Illumina, Inc. (NASDAQ: ILMN) has been through a tough stretch as growth slowed and investor confidence fell. Shares trade near $100, far below prior highs, after years of declining sales and management uncertainty. But analysts now see signs of stabilization as the company refocuses on profitability and its core sequencing markets.

Recently, Illumina reported quarterly results showing improved margin trends while maintaining its annual outlook. In January 2025, the company upgraded its NovaSeq X platform with a single-flow-cell system and new software kits to boost sequencing efficiency. Later in September, Illumina announced new partnerships with major pharmaceutical firms to develop companion diagnostics using its TruSight Oncology portfolio, highlighting its growing role in precision medicine. These developments suggest Illumina is gradually regaining its footing after several challenging years.

This article explores where Wall Street analysts think Illumina could trade by 2027. We have compiled consensus forecasts and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Illumina trades around $100/share today. The average analyst price target is approximately $113/share, which points to about 13% upside. Forecasts remain wide and show mixed conviction:

- High estimate: ~$185/share

- Low estimate: ~$75/share

- Median target: ~$110/share

- Ratings: 7 Buys, 1 Outperforms, 9 Holds, 2 Underperforms, 1 Sell

Analysts see a slow path to recovery as Illumina rebuilds margins and investor confidence. For investors, expectations are muted, but the setup looks better than it has in years if management continues executing on cost control and platform innovation.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

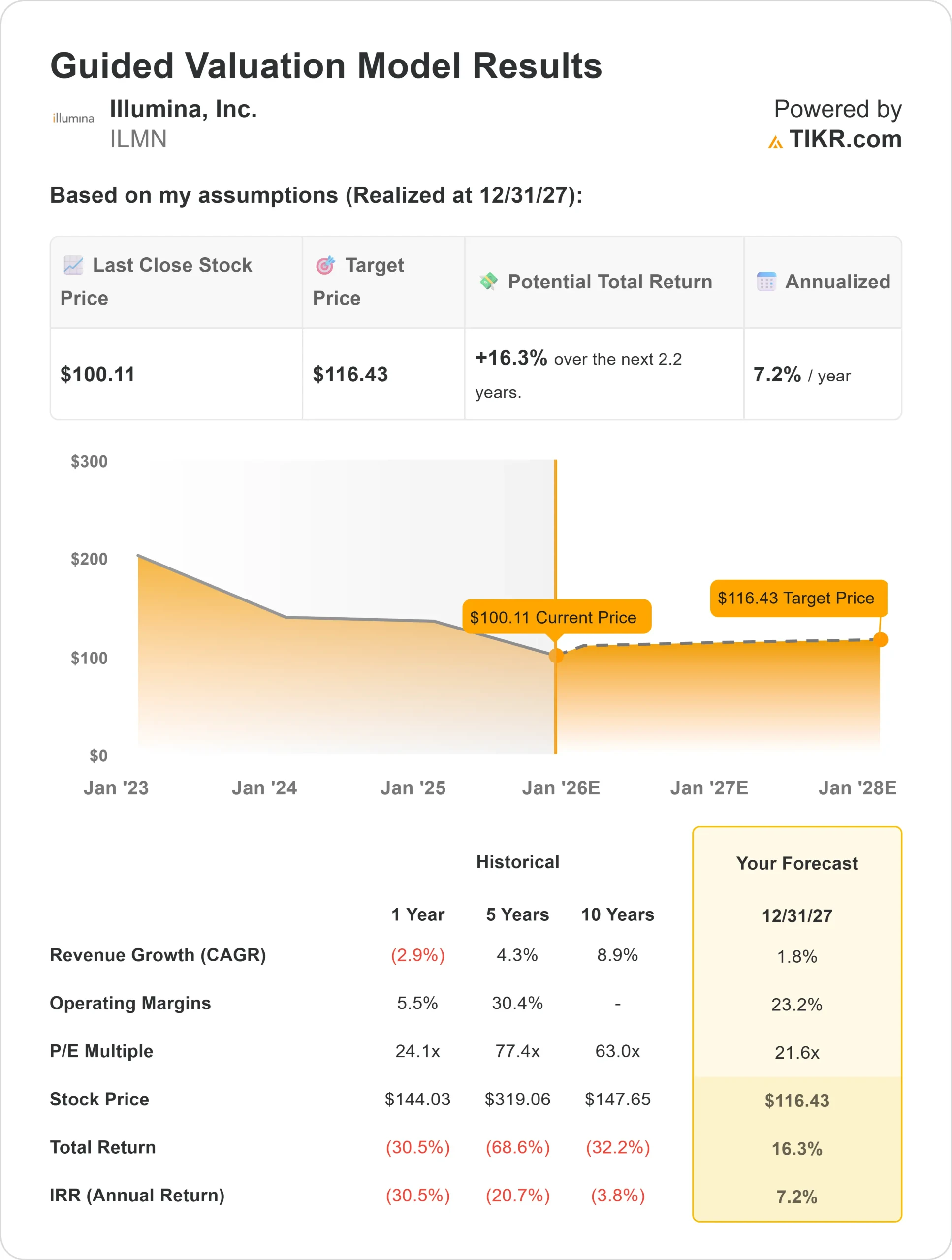

Illumina: Growth Outlook and Valuation

Illumina’s fundamentals are gradually improving, though growth remains modest:

- Revenue is projected to grow roughly 2% annually through 2027

- Operating margins are expected to reach around 23%

- Shares trade near 22x forward earnings, slightly below historical averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 21.6x forward P/E suggests ~$116/share by 2027

- That implies about 16% total upside, or roughly 7% annualized returns

These numbers point to a measured recovery. Illumina’s valuation already reflects cautious optimism, but stronger execution or faster adoption of new sequencing platforms could unlock more upside. For investors, the stock looks like a slow but steady compounder rather than a high-growth story.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Illumina remains the global leader in DNA sequencing, with technology used in everything from genetic research to precision medicine. Recent cost improvements and broader adoption of the NovaSeq X platform are helping rebuild momentum after several uneven quarters.

The company’s expansion into clinical and oncology diagnostics offers new long-term growth opportunities. Its renewed focus on profitability and operational discipline is improving margins and restoring confidence among investors.

For investors, these strengths suggest Illumina is on a gradual recovery path. Continued innovation and disciplined cost management could support steady earnings growth and renewed investor trust.

Bear Case: Growth and Execution Risks

Even with improving profitability, Illumina still faces meaningful challenges. The genomics industry has become more competitive, and research funding remains sensitive to economic conditions. Slower adoption of new sequencing platforms or weaker demand from research labs could delay the recovery.

Valuation also looks balanced rather than cheap, suggesting limited upside if growth continues at the current pace.

For investors, the main risk is that Illumina’s turnaround takes longer than expected. Without stronger revenue momentum, the stock may continue to trade sideways even as operations improve.

Outlook for 2027: What Could Illumina Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 21.6x forward P/E suggests Illumina could trade near $116/share by 2027. That would represent about 16% total upside, or roughly 7% annualized returns from current levels.

This base case assumes modest growth and improving profitability. Faster adoption of clinical sequencing or continued margin expansion could lead to stronger returns, but the current valuation already prices in a slow recovery.

For investors, Illumina appears to be a measured turnaround story. Its steady profitability, balance sheet strength, and global leadership position make it suitable for patient investors looking for gradual compounding rather than explosive growth.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.