Key Takeaways:

- AI Shopping Assistant: 600 million users now engage with an AI-powered visual discovery platform.

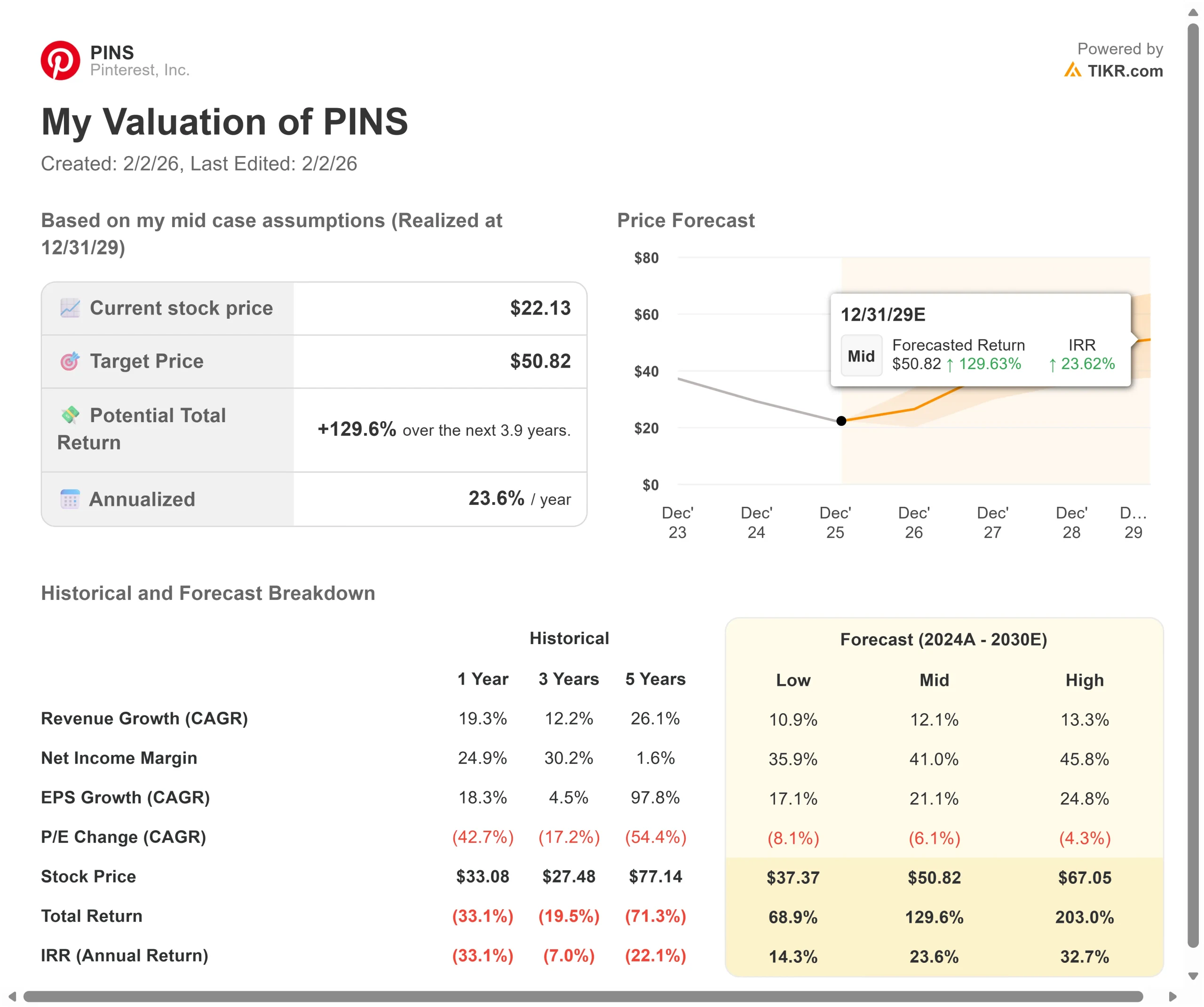

- Price Projection: Based on current execution, PINS stock could reach $30 by December 2027.

- Potential Gains: This target implies a total return of 38% from the current price of $22.

- Annual Return: Investors could see roughly 18% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Pinterest (PINS) just posted its ninth consecutive quarter of record users, reaching 600 million monthly active users while delivering $1.05 billion in Q3 revenue.

The company grew sales by 17% in 2025, transforming from a window-shopping platform into an AI-powered visual search and shopping destination.

