Key Stats for Elevance Health Stock

- Past-Week Performance: -9.4%

- 52-Week Range: $273.7 to $458.8

- Current Price: $280.7

What Happened?

Elevance Health (ELV), one of America’s largest health insurers is trading 39% below its 52-week high at $280.74 after a March 31 regulatory deadline threatens to suspend new enrollment in its Medicare Advantage prescription drug plans, forcing management to reaffirm a guidance cut to at least $25.50 adjusted EPS for 2026.

On February 27, CMS, the federal agency overseeing Medicare and Medicaid, notified Elevance it would halt new enrollments in its Medicare Advantage drug plans over alleged data submission failures dating to November 2018, sending shares down roughly 3% on March 2 and triggering a securities-law investigation by Johnson Fistel on March 3.

The deeper problem is that the CMS sanctions arrive on top of a deliberate membership contraction already in motion: management guided to a high-teens percentage decline in Medicare Advantage members in 2026 while Medicaid margins are expected to hit a trough of -1.75%, conditions peer Centene also flagged when it reported elevated medical cost ratios of 94.3% in Q4.

A notable insider buy emerged on March 6 when director Steven H. Collis acquired 3,000 shares at prices near the 52-week low, providing a concrete signal of internal conviction at the exact moment regulatory pressure reached its peak.

CEO Gail Boudreaux stated on the Q4 2025 earnings call that “based on the actions underway this year, we remain confident in our long-term algorithm and our expectation to return to at least 12% adjusted EPS growth in 2027,” directly tying the recovery timeline to the March 31 CMS resolution and the Carelon services platform’s external growth pipeline.

With $2.3 billion in planned share repurchases, at least $5.5 billion in 2026 operating cash flow, and Carelon Services delivering 60% growth in FY2025 as an independent revenue engine serving external clients, the structural case for ELV rests on whether the March 31 CMS deadline passes without escalation.

Wall Street’s Take on ELV Stock

The March 31 CMS enrollment suspension, which covers new members entering Medicare Advantage drug plans, creates near-term noise around a stock whose core earnings recovery thesis does not depend on Medicare Advantage membership growth to work.

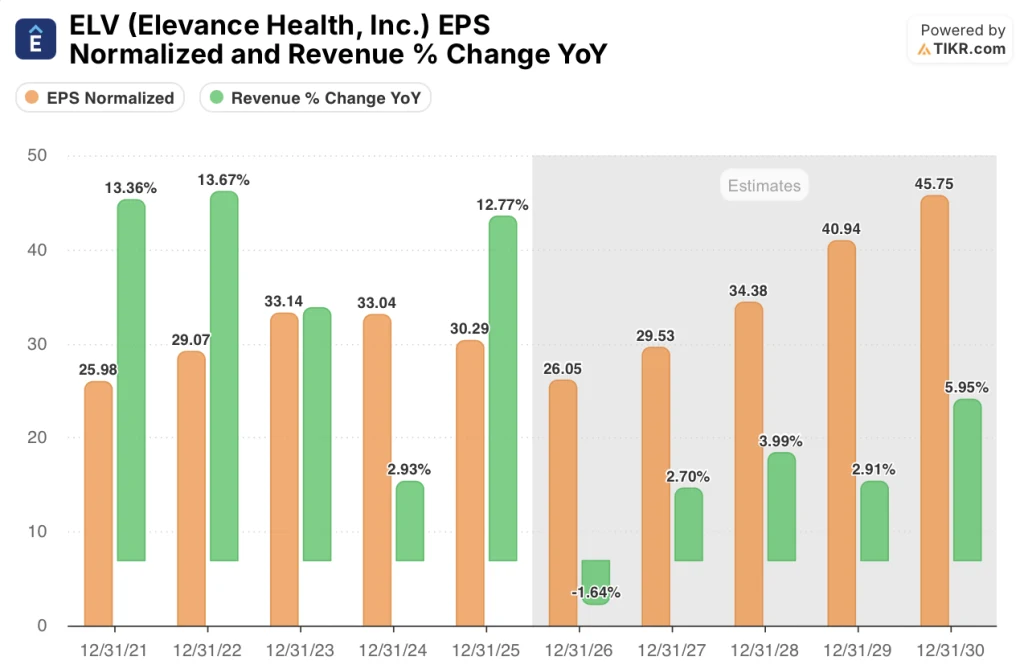

TIKR’s estimates show normalized EPS troughing at $26.05 in FY2026 before accelerating to $29.53 in FY2027, a 13.4% rebound that management explicitly committed to on the January 28 earnings call when it reaffirmed at least 12% adjusted EPS growth in 2027 off the 2026 baseline.

