United Parcel Service, Inc. (NYSE: UPS) has faced a rough stretch. The stock trades near $87/share, down about 35% over the past year as shipping volumes weakened and labor costs climbed. Still, analysts see signs of value emerging as UPS leans on efficiency, pricing discipline, and its high-margin business mix.

Recently, UPS introduced several technology and service upgrades to strengthen profitability and efficiency. The company expanded its use of AI through new pricing and logistics automation tools, enhanced visibility in its premium ground services, and continued cost-cutting efforts to support margin recovery. These initiatives highlight UPS’s commitment to improving network productivity and maintaining strong customer service even in a soft freight environment.

This article explores where Wall Street analysts think UPS could trade by 2027. We’ve combined consensus forecasts and valuation models to outline the stock’s potential recovery path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

UPS trades around $87/share today. The average analyst price target is $99/share, which points to roughly 14% upside over the next year. Forecasts show a relatively tight range, suggesting moderate confidence in the outlook:

- High estimate: ~$120/share

- Low estimate: ~$75/share

- Median target: ~$100/share

- Ratings: 13 Buys, 1 Outperform, 14 Holds, 2 Underperform, 1 Sell

Analysts expect some recovery potential, but sentiment remains cautious following a year of weak shipping volumes and higher labor costs. For investors, this indicates modest upside in the near term, with the possibility of stronger gains if freight demand and pricing trends improve faster than expected.

See analysts’ growth forecasts and price targets for United Parcel Service (It’s free!) >>>

UPS: Growth Outlook and Valuation

The company’s fundamentals point to a steady, gradual recovery supported by efficiency improvements and capital discipline.

- Revenue is expected to stay roughly flat through 2027

- Operating margins are projected around 10%

- Shares trade at about 13× forward earnings, slightly below historical averages

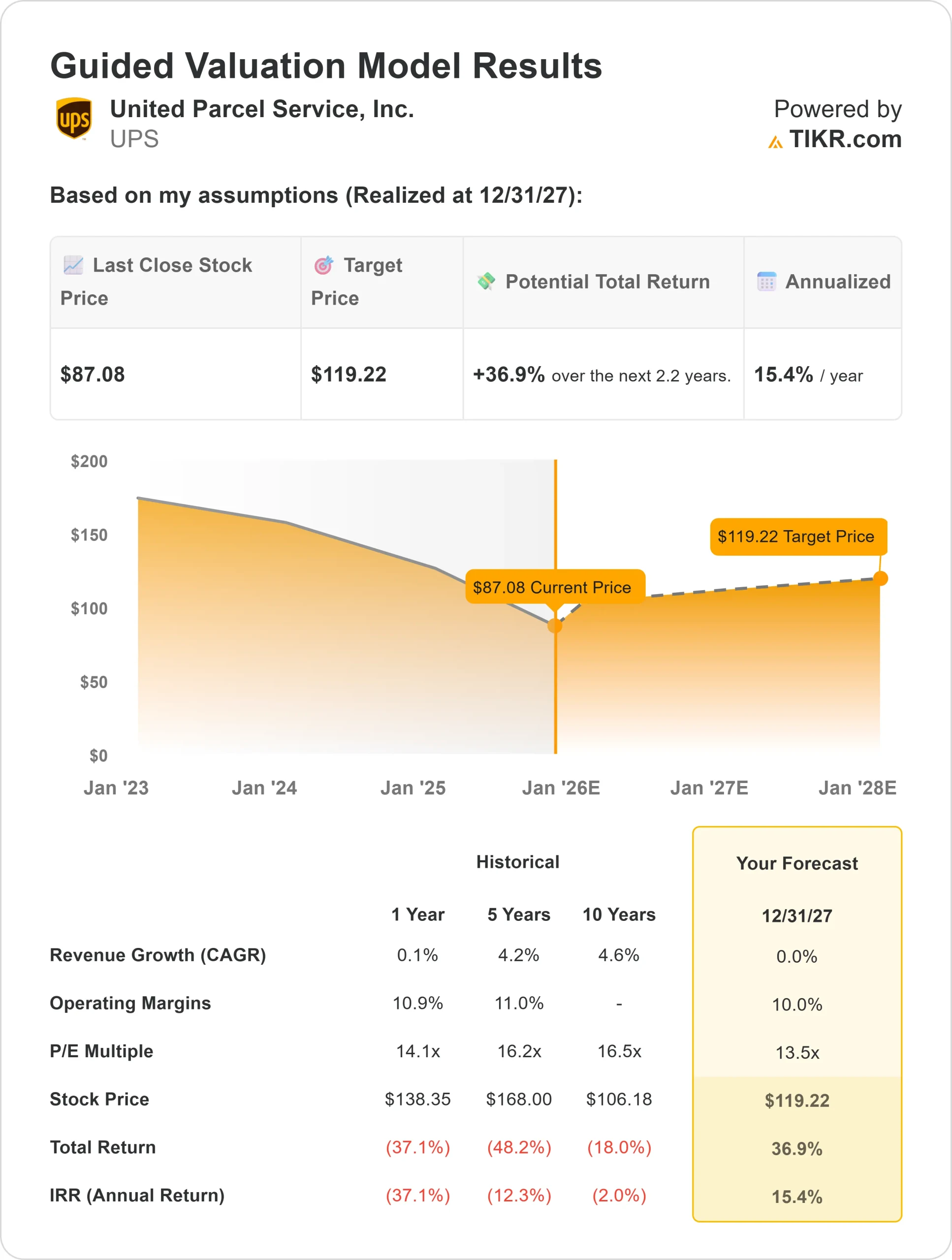

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 13× forward P/E suggests $119/share by 2027

- That implies about 37% total upside, or roughly 15% annualized returns

For investors, this points to a potential mid-teens annual return profile if UPS keeps costs under control and freight volumes gradually improve. The valuation looks reasonable for a global logistics leader that continues to generate strong cash flow even through soft shipping cycles.

Value stocks like United Parcel Service in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

UPS continues to focus on profitable growth and operational efficiency. Its automation programs and route optimization technology are helping reduce costs while maintaining service reliability. The company’s push toward higher-margin customers and premium logistics offerings supports profitability even in a sluggish freight market.

International expansion and growth in business-to-business logistics also provide a long-term tailwind. For investors, these initiatives show that UPS can stabilize earnings, protect its dividend, and gradually rebuild shareholder value as market conditions improve.

Bear Case: Demand and Cost Pressures

Despite these strengths, UPS still faces near-term challenges. Freight volumes remain weak, and consumer demand has yet to fully rebound. Labor costs are elevated following the Teamsters contract, putting pressure on margins while limiting short-term pricing flexibility.

For investors, the risk is that the recovery could take longer than expected. If demand stays soft or inflation keeps costs high, UPS may see slower earnings growth, keeping share price gains moderate over the next few years.

Outlook for 2027: What Could UPS Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 13× forward P/E suggests UPS could trade near $119/share by 2027. That represents about 37% total upside, or roughly 15% annualized returns.

While this would mark a solid recovery, it already assumes gradual improvement in freight activity and stable margins. For investors, stronger-than-expected gains would likely depend on faster cost efficiency, improved delivery demand, and sustained free cash flow growth.

UPS looks like a dependable income and value play, offering steady dividends and potential for mid-teens annualized returns as operations normalize and technology investments start to deliver results.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.