CEO Bill Ready is executing a strategy centered on performance advertising and international expansion.

The company generated 40% more clicks for advertisers in Q3, up more than 5x over the past three years. Shopping ads now account for 30% of international revenue, up from 9% two years ago.

Despite strong momentum in user growth and engagement metrics, Pinterest stock trades at $22, offering upside for investors who recognize the platform’s unique position in visual commerce.

See analysts’ full growth forecasts and estimates for PINS stock (It’s free) >>>

What the Model Says for Pinterest Stock

We analyzed Pinterest’s transformation into a visual-first shopping assistant, leveraging unmatched first-party intent data.

- The company is expanding beyond traditional social discovery.

- Recent launches such as Pinterest Assistant and multimodal search create conversational experiences in which users can describe complex needs and receive personalized product recommendations.

- With 80 billion monthly queries on the platform, Pinterest captures commercial intent in the critical discovery phase.

- The platform serves over 600 million logged-in users who actively curate 15 billion boards.

- This creates intent signals found nowhere else, powering AI models that outperform off-the-shelf alternatives by 30% in recommendation relevance.

- Nearly 85% of users come directly to the mobile app, reducing reliance on third-party traffic sources.

Using a forecast of 14.9% annual revenue growth and 11.1% operating margins, our model projects the stock will rise to $30 within 1.9 years. This assumes a 12.5x price-to-earnings multiple.

That represents compression from Pinterest’s historical P/E averages of 23.3x (three years) and 32.8x (five years).

The lower multiple acknowledges near-term headwinds from tariff-related advertiser pullbacks and competitive pressures in digital advertising.

The real value lies in monetizing international users, expanding Performance+ adoption, and deepening share of wallet with mid-market advertisers.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PINS stock:

1. Revenue Growth: 14.9%

Pinterest’s growth centers on three key drivers: international monetization, Performance+ automation, and catalog depth.

- The company achieved 17% revenue growth in Q3 2025, with particularly strong performance internationally.

- Europe revenue grew 41% while the Rest of World expanded 66%.

- These regions account for 83% of global users but only 25% of revenue, creating significant monetization upside.

- Pinterest Performance+ campaigns are delivering results, with retail advertisers seeing a 24% lift in conversions compared with traditional campaigns.

- The company just launched ROAS bidding two quarters ago, which doubled the number of unique shopping SKUs with paid impressions.

Management sees a significant runway to capture more advertiser budgets as smaller and mid-market advertisers adopt automated tools.

2. Operating margins: 11.1%

Pinterest is demonstrating clear operating leverage while investing in AI.

The company delivered a 29% adjusted EBITDA margin in Q3, up 170 basis points year over year. This reflects disciplined cost management as the platform scales its infrastructure to support 12% user growth and deepen engagement.

Management is approaching its 30-34% adjusted EBITDA margin target range set at the 2023 Investor Day.

As international revenue scales and AI tools improve campaign performance, margins should continue expanding from current levels.

3. Exit P/E Multiple: 12.5x

The market values Pinterest at 12.5x earnings. We assume the P/E will remain at this level over our forecast period.

The compressed multiple reflects several factors: uncertainty about major retailers’ spending amid tariff pressures, competitive dynamics in performance advertising, and the time required to fully monetize international markets.

As Pinterest demonstrates consistent execution on Performance+ adoption, international ARPU growth, and AI-driven engagement, the platform should maintain or expand its valuation multiple.

The company’s proprietary taste graph and visual search capabilities create defensible differentiation in an increasingly AI-driven advertising landscape.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Digital advertising platforms face economic cycles and technology disruption. Here’s how Pinterest stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 10.9% and net income margins compress to 35.9%, investors still see a 68.9% total return (14.3% annually).

- Mid Case: With 12.1% growth and 41.0% margins, we expect a total return of 129.6% (23.6% annually).

- High Case: If international momentum accelerates and Pinterest maintains 45.8% margins while growing at 13.3%, total returns could reach 203.0% (32.7% annually).

See what analysts think about PINS stock right now (Free with TIKR) >>>

The range reflects execution on international expansion, Performance+ adoption rates, and margin improvement as revenue scales.

In the low case, advertiser spending remains pressured, or competition intensifies for performance budgets.

In the high case, international ARPU closes the gap with North America faster than expected; Gen Z engagement drives higher monetization; and AI features deliver stronger advertiser ROI.

How Much Upside Does Pinterest Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!