Key Stats for Deckers Outdoor Stock

- Price Change for $DECK stock: -15%

- Current Share Price: $87

- 52-Week High: $224

- $DECK Stock Price Target: $116

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Deckers Outdoor (DECK) stock plummeted 15% on Friday after the Ugg and Hoka parent company issued weaker-than-expected full-year guidance, citing consumer pullback from tariffs and rising prices.

DECK stock has now lost more than half its value since the year began, reflecting concerns about the company’s ability to navigate the current environment.

Deckers expects full-year sales of about $5.35 billion with diluted earnings per share in the range of $6.30 to $6.39. Analysts surveyed had expected net sales of between $5.39 billion and $5.56 billion, making this a material top-line miss.

CEO Stefano Caroti told investors, “We are anticipating a more cautious consumer as the full impact of tariffs and price increases will be felt here in the U.S.”

CFO Steven Fasching said the headwinds from tariffs may be partially offset by mitigation strategies, including promotions to entice shoppers.

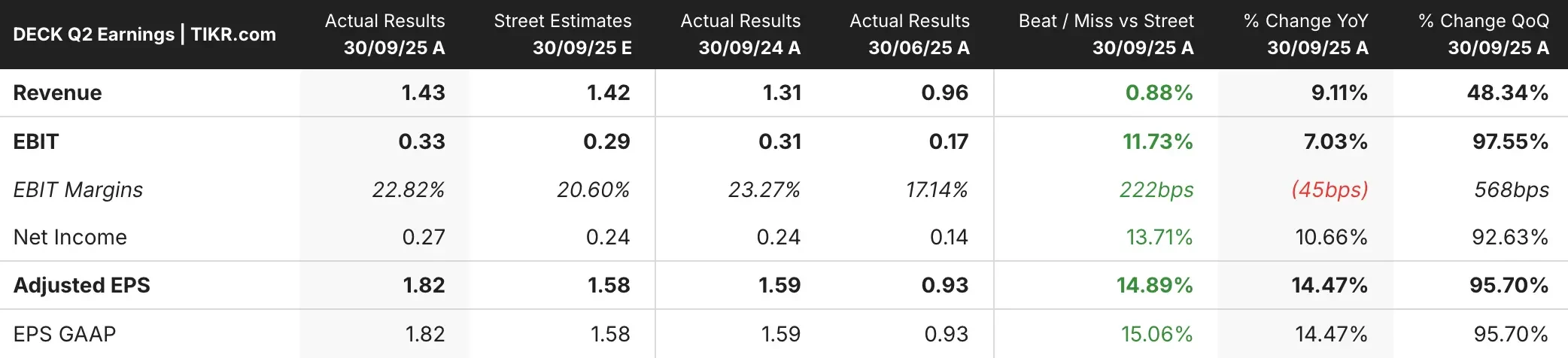

The weak outlook completely overshadowed strong fiscal Q2 results. The footwear maker reported revenue of $1.43 billion and adjusted earnings of $1.82 per share, beating estimates of $1.42 billion and $1.58 per share, respectively.

The results beat the company’s own expectations, which called for net sales of $1.38 billion to $1.42 billion and diluted earnings per share of $1.50 to $1.55.

See analysts’ growth forecasts and price targets for Deckers Outdoor stock (It’s free!) >>>

What the Market Is Telling Us About DECK Stock

The market’s brutal reaction to DECK stock shows investors are focused on the future, which looks increasingly challenging for footwear companies caught in the tariff crossfire.

Deckers delayed providing annual guidance last quarter due to “evolving global trade policy and related macroeconomic pressures,” so this was the first time investors got a full picture of management’s expectations.

Ugg sales surged 10.1% to $759.6 million in the second quarter, while Hoka sales grew 11.1% to $634.1 million.

Those are solid growth rates for mature brands, but the problem is sustaining that momentum when consumers are feeling squeezed and the company may need to raise prices or experience a decline in profit margins.

Sales of other brands dropped 26.5% to $37.2 million, reflecting the impact of phasing out the Koolaburra brand’s standalone operations. The “Other” brands division, which includes Teva and Ahnu, is clearly struggling and represents a drag on overall performance.

The direct-to-consumer channel saw net sales decline 0.8% to $394.6 million, while wholesale net sales increased 13.4% to $1.04 billion.

That wholesale growth is a positive, but DTC is typically higher margin, so seeing that channel go backward isn’t ideal for profitability.

For the full fiscal year 2026, Deckers expects Hoka to increase by a low-teens percentage versus last year, while Ugg is expected to increase by a low-to-mid-single-digit percentage.

That implies a significant deceleration in Ugg’s growth rate and suggests the brand may be maturing faster than investors hoped.

Caroti tried to strike an optimistic tone, saying “our brands’ ability to connect with consumers through leading innovative products differentiates Deckers in today’s dynamic and competitive marketplace.”

Caroti added that he’s “confident in our ability to achieve our fiscal year 2026 outlook, and continue to capture the significant opportunities ahead for Deckers.”

But DECK stock didn’t buy the optimism. When a company beats quarterly estimates and still gets hammered, it’s because investors don’t believe management’s forward guidance is conservative enough or they’re worried about factors outside management’s control, like tariffs and consumer spending.

The tariff situation is a significant headwind for footwear companies that manufacture overseas. Deckers will either need to absorb the costs, which lowers profit margins, or pass them to consumers, which risks volume declines.

CFO Fasching’s comment about using promotions to offset tariffs suggests the company may lean toward protecting volume at the expense of margins, which isn’t great for the bottom line.

The combination of tariff headwinds, consumer caution, and decelerating growth in key brands creates a difficult setup for near-term upside.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!