Key Takeaways:

- EX Growth Engine: Employee experience business crossed $510M in ARR with 26% year-over-year growth, driving upmarket momentum.

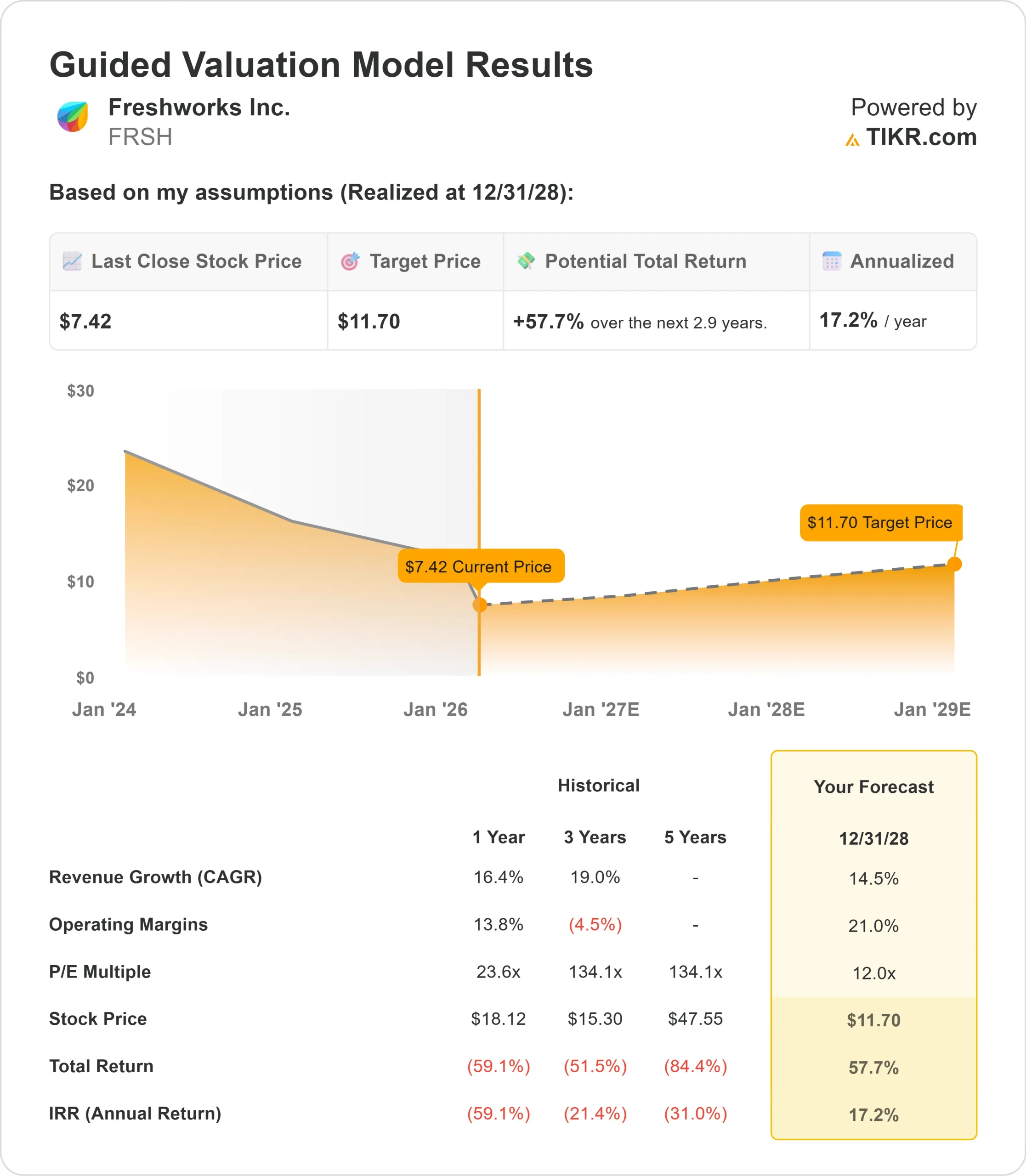

- Price Projection: Based on current execution, FRSH stock could reach $11.70 by December 2028.

- Potential Gains: This target implies a total return of 58% from the current price of $7.42.

- Annual Return: Investors could see roughly 17% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Freshworks (FRSH) delivered exceptional results in Q4, marking the company’s first profitable full year while generating record free cash flow. The software maker now projects sustained growth and profitability exiting 2026.

