Key Stats for HON Stock

- Year-to-Date Performance: 24%

- 52-Week Range: $169 to $246

- Valuation Model Target Price: $291

- Implied Upside: 20.3%

Value your favorite stocks like Honeywell International with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Honeywell stock is up about 24% year to date, recently trading near $242 per share as strong aerospace demand, solid automation execution, and steady institutional accumulation supported the rally. Shares are now approaching their 52 week high of $246, reflecting sustained buying interest rather than a short term spike.

With the stock trading at roughly 32x trailing earnings based on $7.58 EPS, investors are paying a premium for visibility into 2026 growth.

The move higher has been reinforced by institutional buying and portfolio positioning around Honeywell’s aerospace and automation exposure. Westerkirk Capital opened a new 4,400 share position valued at about $926,000, Stevens Capital purchased 10,875 shares worth roughly $2.29 million, and ANTIPODES PARTNERS acquired 15,154 shares valued at approximately $3.19 million.

Fiera Capital boosted its stake by 83.3% to 45,411 shares worth $9.56 million, while Ontario Teachers Pension Plan increased its holdings by 7.0% to 642,389 shares valued at about $135.2 million. Institutional ownership now stands near 75.9%, signaling broad professional conviction behind the stock’s advance.

Selective trimming suggests profit taking rather than distribution. Jupiter Asset Management reduced its stake by 20.3%, King Luther Capital cut its position by 18.6%, and Northeast Investment Management lowered its holdings by 8.3%.

Woodley Farra Manion trimmed its position by 1.6% to 331,565 shares valued at about $69.79 million, while Director D. Scott Davis sold 2,367 shares at an average price of $240 for total proceeds of $568,080, reducing his stake by 7.08%. The overall pattern reflects repositioning near highs rather than weakening fundamentals.

Earlier this month at Citi’s Global Industrial Tech & Mobility Conference, CEO Vimal Kapur said momentum from 2025 continues into 2026, with Aerospace and Building Automation remaining strong and long cycle process orders growing for two consecutive quarters.

The LNG business is booked through late 2027 and into early 2028, Building Automation grew 7% in 2025 driven by 4% new product growth and 3% pricing, and management expects pricing to remain in the 3% to 4% range this year.

Kapur added that the company will “work very hard to be on the upper end of our guidance,” reinforcing confidence in Honeywell’s 2026 outlook.

See analysts’ growth forecasts and price targets for Honeywell International (It’s free) >>>

Is HON Undervalued?

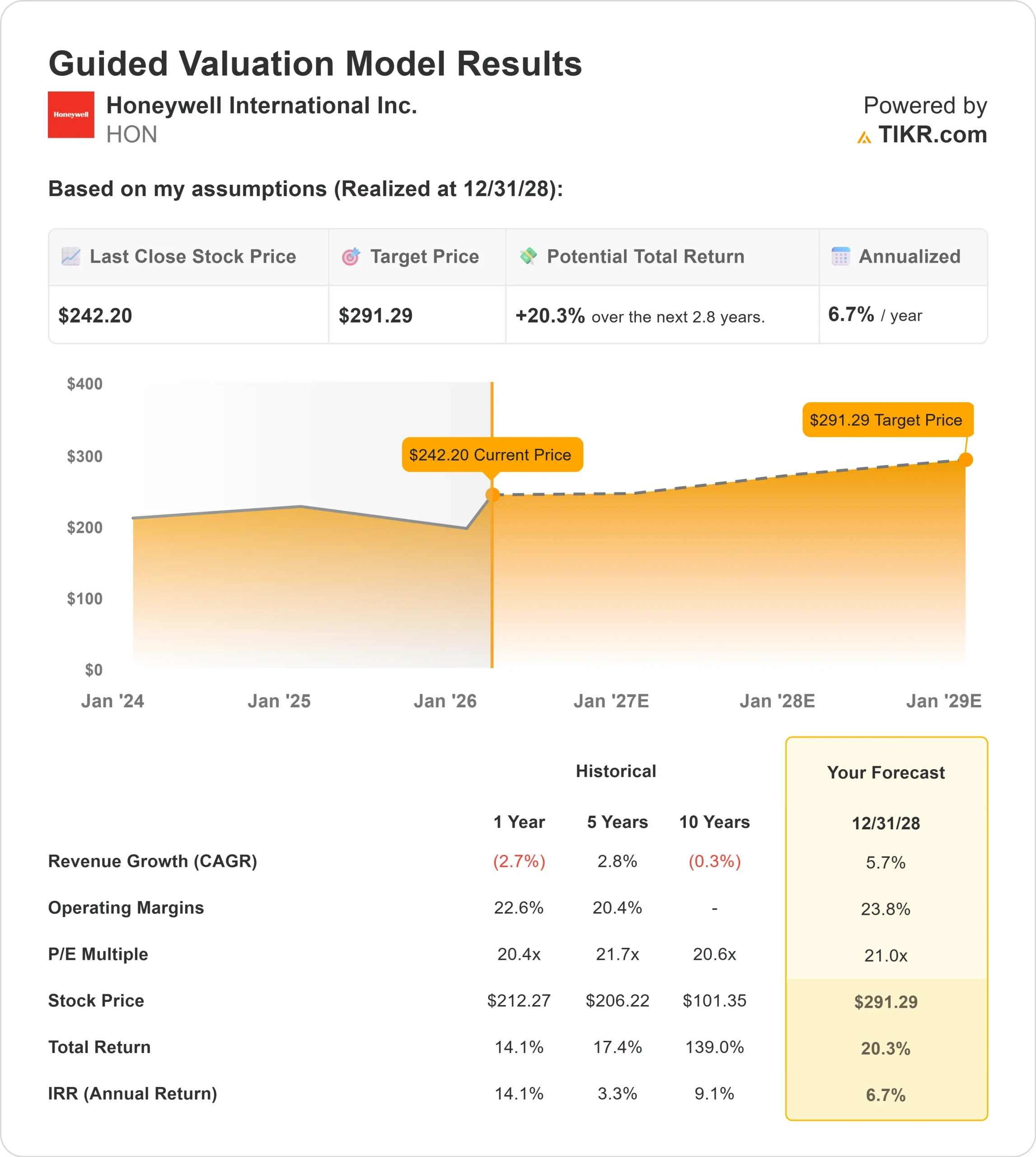

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 5.7%

- Operating Margins: 23.8%

- Exit P/E Multiple: 21x

Revenue growth is expected to be supported by commercial aerospace recovery, strong defense demand, warehouse automation upgrades, and energy efficiency investments in building systems rather than broad industrial acceleration.

Margin expansion toward 23.8% depends on mix shift into higher margin Aerospace Technologies, continued new product penetration in automation, disciplined pricing in a 3% to 4% inflation environment, and improved cost structure within Industrial Automation following portfolio repositioning.

Aircraft engine aftermarket demand remains one of the most important earnings drivers, as service revenue carries structurally higher margins than original equipment. Long cycle LNG and refining capacity investments, combined with growing installed base penetration in automation and services, provide multi year visibility.

Free cash flow conversion and balance sheet flexibility strengthen the outlook, supporting dividends, buybacks, and bolt on acquisitions without stretching leverage.

Based on these inputs, the valuation model estimates a target price of $291, implying about 20% total upside from current levels near $242.

At current levels, Honeywell appears modestly undervalued, with 2026 performance likely driven by aerospace aftermarket strength, backlog execution, and disciplined capital allocation rather than aggressive revenue acceleration.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>