum’s optical circuit switch backlog, referring to hardware that routes data entirely through light to reduce latency and power versus traditional electrical packet switches, surged past $400 million by the Q2 2026 earnings call and then expanded further when the company closed a new multi-year, multibillion-dollar OCS agreement with an existing hyperscaler customer on March 17, a development that pushes OCS revenue toward a $1 billion annual run rate in calendar 2027.

S&P 500 inclusion, effective March 23, validated the company’s transformation from a telecom supplier into an AI infrastructure backbone, adding index-driven demand for a stock that had already gained more than 400% in 2025 before the Nvidia partnership reset its growth trajectory entirely.

Michael Hurlston, President and Chief Executive Officer, stated on the Q2 FY2026 earnings call that “our March revenue guidance with an $805 million midpoint represents an impressive 85-plus percent year-over-year increase,” anchoring management’s confidence in the business just weeks before the Nvidia investment and the Greensboro facility acquisition extended that trajectory into 2028.

Lumentum’s acquisition of a fifth indium phosphide fabrication facility in Greensboro, North Carolina on March 17, a 240,000-square-foot former Qorvo plant targeting production in mid-2028, combined with its confirmed $1.25 billion quarterly revenue milestone targeted within 9 to 12 months and a $2 billion quarterly target within 18 to 24 months, positions the company as the dominant supplier of the laser components that every major AI infrastructure buildout now depends on.

Wall Street’s Take on LITE Stock

The Nvidia partnership, $2 billion equity investment, and multi-billion dollar purchase commitment signed March 2 transform Lumentum from a components supplier into a strategic capacity partner for the AI chip supply chain, making the $805 million Q3 revenue midpoint a floor, not a ceiling.

TIKR estimates FY2026 revenue at $2.91 billion, a 76.8% YoY increase, and FY2027 revenue at $4.81 billion, a further 65.5% gain, supported directly by the $400 million OCS backlog confirmed for H2 calendar 2026 and the multi-hundred million dollar UHP laser order delivering in H1 calendar 2027.

LITE’s normalized EPS also is projected to surge from $2.06 in FY2025 to $7.69 in FY2026 and $14.98 in FY2027, a 273% and 95% successive annual leap driven by the operating leverage already visible in Q2’s 1,730 basis point year-over-year operating margin expansion.

Fourteen of 23 covering analysts rate LITE a buy and four rate it outperform, with five holds and a mean price target of $708.57, reflecting a consensus that has already been lapped by the stock’s $764.65 April 1 close as the market prices in developments Street models have not yet fully captured.

The spread between the $455 low target and the $1,040 high target reflects a genuine bifurcation: bears anchor to near-term supply chain execution risk on the OCS and CPO ramps, while bulls price in the $2 billion quarterly revenue milestone management has guided for within 18 to 24 months of March 17.

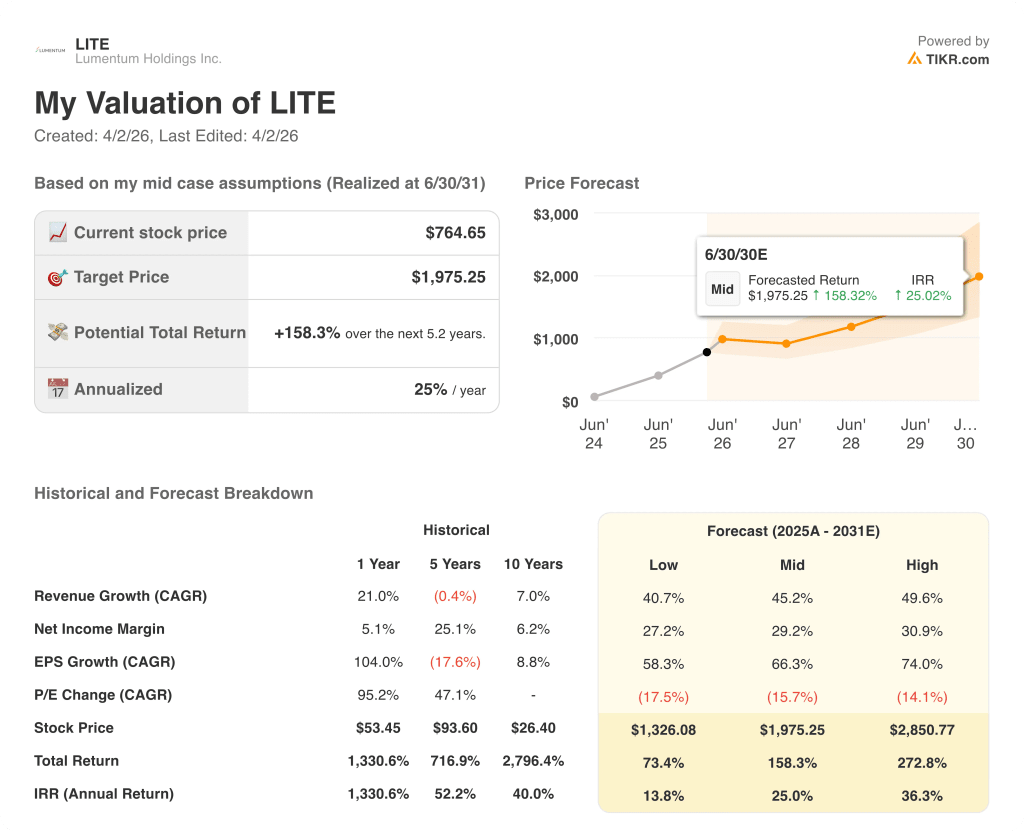

What Does the Valuation Model Say?

The TIKR mid-case model targets $1,975.25 per share by June 2031, implying a 158.3% total return and 25% annualized IRR, driven by a 45.2% revenue CAGR assumption that is directly supported by the Greensboro fab acquisition and Nvidia’s confirmed multi-billion dollar purchase commitment extending capacity needs into 2028.

At roughly 99x forward FY2026 normalized EPS of $7.69, LITE trades at a steep premium to its five-year historical average forward multiple, yet the 273% EPS growth projected for this fiscal year and 95% for the next make the stock fairly valued rather than overvalued, as few compounders in the semiconductor supply chain have ever entered a demand cycle where their core product is simultaneously supply-constrained, sole-sourced, and backed by a $2 billion anchor investor.

The TIKR model’s 45.2% revenue CAGR assumption is anchored to the $400 million OCS H2 calendar 2026 backlog, the UHP laser CPO ramp confirmed for H1 2027, and the 50% incremental indium phosphide capacity increase targeted from Q4 calendar 2025 to Q4 calendar 2026, with the model price of $1,975.25 only rising if Greensboro revenue is added post-2028.

Management’s signal is unambiguous: Lumentum is undershipping customer demand by 25% to 30% even after adding 20% fab capacity in a single quarter, a supply deficit that is growing, not narrowing, as the AI infrastructure buildout accelerates.

The single risk that breaks the model is fab ramp execution: if Caswell’s conversion from EML to UHP production slips, or Greensboro qualification extends past mid-2028, CPO revenue misses and the $2 billion quarterly target slides with it.

Q4 FY2026 earnings, expected around August 2026, will be the first test of whether OCS revenue is tracking toward the $400 million H2 backlog commitment and whether UHP laser shipments are building the run rate needed for the H1 2027 CPO order delivery.

Should You Invest in Lumentum Holdings Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LITE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lumentum Holdings Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LITE stock on TIKR for Free →