Key Stats for Johnson & Johnson Stock

- Past-Week Performance: -3.2%

- 52-Week Range: $141.5 to $251.7

- Current Price: $242

What Happened?

Johnson & Johnson (JNJ), the $242 healthcare giant spanning cancer drugs and surgical robotics, crossed $94.2 billion in 2025 sales while burying its biggest revenue headwind in the rearview mirror.

The FDA approved TECVAYLI plus DARZALEX FASPRO on March 5 under the agency’s new priority voucher program, clearing the combination in just 55 days versus the typical 10 to 12 months, based on Phase 3 data showing an 83% reduction in myeloma progression risk.

The approval cycle runs on DARZALEX, J&J’s foundational multiple myeloma antibody, which grew 22% to more than $14 billion in annual sales while TREMFYA, the company’s immunology blockbuster for bowel disease and psoriasis, exceeded $5 billion for the first time with Q4 growth of 65%.

Chairman and CEO Joaquin Duato stated on the Q4 2025 earnings call that “we have line of sight to double-digit growth by the end of the decade, which is notable as Johnson & Johnson is the only health care company that will soon deliver more than $100 billion in annual revenue.”

With Oncology targeting $50 billion by 2030, TREMFYA projecting $10 billion in peak sales, and the FDA approval of TECNIS PureSee on March 12 expanding J&J’s surgical vision franchise, the company’s transition from STELARA dependency to a multi-platform growth engine is now showing up in the numbers.

Wall Street’s Take on JNJ Stock

The March 5 FDA approval of TECVAYLI plus DARZALEX FASPRO under the priority voucher program accelerates J&J’s shift from a single-blockbuster dependency to a diversified oncology platform generating compounding margin leverage.

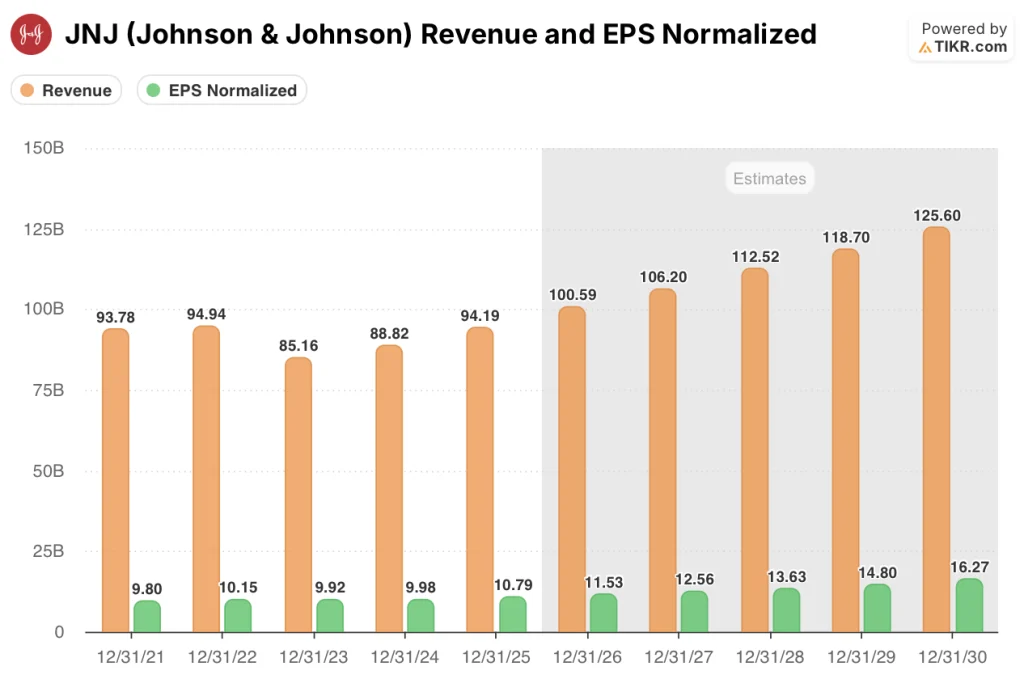

Consensus estimates reflect that shift directly: as DARZALEX, TREMFYA, and the newly approved TECVAYLI combination scale across more treatment lines, revenue is projected to reach $100.6 billion in 2026 and $125.6 billion by 2030, while normalized EPS, the per-share earnings figure that strips out one-time items, climbs from $10.79 in 2025 to $16.27 by 2030, a 51% cumulative increase driven by both top-line growth and expanding net income margins.

