Key Stats for AES Stock

- Past-Week Performance: 8%

- 52-week Range: $9 to $16

- Valuation Model Target Price: $18

- Implied Upside: 19.4% over 1.9 years

Value your favorite stocks like The AES Corporation with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

AES stock rose about 8% over the past week, finishing near $16 after breaking out to a new 52-week high of $15.75 earlier in the week. The move pushed shares to the top of their recent range and marked one of the stock’s strongest weekly gains in months.

The stock moved higher as increased bullish positioning followed the breakout, reflecting expectations for additional upside.

On Tuesday alone, 28,249 AES call options were purchased, about 88% above the typical daily call volume of 15,024, indicating heightened interest after shares cleared prior resistance levels.

Analyst actions reinforced the rally. Argus Research upgraded AES to Buy, while Mizuho upgraded the stock to Outperform, lifting the broader analyst consensus to Moderate Buy with an average price target of $23.83. The upgrades helped validate the price move and supported follow-through buying during the week.

Recent portfolio updates also shaped sentiment. AES Andes abandoned a planned $10 billion green hydrogen and ammonia project in Chile, redirecting capital toward core renewable energy and storage investments.

Separately, AES disclosed it expects to record a $250 million to $325 million pre-tax impairment charge related to its Maritza coal-fired power plant in Bulgaria, reflecting uncertainty after the plant’s power purchase agreement expires in May 2026, with no replacement agreement yet in place.

See analysts’ growth forecasts and price targets for The AES Corporation (It’s free) >>>

Is AES Undervalued?

Under valuation assumptions, the stock is modeled using:

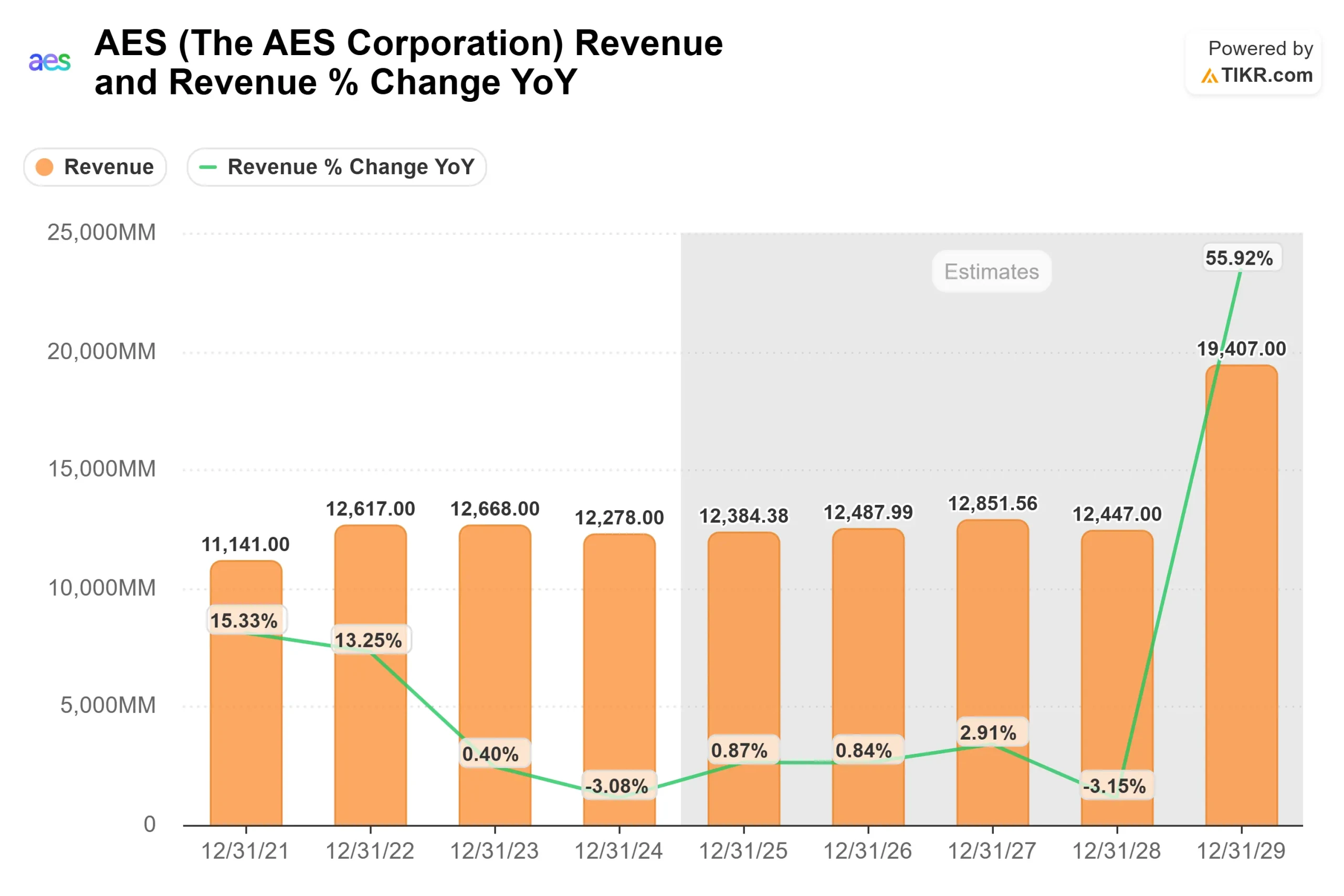

- Revenue Growth (CAGR): 1.5%

- Operating Margins: 21.9%

- Exit P/E Multiple: 7.5x

Revenue growth has been uneven over time, reinforcing expectations for modest top-line expansion rather than a sustained reacceleration.

This supports the view that future returns depend more on execution and efficiency than on faster revenue growth.

EBIT and margins have declined as AES exited legacy assets and absorbed higher costs during its transition toward renewables.

That pressure explains why profitability, rather than revenue growth, has been the primary constraint on valuation.

AES is trading near the low end of its historical forward P/E range, with the current multiple well below its long-term average.

The discounted valuation reflects margin pressure and portfolio transition risk rather than deterioration in the company’s largely contracted cash flow base.

Based on these inputs, the model estimates a target price of $18, implying 19.4% total upside from recent levels over the next 1.9 years, indicating the stock is undervalued at current prices.

Results over the next year hinge on execution within AES’s contracted renewable backlog, particularly utility-scale solar and wind projects supported by long-term power purchase agreements that improve cash flow visibility.

At current levels, AES appears undervalued, with future performance driven by steady execution and balance sheet progress rather than aggressive top-line growth.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>