Regeneron Pharmaceuticals (NASDAQ: REGN) has struggled over the past year, with shares down nearly 38% from their 2024 peak. The slowdown reflects weaker revenue growth and softer demand for its flagship eye drug Eylea. Still, analysts expect moderate upside as new therapies gain traction and profitability stays strong.

Recently, Regeneron announced new data supporting Dupixent’s potential use in chronic obstructive pulmonary disease (COPD), following positive Phase 3 results presented in 2024 and regulatory submissions now under review in 2025. The company also reported continued progress across its oncology and immunology pipeline, including expanded trials for linvoseltamab in multiple myeloma and new studies evaluating Odronextamab in lymphoma. Alongside these R&D milestones, Regeneron continues to generate strong cash flow and maintain a debt-free balance sheet, underscoring its ability to invest for long-term growth even in a slower market environment.

This article explores where Wall Street analysts think Regeneron could trade by 2027. We’ve gathered consensus price targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Regeneron trades near $578/share, while the average analyst price target sits around $725/share, implying about 26% upside over the next year. Forecasts show a fairly tight range, suggesting analysts are cautiously optimistic:

- High estimate: ~$900/share

- Low estimate: ~$543/share

- Median target: ~$750/share

- Ratings: 15 Buys, 4 Outperforms, 6 Holds, 1 Underperform

It looks like analysts still see room for gains, but expectations are balanced. For investors, the takeaway is that Regeneron is viewed as a steady compounder rather than a breakout story. Its strong pipeline and cash position provide support for moderate upside if execution stays on track.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Regeneron: Growth Outlook and Valuation

Regeneron’s fundamentals remain solid, though growth has cooled compared to its peak years:

- Revenue is expected to grow around 4% annually through 2027

- Operating margins should hold near 34%

- Shares trade around 15x forward earnings, slightly below their 5-year average

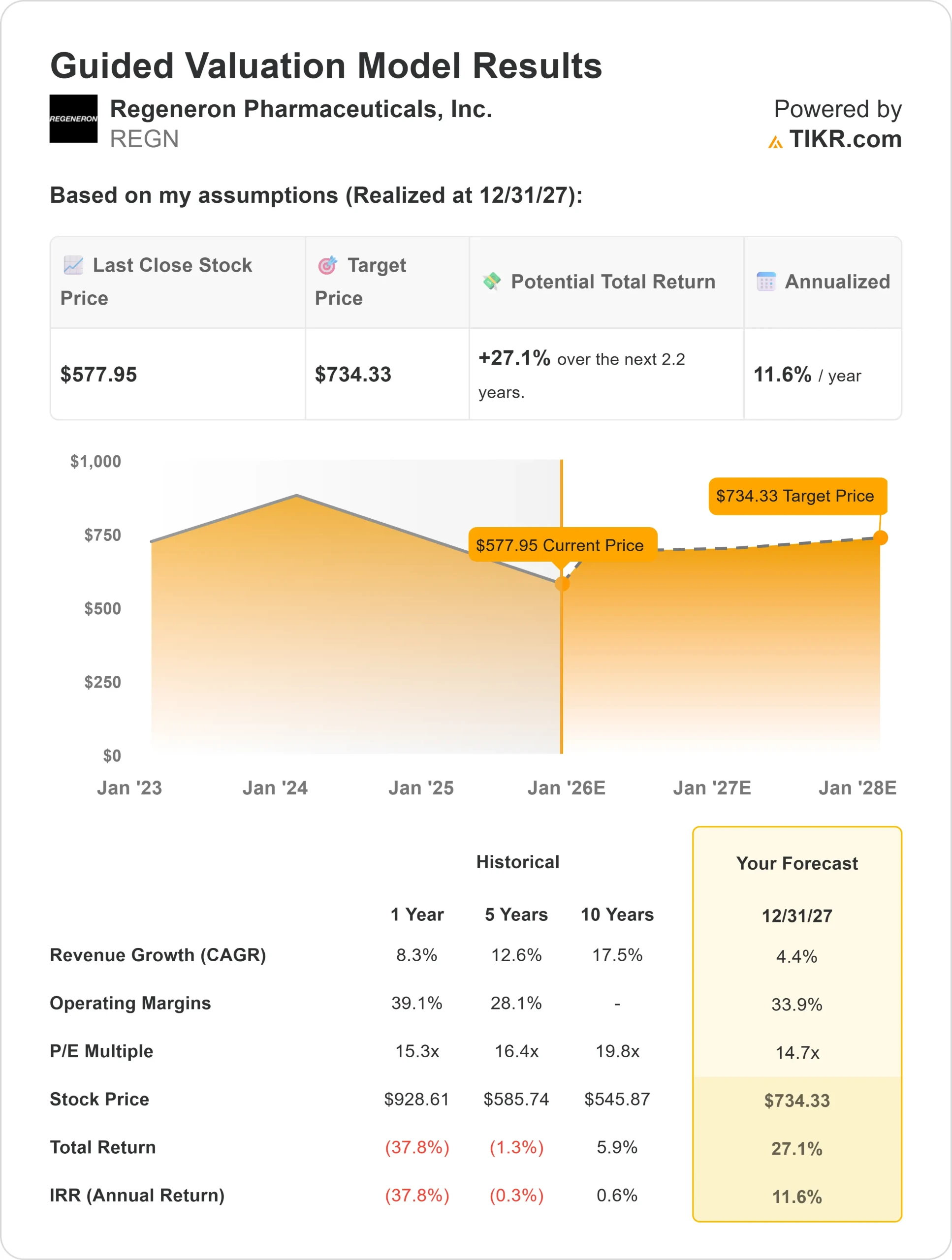

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 14.7x forward P/E suggests roughly $734/share by 2027

- That implies around 27% total upside, or about 12% annualized returns

These figures suggest Regeneron can continue compounding steadily, supported by consistent earnings and disciplined capital allocation. For investors, the stock looks fairly priced for its growth profile and could deliver solid returns if margins remain strong and new therapies gain momentum.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Regeneron’s innovation pipeline remains one of the most promising in biotech. Its antibody platform continues to produce new therapies across oncology, immunology, and rare diseases. Dupixent remains the company’s growth engine, with expanding indications including COPD potentially driving the next phase of revenue growth.

The company’s focus on R&D efficiency and strong cash generation also supports continued reinvestment in innovation. For investors, these strengths suggest Regeneron can sustain profitability while gradually rebuilding top-line momentum. Its track record of scientific leadership gives confidence that it can weather short-term headwinds.

Bear Case: Slower Growth and Pipeline Risk

Despite these positives, Regeneron’s near-term growth remains limited. Eylea still represents a large portion of sales and faces increasing competition from biosimilars and new entrants in the retinal market. If new drugs take longer to scale, earnings could stagnate.

Valuation also assumes stable margins and steady product launches. Any delays in the pipeline or pricing pressure could dampen returns. For investors, the risk is that Regeneron’s growth stays slow enough for the stock to trade sideways, even with strong fundamentals.

Outlook for 2027: What Could Regeneron Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 14.7x forward P/E suggests Regeneron could trade near $734/share by 2027. That would represent about 27% total upside, or roughly 12% annualized returns from current levels.

While this points to moderate upside, it already factors in stable margins and ongoing pipeline success. To deliver stronger returns, Regeneron would need to exceed expectations in key programs like Dupixent and its emerging oncology portfolio.

For investors, Regeneron offers a balance of innovation, profitability, and financial strength. It may not be a high-growth name anymore, but it remains a high-quality biotech compounder capable of delivering steady long-term gains.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.