Key Stats for DE Stock

- Past-6-Month Performance: 27%

- 52-Week Range: $404 to $674

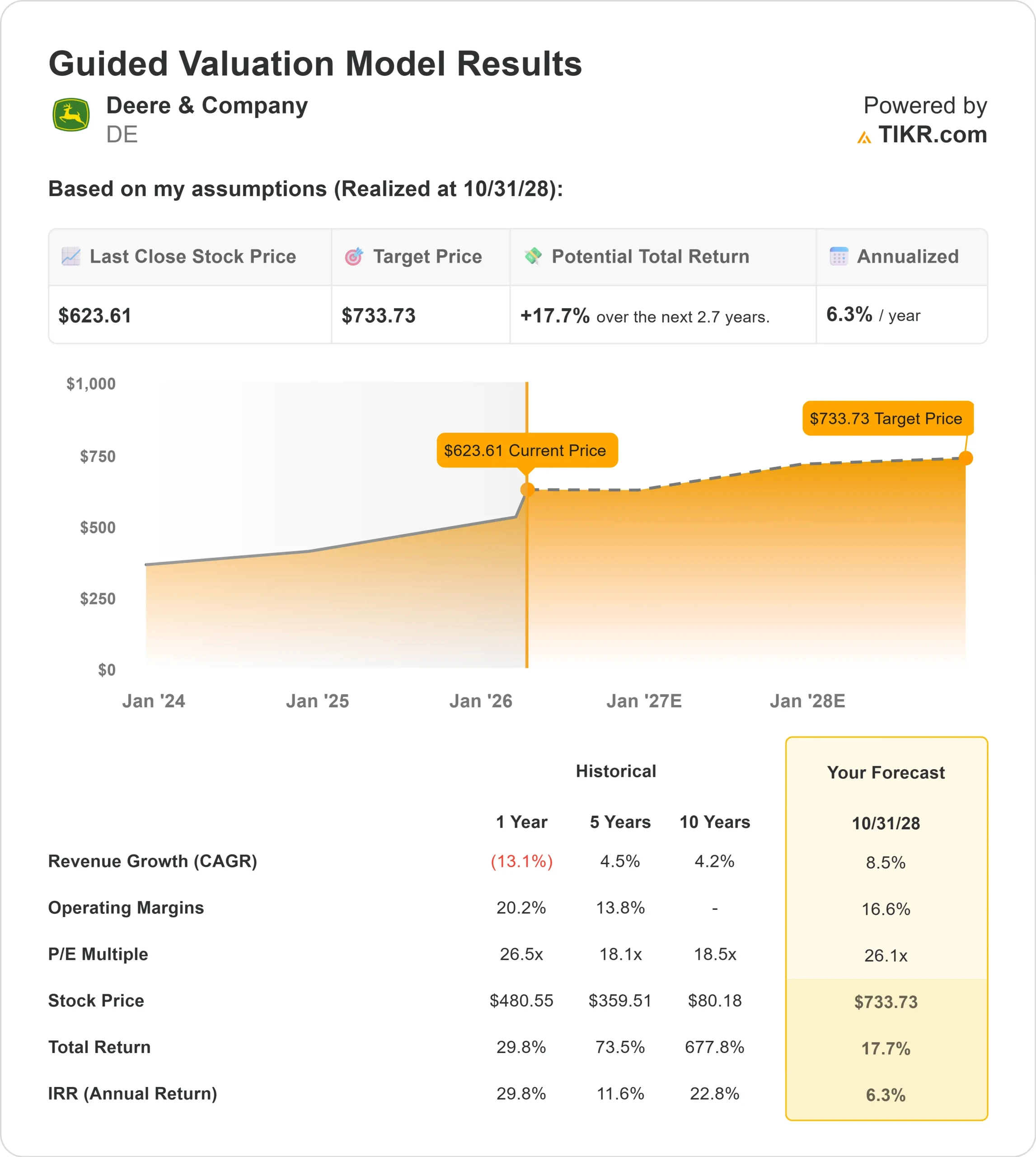

- Valuation Model Target Price: $734

- Implied Upside: 18%

Value your favorite stocks like Deere & Company with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Deere & Company stock shares are up about 27% over the last six months, recently trading near $620 per share, as investors re-rated the stock on signs that fiscal 2026 could mark the bottom of the agricultural cycle while construction demand accelerates.

