Shopify Inc. (SHOP) has reasserted its dominance as Canada’s flagship technology company, powering more than five million merchants globally through its end-to-end e-commerce and payments ecosystem. From online storefronts to point-of-sale systems, shipping, financing, and analytics, Shopify has built a full-stack commerce platform that anchors much of the modern digital retail economy.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free!)

In 2025, that model is paying off, as second-quarter revenue climbed 31% year-over-year to US $2.68 billion, driven by record merchant adoption and growing penetration of Shopify Payments, Markets, and Fulfillment Network. Gross merchandise volume reached US $87.8 billion, up 31%, while free cash flow margins held above 16% for an eighth consecutive quarter, proving that scale and profitability can coexist.

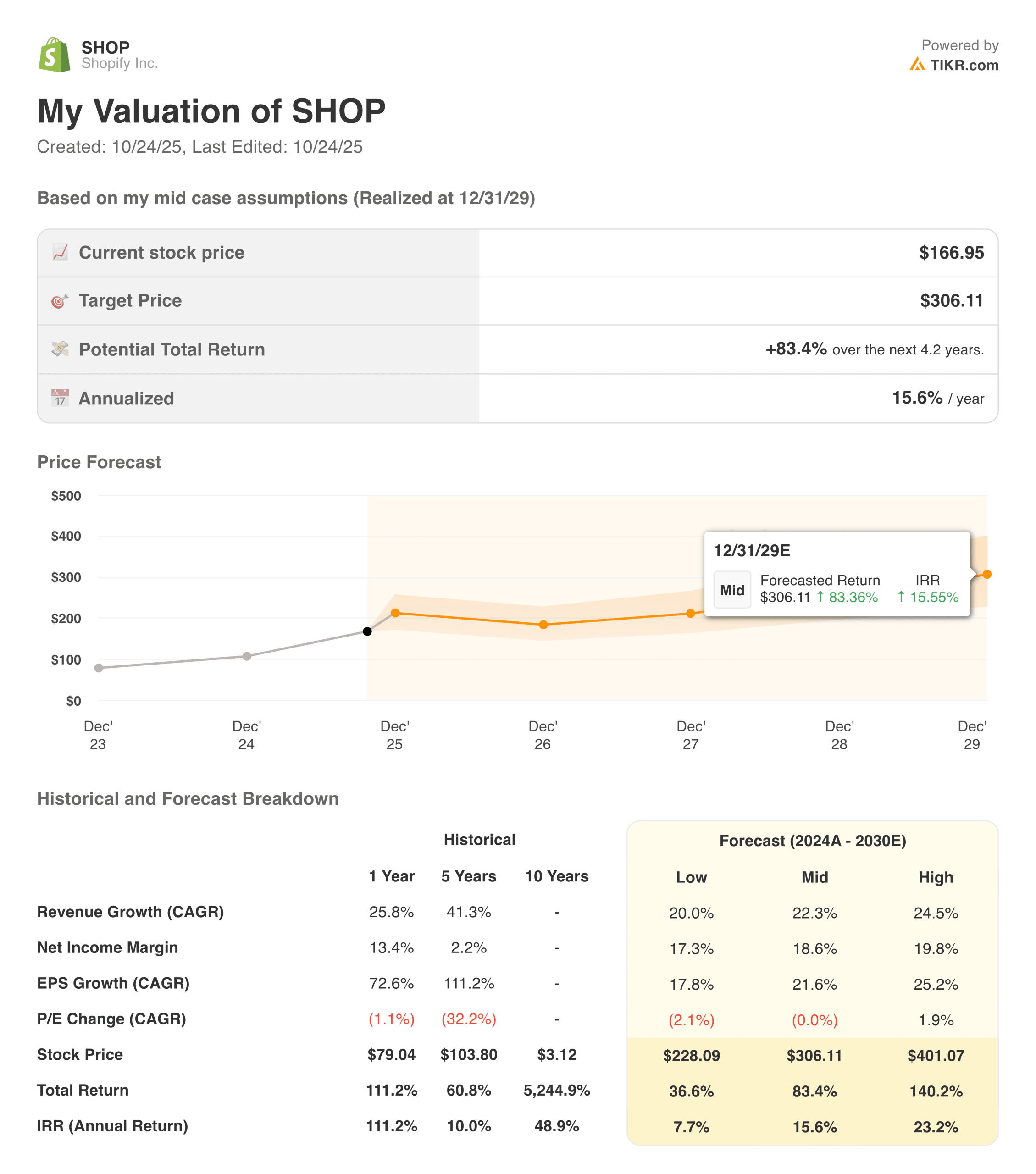

At roughly C$220 per share, Shopify is one of the best-performing TSX listings this year, up nearly 107% over twelve months. The question now is whether its high-growth narrative and recurring-revenue model justify a forward P/S ratio of nearly 18x, or whether investors are chasing momentum in an already fully-priced story.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Shopify’s Q2 results reinforced a critical turning point: sustainable profitability. After years of prioritizing growth, the company now delivers consistent free cash flow while maintaining 30%+ topline expansion. Merchant Solutions revenue, which includes payments, shipping, and capital lending, remains the key engine, growing 37% YoY and now accounting for three-quarters of total revenue.