The revenue picture confirms the trough thesis: after a projected -1.6% decline to $194.4 billion in FY2026, consensus models a return to growth at 2.7% in FY2027 and 4% in FY2028 as Medicaid rates catch up to trend and Carelon Services, the company’s external health management platform, scales its pipeline.

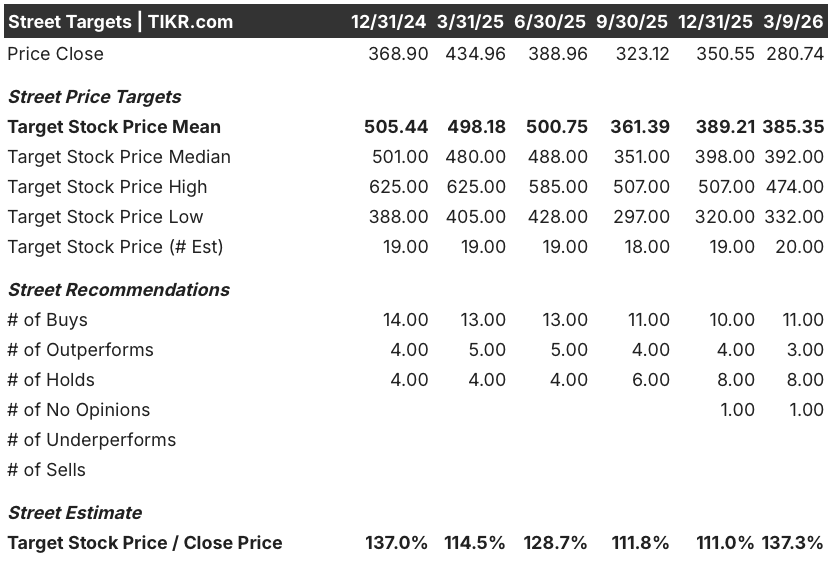

Despite the 39% collapse from the 52-week high, Wall Street has not abandoned the stock: 11 buys and 3 outperforms against only 8 holds and zero sells, with a mean price target of $385.35 implying 37.3% upside from the March 9 close of $280.74.

The target range spans $332.00 on the low end to $474.00 on the high end, with the floor anchored to a scenario where CMS sanctions escalate beyond the March 31 enrollment suspension and the ceiling contingent on Medicaid rates normalizing and the 2027 EPS recovery arriving on schedule.

What Does the Valuation Model Say?

TIKR’s mid-case model prices ELV at $412.38 by December 2030, implying 46.9% total return at an 8.3% annualized IRR, driven by mid-case EPS CAGR of 2.4% and net income margin recovering from 2.9% in FY2026 toward 3.1% as the Medicaid trough passes and Medicare margins improve by over 100 basis points.

The market is pricing ELV as though the 2026 EPS trough is the new normal, yet the TIKR model requires only 2.4% EPS CAGR to reach $412, a fraction of the 6.5% CAGR already embedded in the 10-year consensus.

Director Steven H. Collis purchased 3,000 shares on March 6 near the 52-week low, providing the clearest internal signal that the regulatory selloff has created a valuation disconnect the people closest to the company are willing to act on.

Carelon Services, the company’s externally facing health management unit that generated 60% revenue growth in FY2025, provides an earnings floor independent of the Medicare and Medicaid membership headwinds driving the current selloff.

If CMS escalates sanctions beyond the March 31 enrollment suspension or Medicaid rates fail to converge toward trend in 2026, the -1.75% Medicaid margin assumption breaks and the 2027 EPS recovery timeline shifts, undermining the model’s $412 target.

The March 31 CMS deadline is the single most important near-term event: watch whether Elevance resolves the risk-adjustment data submission issue before sanctions take effect, and whether the $25.50 adjusted EPS guidance holds intact on the next earnings call.

Should You Invest in Elevance Health, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ELV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elevance Health, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ELV stock on TIKR for Free →