The rally has pushed shares near the upper end of their $404 to $674 52-week range, reflecting improving earnings visibility and stronger backlog trends.

The advance has been driven by stronger-than-expected earnings, rising order momentum, and a series of bullish analyst updates.

DA Davidson raised its price target from $580 to $775 and reiterated a Buy rating, implying roughly 25% upside from current levels, while Royal Bank of Canada lifted its target to $736 and maintained an Outperform rating, implying about 19% upside.

Institutional positioning remained active, with Rothschild & Co Wealth Management UK increasing its stake by 1.5% to 1,196,643 shares valued at about $547 million, Synovus Financial boosting its position by 50.8%, and Empirical Financial Services increasing its holdings by 62.0%.

While Granite Investment Partners and Kovitz Investment Group trimmed positions modestly, overall activity reflected continued engagement from large investors.

This week, Deere reported first quarter net sales and revenues up 13% to about $9.6 billion, with equipment operations net sales rising 18% to about $8.0 billion and net income of $656 million, or $2.42 per diluted share, as shipment volumes exceeded internal expectations.

Construction & Forestry sales surged 34% to $2.67 billion and Small Ag & Turf climbed 24%, prompting management to raise its full-year 2026 net income outlook to $4.5 billion to $5.0 billion and increase projected operating cash flow to between $4.5 billion and $5.5 billion.

The Construction & Forestry order bank rose more than 50% sequentially to its highest level since May 2024, and large tractor orders now extend into the fourth quarter.

Manager of Investor Communications Josh Beal said the quarter delivered “better top line and margins than originally forecasted,” reinforcing management’s view that 2026 marks the bottom of the current cycle.

Looking ahead, production alignment, improving used equipment inventories, and accelerating precision technology adoption are shaping expectations for margin recovery in 2026.

Construction momentum supported by infrastructure spending and data center demand provides a second earnings engine beyond agriculture.

With order books strengthening and cash flow guidance raised, Deere’s recent rally reflects improving visibility into next year rather than short-term momentum alone.

See analysts’ growth forecasts and price targets for Deere & Company (It’s free) >>>

