Eli Lilly and Company (NYSE: LLY) has become a market favorite for its groundbreaking diabetes and obesity drugs. Shares trade around $825/share, off their highs but still reflecting confidence in its blockbuster pipeline. Despite short-term volatility, analysts see strong earnings growth ahead, supported by expanding margins and leadership in the fast-growing obesity market.

Recently, Eli Lilly reported strong Q3 2025 results that topped expectations, driven by robust demand for its weight-loss treatments Mounjaro and Zepbound. The company also announced encouraging late-stage data for its new oral GLP-1 candidate orforglipron, signaling another potential growth driver in its obesity portfolio. These developments reinforce Lilly’s momentum as it scales production and extends its leadership in metabolic health.

This article explores where Wall Street analysts think Eli Lilly could trade by 2027. We have pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Limited Upside

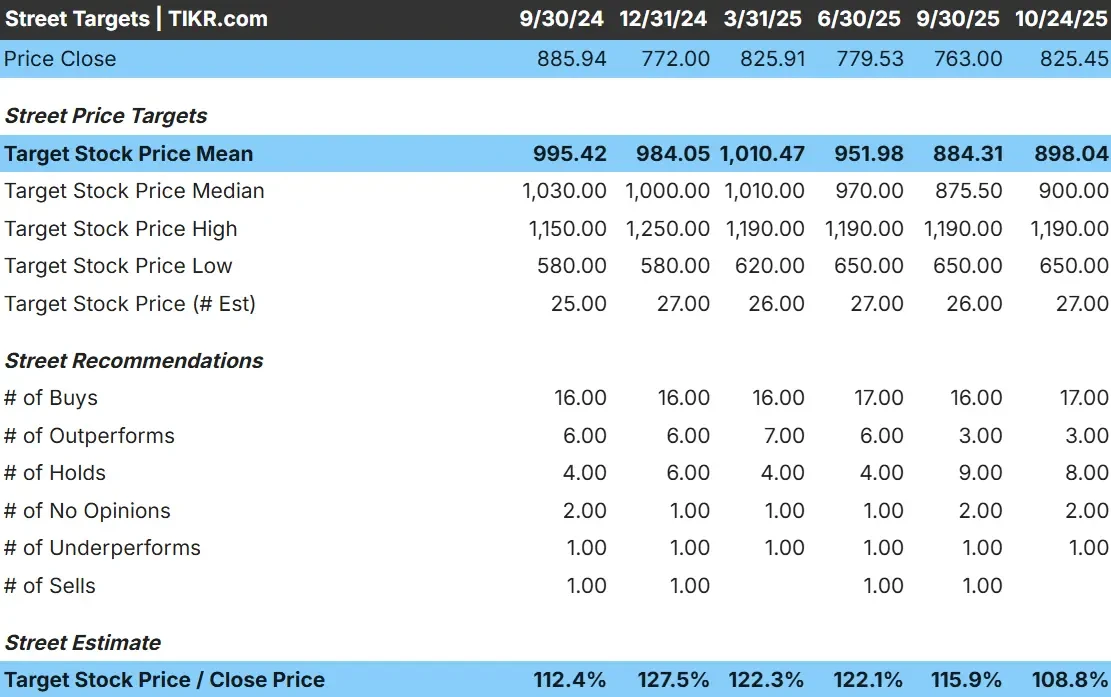

Eli Lilly trades around $825/share today. The average analyst price target is $898/share, which points to about 9% upside. Forecasts show a wide range and reflect mixed sentiment among Wall Street analysts:

- High estimate: ~$1,190/share

- Low estimate: ~$650/share

- Median target: ~$900/share

- Ratings: 17 Buys, 3 Outperforms, 8 Holds, 1 Underperform

It looks like analysts see limited room for gains, suggesting the stock may already price in much of its recent success. For investors, the near-term upside appears muted, but long-term potential remains tied to continued growth in obesity and diabetes treatments like Mounjaro and Zepbound.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Eli Lilly: Growth Outlook and Valuation