CEO Dennis Woodside highlighted the company’s transformation into a world-class unified service platform.

- Revenue grew over 14% year-over-year to $223 million in Q4, topping estimates by nearly $3 million.

- The company achieved a 19% non-GAAP operating margin and 25% free cash flow margin, marking the sixth consecutive quarter of Rule of 40 performance.

- Enterprise momentum surged with larger customer cohorts outpacing overall growth. Freshworks now serves over 1,500 customers with more than $100,000 in ARR, up 28% year-over-year, while customers above $50,000 in ARR grew 23% to over 3,700.

- The employee experience business reached a major milestone, crossing $510 million in ARR and growing 26%.

- Freshworks is capturing mid-market organizations demanding sophisticated AI-native service management that deploys in weeks rather than years.

- Device42, the IT asset management solution, ended 2025 with over $40 million in ARR and showed a 30% attach rate on the top 50 new deals.

- Freshworks’ AI platform, Freddy AI, is proving to be a tangible revenue engine. Over 8,000 customers now use Freddy AI, generating more than $25 million in ARR.

- The technology deflects over 50% of tickets for both customer and employee experience users.

- Customers using AI products showed significantly higher retention, with net dollar retention improving from 112% to 116% quarter over quarter.

Despite strong fundamentals and clear momentum in the mid-market, Freshworks trades at $7.42, offering upside for investors who recognize the company’s position in the rapidly growing service management sector.

See analysts’ full growth forecasts and estimates for FRSH stock (It’s free) >>>

What the Model Says for Freshworks Stock

We analyzed Freshworks as it evolved into a comprehensive service management platform serving mid-market enterprises.

- The company benefits from multiple demand drivers. In employee experience, organizations between $1 billion and $3 billion in revenue are seeking alternatives to expensive legacy platforms.

- These customers need sophisticated software that meets complex needs with a fast time-to-value.

- Freshworks has assembled a complete platform covering ITSM, ITAM through Device42, ESM through Freshservice for Business Teams, and now ITOM with the FireHydrant acquisition.

- This unified approach opens an $8 billion addressable market while providing expansion opportunities within existing customers.

- The AI business represents significant upside. With only 8,000 of 75,000 total customers using paid AI features, a substantial penetration opportunity remains.

- Management expects AI to reach $100 million in ARR by 2028.

Using a forecast of 14.5% annual revenue growth and 21% operating margins, our model projects the stock will rise to $11.70 within 2.9 years. This assumes a 12x price-to-earnings multiple.

That represents compression from Freshworks’ historical P/E averages of 23.6x (one year) and 134.1x (three years). The lower multiple acknowledges the company’s transition phase as it moves upmarket and scales profitability, while also reflecting current market skepticism.

The real value lies in capturing the massive mid-market opportunity where Freshworks is displacing entrenched competitors, expanding through multiple product lines, and scaling AI monetization.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Freshworks stock:

1. Revenue Growth: 14.5%

Freshworks’ growth centers on capturing mid-market share in the employee experience space.

The company delivered 26% growth in its EX business in Q4, with continued momentum from Device42, ESM, and now FireHydrant integration.

Management raised full-year 2026 guidance to 14% growth at the midpoint, up from prior expectations.

The pipeline for deals over $100,000 reached record levels entering 2026.

Customer references and win rates continue improving as the unified platform story resonates with CIOs evaluating alternatives to legacy systems.

2. Operating margins: 21%

Freshworks expanded non-GAAP operating margins by nearly 500 basis points over the 2025 estimate through disciplined execution and operational efficiency.

The company achieved profitability for the first time while investing heavily in the high-growth EX business.

Management expects margins to expand throughout 2026, exiting Q4 at approximately 23.5%.

This reflects the benefit of scale as the company grows revenue while managing the CX business for efficiency.

3. Exit P/E Multiple: 12x

The market values Freshworks at 12.9x current earnings. We assume the P/E will compress slightly to 12x over our forecast period.

Near-term uncertainty from the stock’s significant decline weighs on the multiple.

However, as Freshworks demonstrates consistent execution on its mid-market strategy and proves AI monetization at scale, the company should command a higher valuation.

