Key Takeaways:

- CTV Revolution: Connected TV remains the fastest-growing channel, with decisioning becoming the default buying model.

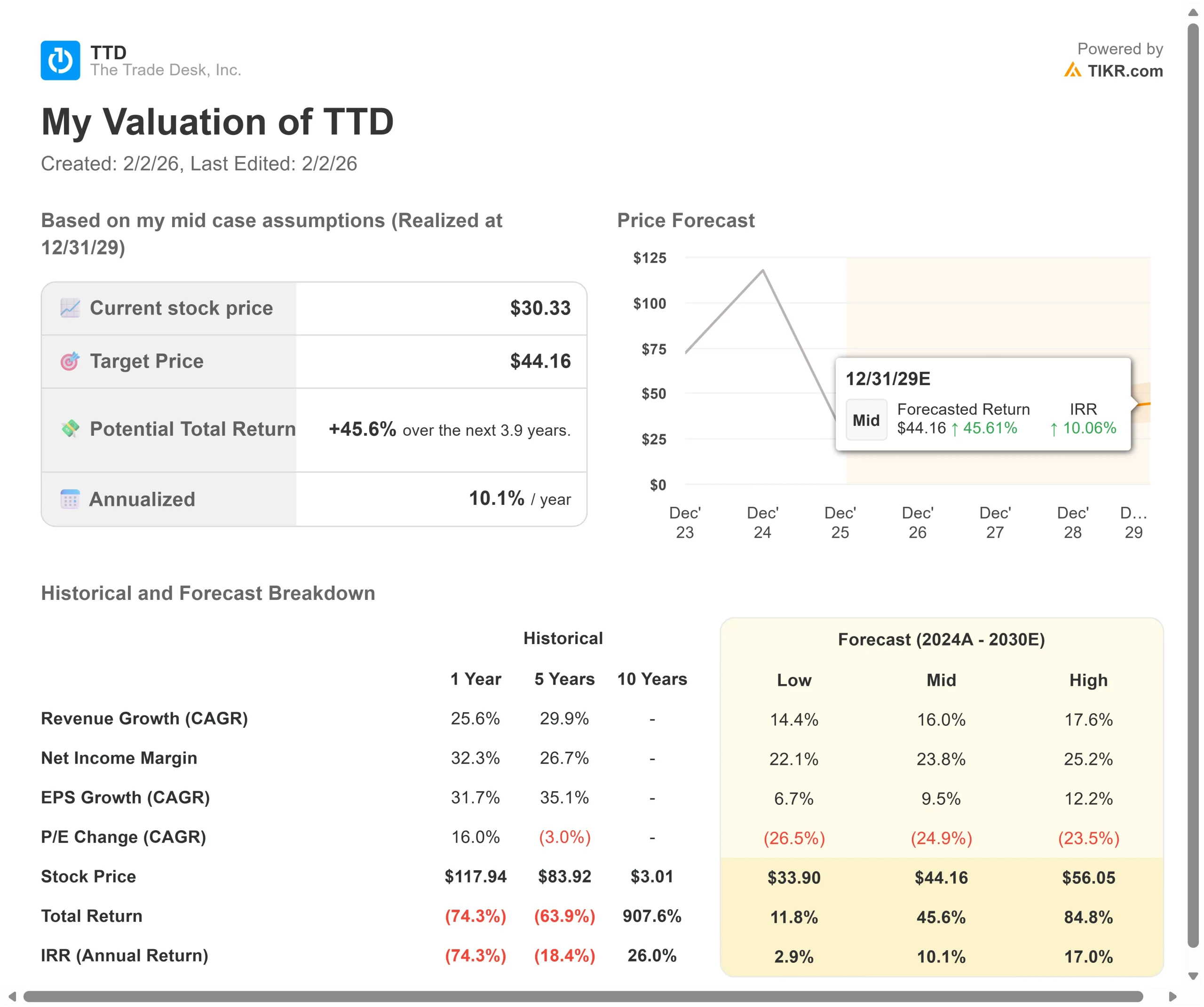

- Price Projection: Based on current execution, TTD stock could reach $37 by December 2027.

- Potential Gains: This target implies a total return of 21% from the current price of $30.

- Annual Return: Investors could see roughly 10% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

The Trade Desk (TTD) posted 18% revenue growth in Q3, reaching $739 million. Excluding political spending, the growth rate jumped to 22%.

CEO Jeff Green is executing an aggressive AI-powered transformation of programmatic advertising with new products such as Kokai, delivering a 26% lower cost per acquisition than previous versions.

The company now has over 180 active joint business plans with major brands, collectively worth billions, and CTV continues to outpace overall business growth.