Is DE Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 8.5%

- Operating Margins: 16.6%

- Exit P/E Multiple: 26.1x

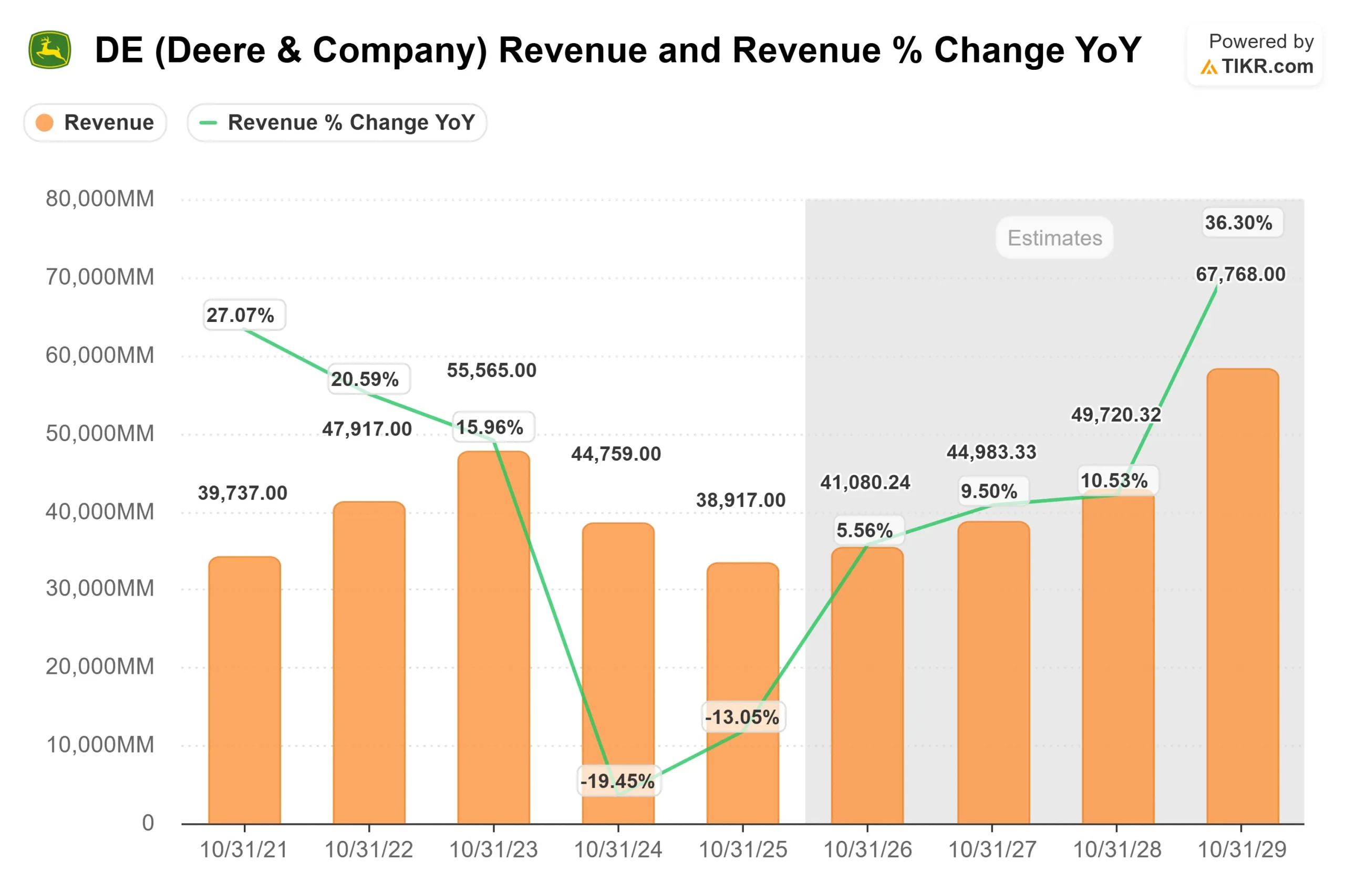

Revenue is projected to recover from cyclical trough levels, expanding toward the $50 billion to $68 billion range by 2029 as replacement demand returns and construction activity remains firm.

Margin assumptions near 16.6% reflect operating leverage from higher volumes, disciplined production alignment, and greater mix contribution from precision agriculture technology and connected machinery.

Based on these inputs, the model estimates a target price of $734, implying about 18% total upside over the next several years, indicating the stock appears modestly undervalued at current levels near $620.

The most important driver in 2026 is order conversion. The 50% increase in Construction & Forestry backlog, improved tractor order velocity, and healthier used equipment inventories reduce downside risk to production planning.

Precision technology adoption continues to expand, increasing revenue per machine and supporting structurally stronger margins over time.

Construction remains a critical growth engine. Infrastructure investment, rental fleet replenishment, and data center development are supporting retail settlements that were up mid-teens year over year in the first quarter. If those trends persist, incremental volume would flow through a lean cost base, enhancing earnings leverage.

Performance in 2026 will likely hinge on sustained order momentum, margin durability above 15%, and continued stabilization in global agricultural fundamentals.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>