Key Takeaways:

- Rolls-Royce is executing a comprehensive turnaround strategy through operational excellence, Civil Aerospace recovery, and Defense portfolio expansion.

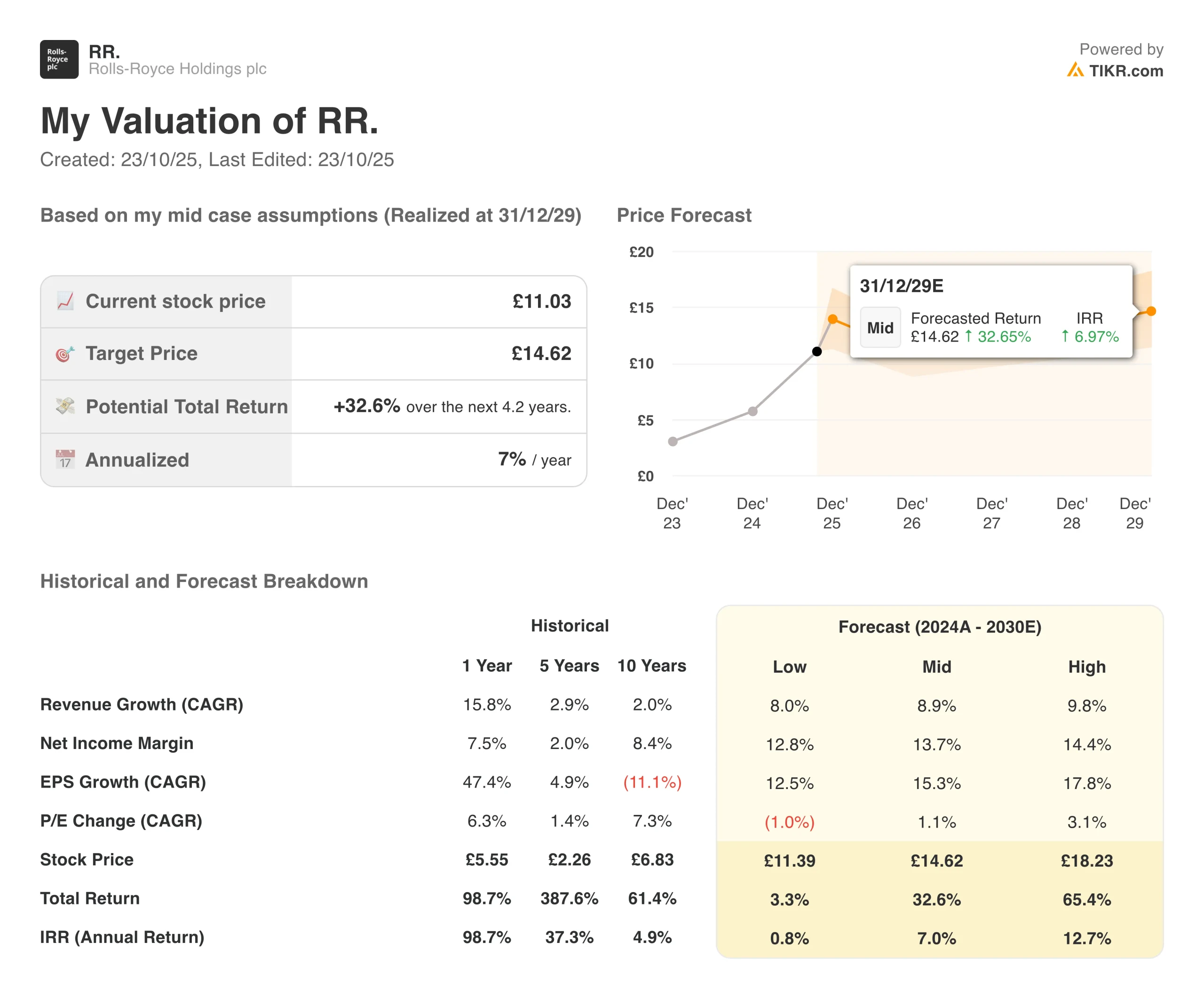

- RR stock could reasonably reach £12.85/share by December 2027, based on our valuation assumptions.

- This implies a total return of 17% from today’s price of £11.03, with an annualized return of 7.2% over the next 2.2 years.

Rolls-Royce Holdings (RR) is redefining aerospace and defense engineering through strategic transformation, addressing comprehensive power systems solutions, engine lifecycle services, and electrical propulsion innovations across its global markets.