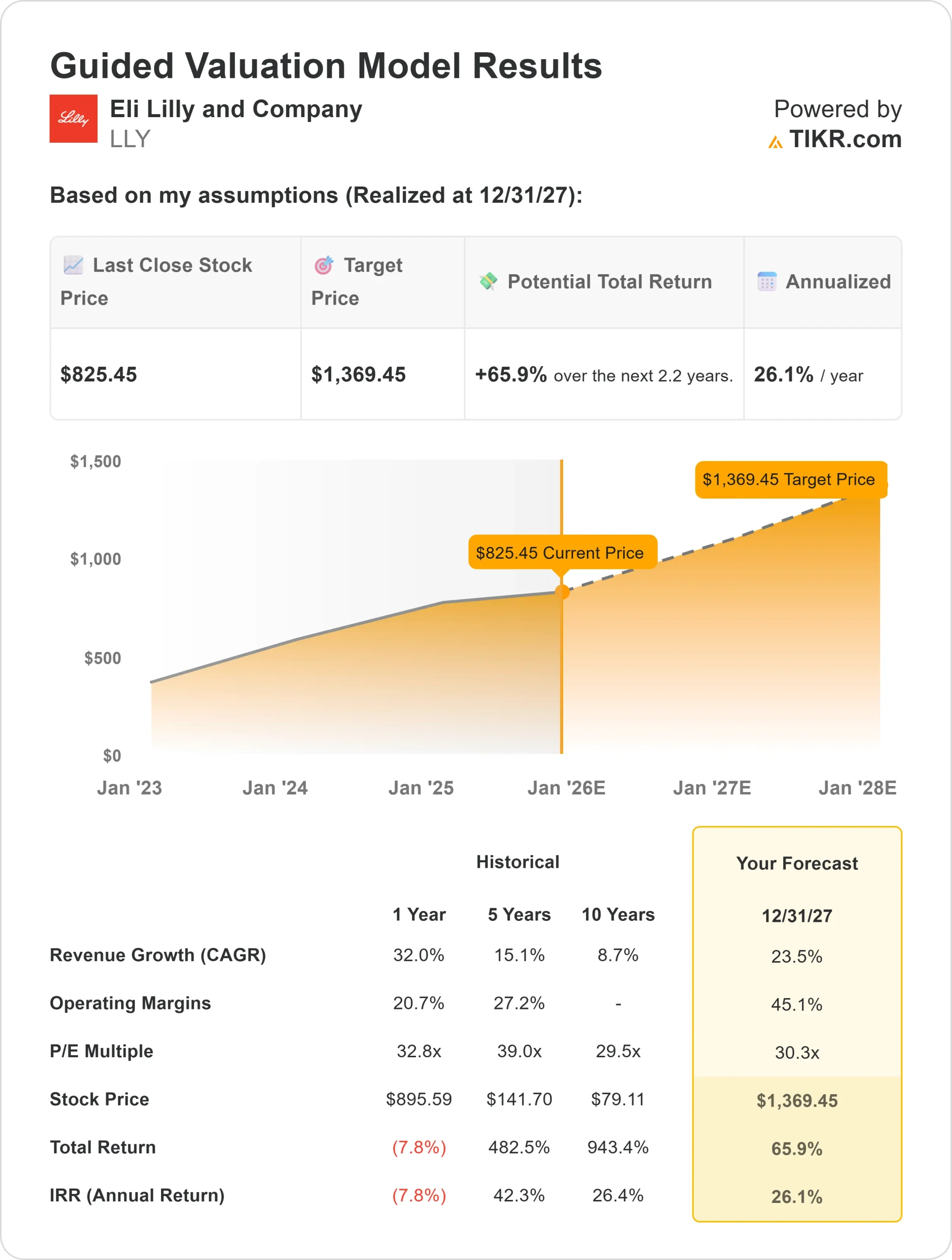

Eli Lilly’s financial foundation remains one of the strongest in global healthcare:

- Revenue is projected to grow about 23% annually through 2027

- Operating margins are expected to hold near 45%

- Shares trade around 30x forward earnings, slightly above the sector average

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 30x forward P/E suggests ~$1,369/share by 2027

- That implies roughly 66% total returns, or about 26% annualized, signaling strong upside potential

For investors, these metrics suggest Eli Lilly remains a high-quality compounder with exceptional growth and profitability. The valuation looks full, but it appears warranted given the company’s dominance in obesity and diabetes care, coupled with its expanding Alzheimer’s pipeline.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Eli Lilly’s leadership in obesity and diabetes treatments remains the biggest driver of investor confidence. Mounjaro and Zepbound continue to see strong global demand, positioning Lilly at the center of one of the fastest-growing markets in healthcare. The company is also expanding manufacturing capacity to meet surging prescriptions, helping protect its dominant market share.

Beyond obesity, new data from its Alzheimer’s candidate donanemab and pipeline programs in oncology and inflammation show that Lilly’s innovation engine remains robust. For investors, these strengths suggest Lilly can keep compounding earnings through 2027, supported by durable pricing power and high-margin growth in next-generation treatments.

Bear Case: Valuation and Competition

Even with outstanding fundamentals, Lilly’s valuation looks demanding. The stock trades around 30x forward earnings, well above peers in large-cap pharma. Much of the obesity drug success may already be priced in, leaving limited cushion if sales growth moderates or competitors close the gap.

Novo Nordisk remains the biggest rival in weight-loss treatments, and new entrants could pressure pricing over time. For investors, the risk is that expectations for sustained hypergrowth may prove too optimistic if the obesity market normalizes faster than projected.

Outlook for 2027: What Could Eli Lilly Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 30x forward P/E suggests Eli Lilly could trade near $1,369/share by 2027. That represents about 66% total upside, or 26% annualized returns.

This outlook assumes continued momentum in obesity drugs, strong margin expansion, and a steady stream of pipeline approvals. To exceed that target, Lilly would need to sustain double-digit revenue growth and successfully diversify beyond its metabolic franchise.

For investors, Eli Lilly stands out as a high-quality growth compounder. The upside potential looks meaningful, but valuation discipline and long-term execution will determine how much more room this market leader has to run.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.