| Metric | Value | YoY Change | Notes |

|---|---|---|---|

| Revenue | US$656M | +31% | Strongest Q2 since 2021 |

| GMV | US $87.8 B | +31% | Growth led by international markets |

| Free Cash Flow Margin | 16% | — | 8th straight double-digit quarter |

| Subscription Revenue | US$6.4B | +17% | Steady base growth |

| Merchant Solutions Revenue | US $2.02B | +37% | Driven by payments & fulfillment |

| Gross Margin | 48.6% | −250 bps | Higher transaction costs |

| Cash & Equivalents | US $6.4B | +14% | Strong liquidity position |

Operating expenses rose modestly as Shopify continued investing in AI tools, enterprise-grade features, and logistics automation. Management reiterated confidence in maintaining double-digit operating margins for 2025, supported by disciplined cost control and rising subscription ARPU. The company’s balance sheet remains pristine, with over US $6 billion in cash and no long-term debt, giving Shopify the flexibility to pursue opportunistic acquisitions or weather potential slowdowns.

Broader Market Context

Shopify’s resurgence aligns with renewed optimism in the global tech sector. As inflation cools and interest-rate expectations ease, investors have rotated back into high-growth digital platforms capable of converting scale into durable profits. For Shopify, that shift is particularly significant: its business model now benefits from both consumer demand resilience and merchants’ need for omnichannel tools that unify online and physical sales.

Still, competition is fierce. Amazon continues to encroach on merchant services, and emerging players like TikTok Shop and Temu are redefining the consumer funnel. Shopify’s long-term success will depend on defending its merchant base while deepening integrations that make its platform indispensable.

See Shopify’s full financial results & estimates (It’s free) >>>

1. Growth Momentum and Product Innovation

Shopify’s evolution from a storefront builder to a global commerce infrastructure company is unlocking new growth vectors. The launch of Shopify Magic and Sidekick, its AI-powered merchant assistants, enhances store optimization and customer analytics, helping merchants automate workflows and boost conversion. International expansion also remains a powerful lever, with European GMV up 42% year over year.

Enterprise adoption is another standout. Shopify Plus continues to gain traction among large retailers seeking flexibility and lower costs than legacy enterprise software. This mix of SMB and enterprise clients broadens Shopify’s revenue durability while raising average revenue per user (ARPU), a key margin driver for 2026 and beyond.

2. Valuation at a Crossroads

At nearly 18x forward sales, Shopify trades at one of the richest valuations in the global tech sector. That multiple assumes uninterrupted growth and continued margin expansion, a high bar in an environment where global retail spending remains uneven. Investors appear to be pricing in a best-case scenario, leaving a limited cushion if macro conditions deteriorate or if merchant churn rises.

While the company’s fundamentals are excellent, valuation discipline matters. Even modest revenue deceleration could quickly compress multiples, especially given profit margins still below peers like Adobe or Intuit. For long-term investors, the trade-off is clear: exceptional quality, but at an exceptional price.

Value stocks like Shopify in less than 60 seconds with TIKR (It’s free) >>>

3. Profitability, Cash Flow, and Scale

Shopify’s capital-light model continues to scale efficiently. With gross profit of US $1.3 billion in Q2 and eight consecutive quarters of positive free cash flow, the company has established a clear profitability track record. Operating leverage from cloud infrastructure optimization and reduced fulfillment expenses has also helped offset increased R&D spending.

Looking ahead, management’s focus is on maintaining profitability while expanding strategic partnerships, including payment integrations, logistics providers, and AI infrastructure vendors. The result should be consistent cash flow growth and the capacity for continued reinvestment, even as macro volatility persists.

The TIKR Takeaway

Shopify’s 2025 rebound has been impressive and deserved. The company has executed a difficult transition from growth-at-all-costs to sustainable profitability without losing momentum. Its global platform scale, strong balance sheet, and deep ecosystem make it a dominant force in e-commerce infrastructure. For growth-focused investors, it remains one of Canada’s most influential companies globally.

Yet, with the stock up nearly 107% over twelve months and trading at an 18x sales multiple, much of that optimism is already embedded in the price. The fundamentals are outstanding, but expectations are sky-high. Unless Shopify can deliver another leg of margin expansion or unveil a breakthrough AI-driven monetization stream, near-term upside may be limited. Long-term holders can stay confidently invested, but new buyers may want to wait for a pullback before adding exposure.

Should You Buy, Sell, or Hold Shopify Stock in 2025?

Shopify remains one of the strongest growth franchises in Canada, but the stock’s valuation leaves little margin for error. Investors should stay the course for compounding potential, while keeping expectations and position sizes in check.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!