Intuitive Surgical (NASDAQ: ISRG) remains the undisputed leader in robotic-assisted surgery, supported by strong procedure growth and a dominant installed base of its da Vinci systems. The stock trades near $547/share, recovering sharply in recent months as confidence in its long-term growth story continues to build.

Recently, Intuitive reported solid quarterly results, highlighted by rising procedure volumes and growing adoption of its da Vinci Xi and Ion platforms. The company also introduced new AI-driven software tools to assist surgeons in training and precision control, signaling a deeper move toward intelligent surgery. These updates strengthen its leadership in surgical robotics and expand its global reach.

This article explores where Wall Street analysts believe Intuitive Surgical could trade by 2027, combining consensus price targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

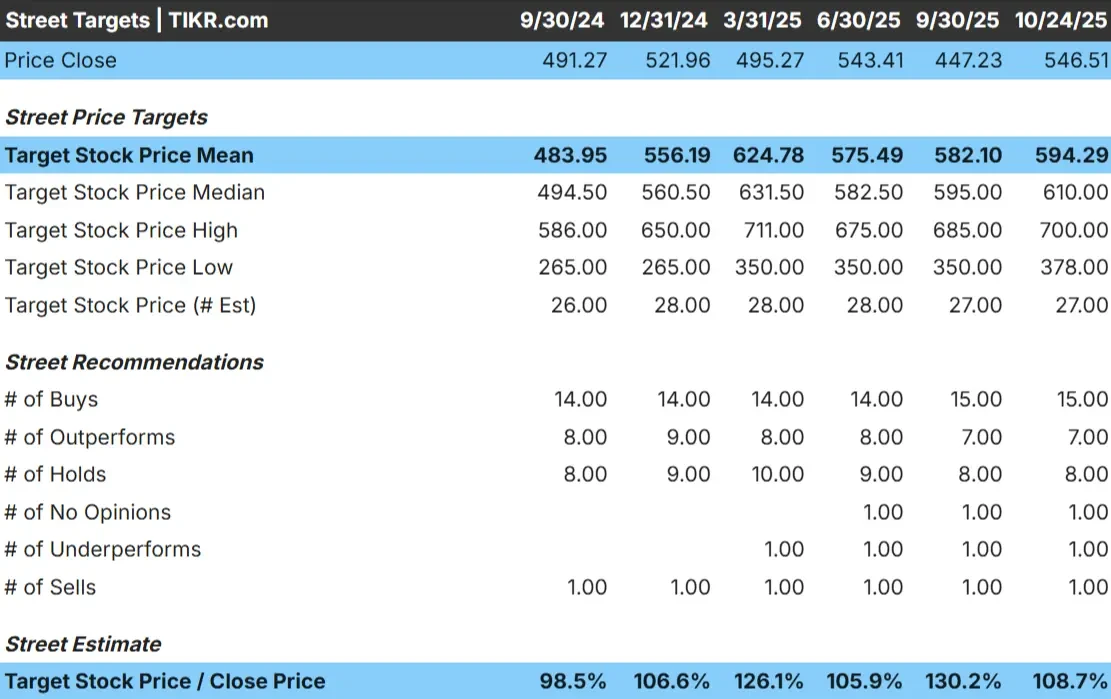

Intuitive Surgical trades around $547/share today. The average analyst price target sits near $594/share, implying about 9% upside from current levels. Forecasts show a wide range, reflecting mixed conviction among analysts:

- High estimate: ~$700/share

- Low estimate: ~$378/share

- Median target: ~$610/share

- Ratings: 15 Buys, 7 Outperforms, 8 Holds, 1 Underperform, 1 Sell

The modest upside shows that most analysts expect steady but not explosive returns. For investors, this means Intuitive could outperform if procedure volumes continue to accelerate or if new system placements exceed expectations. While valuation limits short-term gains, its dominant market share and recurring instrument revenue make it a reliable long-term compounder.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Intuitive Surgical: Growth Outlook and Valuation

The company’s fundamentals remain strong:

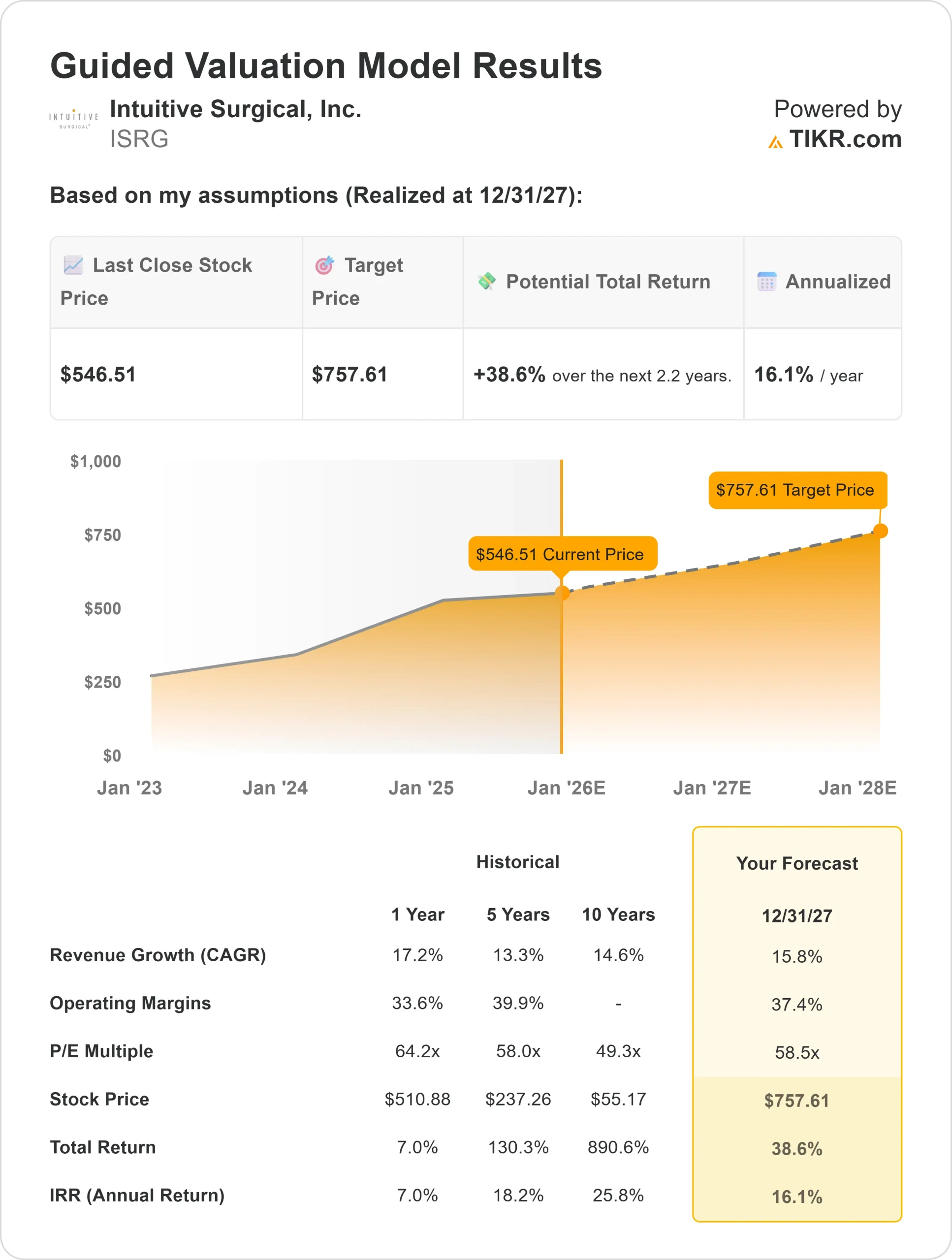

- Revenue is projected to grow about 16% annually through 2027

- Operating margins are expected near 37%

- Shares trade around 59x forward earnings, above medtech averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 59x forward P/E suggests about $758/share by 2027

- That implies roughly 39% total upside, or about 16% annualized returns

These projections reflect analysts’ confidence in Intuitive’s ability to expand its installed base and grow recurring instrument revenue. For investors, the key takeaway is that the stock’s long-term appeal lies in its recurring cash flow and innovation pipeline. While the valuation is demanding, its leadership in robotic surgery and expanding global adoption make it one of the most durable compounders in healthcare.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Intuitive Surgical’s dominance in robotic-assisted surgery continues to strengthen. Its large installed base of da Vinci systems generates recurring revenue from instruments and services, while global procedure volumes keep growing at a healthy pace.

The company’s focus on innovation is also fueling optimism. Its next-generation platforms and AI-driven tools aim to make surgeries faster, safer, and more precise. For investors, these advances show how Intuitive is turning its technological edge into predictable growth, supported by strong margins and consistent cash generation.

Bear Case: Valuation and Execution Risks

Even with these positives, valuation remains a concern. At around 59x forward earnings, Intuitive trades at one of the highest multiples in medtech. That leaves little room for error if hospital budgets tighten or if new competitors gain traction.

The market is also watching how well the company scales newer systems like Ion, which target lung and soft-tissue procedures. Any slowdown in adoption could pressure growth. For investors, the key risk is that the stock’s premium valuation already prices in a lot of success. If procedure volumes or capital equipment demand soften, returns could flatten despite strong fundamentals.

Outlook for 2027: What Could Intuitive Surgical Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 59x forward P/E suggests Intuitive Surgical could trade near $758/share by 2027. That represents about 39% total upside, or roughly 16% annualized returns.

While this outlook shows meaningful long-term potential, it also assumes consistent execution and sustained demand growth. To deliver stronger gains, Intuitive will need to expand its platform adoption in emerging markets and continue leading innovation in surgical robotics.

For investors, Intuitive stands out as a high-quality compounder rather than a quick win. Its proven business model, recurring revenue base, and global scale make it one of the most resilient names in medtech, though short-term returns may be limited by valuation.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.