New CFO Alex Kayyal brings a fresh growth mindset after serving on the board for 13 years, while the addition of former Google executive Anders Mortensen as CRO strengthens the go-to-market organization.

Despite strong momentum with products like OpenPath growing by hundreds of percentage points, The Trade Desk stock trades at $30, down significantly from its 2021 peak, but offering upside for investors who recognize the company’s position in the open Internet advertising revolution.

See analysts’ full growth forecasts and estimates for TTD stock (It’s free) >>>

What the Model Says for The Trade Desk Stock

We analyzed The Trade Desk’s transformation into the dominant independent demand-side platform for the open Internet, with unmatched AI capabilities and objectivity.

The company is capitalizing on the shift from walled gardens to the open Internet.

- With Kokai adoption at nearly 85% and campaigns showing 94% better click-through rates, The Trade Desk is delivering unprecedented performance improvements.

- The platform’s distributed AI architecture breaks down every function into separate models, enabling parallel innovation that competitors can’t match.

- The company now serves the world’s largest advertisers at global scale. Joint business plans are growing significantly faster than non-JBP accounts, demonstrating the value of deeper brand relationships.

- With no conflicts of interest from owned inventory, The Trade Desk maintains pure buy-side alignment that becomes more valuable as AI makes advertiser data increasingly critical.

Using a forecast of 16.5% annual revenue growth and 22.2% operating margins, our model projects the stock will rise to $37 within 1.9 years. This assumes a 14.4x price-to-earnings multiple.

That represents significant compression from The Trade Desk’s historical P/E averages of 31.6x (one year) and 65.4x (five years).

The lower multiple acknowledges intense competition from tech giants and the ongoing transition to newer products and go-to-market strategies.

The real value lies in capturing the shift of advertising dollars to the open Internet while maintaining operational discipline and leveraging AI to drive superior campaign performance.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TTD stock:

1. Revenue Growth: 16.5%

The Trade Desk’s growth centers on three massive shifts in digital advertising.

CTV continues growing faster than the overall business, now representing roughly half of total revenue alongside other video formats.

The decisioning model is becoming the default for CTV buying, replacing legacy programmatic guaranteed approaches.

International markets are growing significantly faster than North America, with EMEA and APAC showing strong momentum.

Given that 60% of the $1 trillion advertising TAM sits outside the U.S., this geographic expansion provides substantial runway.

The company is also capturing retail media spend as more shopper marketing budgets flow into programmatic.

2. Operating margins: 22.2%

The Trade Desk is expanding profitability while investing heavily in platform innovation.

The company delivered an adjusted EBITDA margin of 43% in Q3, demonstrating the inherent operating leverage in its business model.

New CFO Alex Kayyal is bringing fresh discipline to resource allocation and metrics-driven management across the organization.

Recent operational improvements under COO Vivek Kundra include a streamlined go-to-market organization, automated workflows for traders and account managers, and standardized account planning for high-growth clients.

These efficiency gains support margin expansion even as the company invests in AI and new product development.

3. Exit P/E Multiple: 14.4x

The market values The Trade Desk at 15.4x earnings. We assume the P/E will compress slightly to 14.4x over our forecast period.

Near-term headwinds include intense competition from Google, Amazon, and other tech giants, who are offering zero-fee DSP products to gain market share.

The company must successfully execute its leadership transition with new executives in critical roles while maintaining growth momentum.

However, The Trade Desk’s structural advantages should support premium valuation.

The platform’s pure buy-side positioning, distributed AI architecture, and products like Deal Desk and Audience Unlimited create genuine differentiation.

As the open Internet captures more advertiser spend and The Trade Desk demonstrates consistent execution, the market should recognize this leadership position.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Programmatic advertising faces technology disruption and shifting spending patterns. Here’s how The Trade Desk stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 14.4% and net income margins compress to 22.1%, investors still see an 11.8% total return (2.9% annually).

- Mid Case: With 16.0% growth and 23.8% margins, we expect a total return of 45.6% (10.1% annually).

- High Case: If CTV and retail media accelerate and The Trade Desk maintains 25.2% margins while growing at 17.6%, returns could hit 84.8% total (17% annually).

See what analysts think about TTD stock right now (Free with TIKR) >>>

The range reflects execution on product innovation, successful integration of new leadership, and the pace of advertiser migration from walled gardens to the open Internet.

In the low case, tech giants succeed with aggressive zero-pricing strategies or AI search disrupts display advertising more than expected.

In the high case, CTV decisioning adoption accelerates, joint business plans exceed expectations, and Kokai’s performance advantages drive market share gains faster than anticipated.

How Much Upside Does The Trade Desk Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!