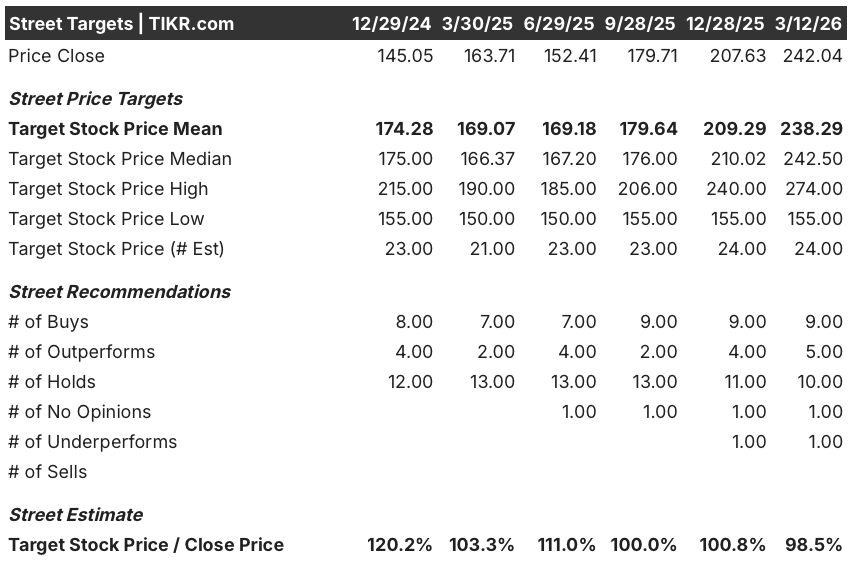

With 9 buys, 5 outperforms, 10 holds, 1 underperform, and 1 sell among 26 analysts, the Street’s mean price target of $238.29 sits just 1.6% below the current price of $242.04, suggesting analysts have not yet fully repriced the post-STELARA growth acceleration.

The analyst target range stretches from $155 to $274, with the low anchored to talc litigation uncertainty and ongoing Orthopaedics transformation costs, and the high requiring TREMFYA and DARZALEX to sustain double-digit growth through the early part of the decade.

What Does the Valuation Model Say?

The TIKR mid-case model prices J&J at $301.17 by December 2030, implying 24.4% total return and a 4.7% annualized IRR, driven by a mid-case revenue CAGR of 5.9% and net income margin expanding from 27.8% in 2025 to 30.9% by 2031. The model prices in a P/E multiple compression of 3.5% annually, meaning the return is earned entirely through earnings growth, not re-rating.

The market is pricing J&J near a breakeven analyst mean target while the company just guided to $100 billion in 2026 revenue and double-digit growth by decade end.

DARZALEX growing 22% to more than $14 billion annually and TREMFYA exceeding $5 billion for the first time provide the specific operational proof that the margin expansion the TIKR model assumes is already in motion.

CEO Joaquin Duato’s line of sight to double-digit growth is not speculative: 28 platforms generating at least $1 billion in annual revenue and $21 billion in projected 2026 free cash flow make the compounding case structural, not promotional.

The primary risk is talc litigation: an adverse Daubert ruling on appeal could force a reserve step-up that directly pressures the free cash flow the TIKR model needs to sustain margin expansion and share count reduction.

The April 14 Q1 2026 earnings call is the first test, with TREMFYA IBD ramp, TECVAYLI plus DARZALEX commercial launch trajectory, and the $500 million MedTech tariff impact all hitting the P&L simultaneously.

Should You Invest in Johnson & Johnson?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JNJ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Johnson & Johnson alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze JNJ stock on TIKR for Free →