The British engineering icon serves customers worldwide through its diversified platform, spanning jet engines for wide-body aircraft, military propulsion systems, submarine nuclear reactors, and power generation equipment delivered through Civil Aerospace, Defense, and Power Systems divisions.

Core offerings include Trent engine families powering long-haul commercial aircraft, military engines for fighter jets and transport planes, nuclear propulsion for Royal Navy submarines, and electrical power solutions for marine and industrial applications.

The aerospace leader has delivered exceptional recent performance, with 15.8% revenue growth over the past year and operating margins expanding to 13.8% as the company executes its transformation program under CEO Tufan Erginbilgic.

Rolls-Royce demonstrates strong execution across operational improvement and commercial recovery following years of pandemic-related challenges and operational missteps.

The company achieved record flying hours in Civil Aerospace, expanded Defense order intake, substantially improved cash generation, and reduced net debt while investing in next-generation propulsion technologies, including sustainable aviation fuels and electrical systems.

RR stock trades on the London Stock Exchange and has risen 1,400% in the last three years. Here’s why Rolls-Royce stock could deliver solid returns through 2027 as it capitalizes on the wide-body aviation recovery, transforms operational performance, and expands its Defense franchise.

See analysts’ full growth forecasts and estimates for RR stock (It’s free) >>>

What the Model Says for Rolls-Royce Stock

We analyzed the upside potential for Rolls-Royce stock using valuation assumptions based on its turnaround execution capabilities and market recovery opportunities across Civil Aerospace and Defense markets.

Analysts see an opportunity ahead for Rolls-Royce stock, given its proven operational transformation, exposure to the wide-body aviation recovery, and a systematic approach to building competitive advantages while restoring margins to peer levels.

Rolls-Royce’s multi-divisional strategy provides diversified growth vectors. At the same time, the Civil Aerospace recovery validates that disciplined execution can drive margin expansion and cash generation in the recovering long-haul aviation market.

Based on estimates of 9% annual revenue growth, 17% operating margins, and a normalized P/E valuation multiple of 32x, the model projects Rolls-Royce stock could rise from £11.03/share to £12.85/share.

That would be a 17% total return, or a 7.2% annualized return over the next 2.2 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Rolls-Royce stock:

1. Revenue Growth: 7%

Rolls-Royce delivered impressive recent performance, with 15.8% revenue growth over the past year, driven by a recovery in Civil Aerospace flying hours and Defense order execution.

Growth drivers include continued increases in wide-body aircraft utilization as long-haul international travel normalizes, aftermarket service revenue growth from the installed engine base, Defense spending increases across NATO allies, and new engine program ramps, including UltraFan technology development.

We used a 9.3% forecast, reflecting Rolls-Royce’s transition from recovery-driven hypergrowth to more normalized expansion as flying hours approach pre-pandemic levels. At the same time, long-term aviation growth and Defense opportunities provide sustained momentum.

2. Operating Margins: 17%

Rolls-Royce has expanded operating margins dramatically to 13.8% over the past year, supported by operational transformation initiatives, improved Civil Aerospace pricing, and Defense mix benefits.

RR targets continued margin improvement through

- Operational excellence programs

- Eliminating costs and complexity

- Civil Aerospace margin expansion toward mid-teens targets as pricing and volume scale

- Defense maintaining high-teens margins

- Overhead reduction as restructuring completes

3. Exit P/E Multiple: 32x

Rolls-Royce stock trades at an elevated multiple of around 36x currently, reflecting its turnaround story, Civil Aerospace recovery exposure, and operational transformation potential.

We maintain a 32x valuation level given Rolls-Royce’s execution capabilities under new leadership, improving cash generation, and a systematic approach to building sustainable competitive advantages through engineering excellence and installed base economics.

Long-term competitive advantages from intellectual property, barriers to entry in large-engine design, and aftermarket economics from the installed base should support premium valuations as the company delivers on margin targets and capitalizes on Defense modernization while advancing sustainable aviation technologies.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for RR stock through 2030 show varied outcomes based on execution and market conditions (these are estimates, not guaranteed returns):

- Low Case: Slower aviation recovery and margin pressure → 1% annual returns

- Mid Case: Successful transformation and Defense growth → 7% annual returns

- High Case: Margin targets achieved with strong aftermarket → 13% annual returns

Even in the conservative case, Rolls-Royce stock offers modest returns supported by wide-body exposure and proven ability to improve operations while the turnaround progresses.

The upside scenario for RR stock could deliver strong performance if the company successfully achieves mid-teens Civil Aerospace margins while maintaining Defense performance and accelerating cash generation.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!