Key Stats for Hub Group Stock

- Past-Week Performance: +10%

- 52-Week Range: $30.8 to $53.3

- Current Price: $43.1

What Happened?

A $77 million accounting error spanning three quarters has reset Hub Group‘s investment thesis entirely, sending shares to $43.08 while three separate securities fraud investigations from Levi & Korsinsky, Pomerantz LLP, and Bleichmar Fonti and Auld pile pressure onto an already battered stock sitting 19.1% below its 52-week high.

Accelerating the selloff, the February 5 Form 8-K disclosure triggered an immediate 18.3% single-day collapse, with subsequent reporting confirming the total decline exceeded 24% as analysts rapidly issued downgrades and steep price target cuts following confirmation that internal controls over financial reporting were ineffective for all of 2025.

Beneath the accounting crisis, the operational picture tells a starkly different story, as Q4 intermodal on-time performance improved 90 basis points YoY, Mexico volumes surged 33%, refrigerated volumes jumped 150%, and full-year operating cash flow held firm at $194 million despite a challenging freight market cycle.

Consequently, the market is forcibly re-rating Hub Group from a steady logistics compounder to an accounting risk story, stripping away the credibility premium the stock had earned through record service levels and disciplined capital returns while investors wait for restated financials before rebuilding any conviction.

President and CEO Phillip Yeager stated on the Q4 earnings call that “accuracy and transparency in reporting on our performance is of the utmost importance at Hub Group, and we have taken steps to strengthen and enhance our controls,” contextualizing management’s response as the company simultaneously delayed its Form 10-K and faced three active securities fraud probes.

Adding complexity to the recovery thesis, analysts issued rapid downgrades and steep price target cuts following the disclosure, while the company still holds $142 million in share repurchase authorization and continues paying a $0.125 quarterly dividend, signaling that balance sheet strength remains intact even as credibility repair takes center stage.

Looking across the next three to five years, Hub Group’s ability to rebuild investor trust through clean restated financials, combined with rail consolidation expected in 2027 and $3.65 billion to $3.95 billion in 2026 revenue guidance, will determine whether this accounting crisis becomes a footnote or a permanent discount in the stock’s multiple.

Wall Street’s Take on HUBG Stock

The $77 million restatement clouds near-term earnings visibility, but the mid-case DCF still points to meaningful upside once clean financials restore investor confidence.

Meanwhile, the fundamentals show stabilization: revenue declines decelerate from 7% in 2025 to just 2.7% growth in 2026, while EPS recovers 14.7% to $2.10.

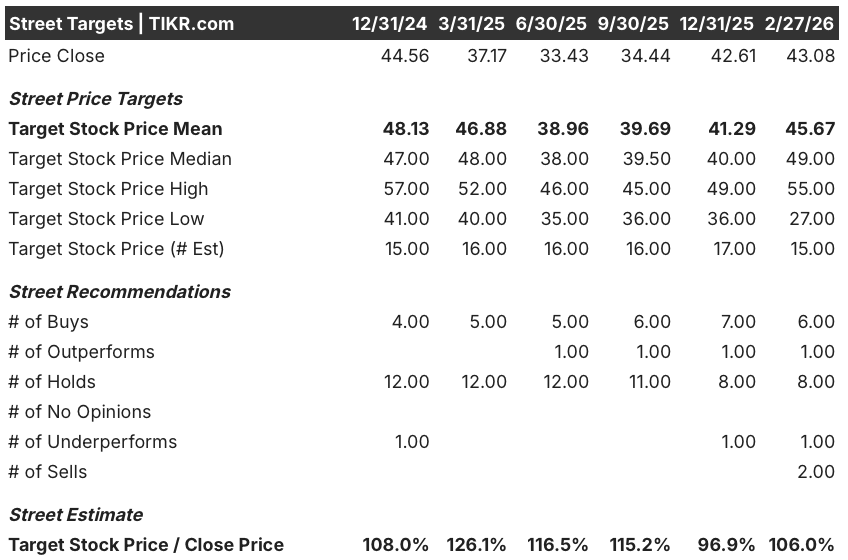

Despite the accounting crisis, Wall Street maintains a mean target of $45.67 across 6 buys, 1 outperform, 8 holds, and 2 sells, implying 6% upside from $43.1.

However, the target spread is wide: the high of $55 requires clean restated financials and freight market recovery, while the low of $27 reflects full accounting fraud confirmation.

What Does the Valuation Model Say?

Even with accounting uncertainty, Hub Group’s $194 million operating cash flow and a 4.4% revenue CAGR through 2030 support the mid-case target of $70.36, implying 63.3% total return at a 13.6% annualized IRR.

The market is currently treating Hub Group’s accounting error as a fraud story rather than a controls failure, ignoring that cash flow remained completely unaffected across all restated periods.

Hub Group’s $194 million operating cash flow confirms the underlying business generated real cash despite the $77 million bookkeeping error.

Management’s active $142 million share repurchase authorization confirms executives view the current price as a buying opportunity, not a distress signal.

Critically, if restated financials reveal the error was larger or broader than the disclosed $77 million, EPS already compressing from $1.91 to an estimated $1.83 in 2025 faces further downside risk that directly undermines the recovery thesis.

Therefore, watch for the Form 10-K filing date and the final restated figures, since any upward revision to the $77 million understatement resets the entire forward earnings baseline.

HUBG is a wait-and-see at $43.08 until the restated 10-K confirms the accounting error is contained, because the 63.3% upside potential is real but entirely contingent on that single disclosure.

Should You Invest in HUBG, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HUBG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HUBG, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HUBG stock on TIKR for Free →