The company’s position as a disruptor in a massive market with improving unit economics supports multiple expansions over time.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

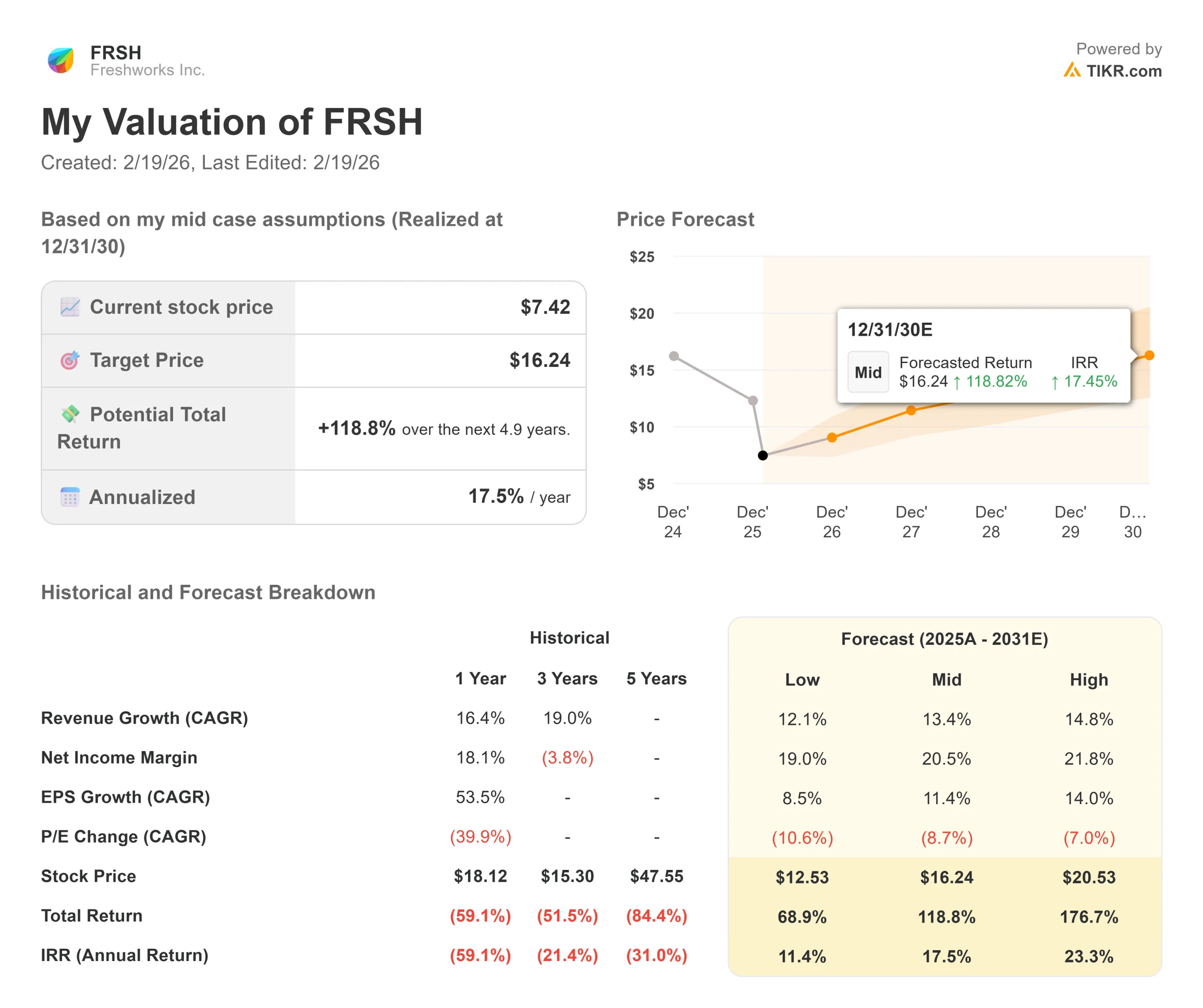

Software companies face execution risk and market adoption challenges. Here’s how Freshworks stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 12.1% and net income margins compress to 19%, investors still see a 69% total return (11% annually).

- Mid Case: With 13.4% growth and 20.5% margins, we expect a total return of 119% (17.5% annually).

- High Case: If mid-market adoption accelerates to 14.8% revenue growth while Freshworks maintains 21.8% margins, returns could hit 177% total (23% annually).

See what analysts think about FRSH stock right now (Free with TIKR) >>>

The range reflects execution on the unified platform strategy, AI penetration in the customer base, and the ability to sustain momentum in the competitive mid-market.

In the low case, competitive pressure intensifies, or AI adoption disappoints.

In the high case, the company captures market share faster than expected, and AI becomes a larger revenue driver sooner.

How Much Upside Does Freshworks Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!