Key Stats for CrowdStrike Stock

- Current Price: $742.91

- Target Price (Mid): ~$1,230

- Street Target: ~$715

- Potential Total Return: ~66%

- Annualized IRR: ~12% / year

- Earnings Reaction: (3.81%) (June 3, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

CrowdStrike Holdings (CRWD) closed at $742.91 on June 29, up 5.96% in a single session, the last trading day before the first stock split in its history takes effect. The timing is not a coincidence. Investors are positioning ahead of a 4-for-1 split that begins trading on a split-adjusted basis on July 2.

A split changes nothing about what the business is worth. Four shares at one-quarter the price still equal the same company. Yet the stock now trades above the Street’s average target, the rally is accelerating, and the question underneath the excitement is sharper than the split chatter suggests. Has CrowdStrike grown into one of the richest valuations in large-cap software, or is the market paying for a story that still has to deliver?

That tension is real and unresolved. Bulls see a company that just raised its full-year recurring revenue outlook by 520 basis points. Bears see a stock at 98 times forward EV/EBITDA with insiders selling into the move. Both are looking at the same numbers and reaching opposite conclusions.

The Split Is the Headline, but the Quarter Is the Story

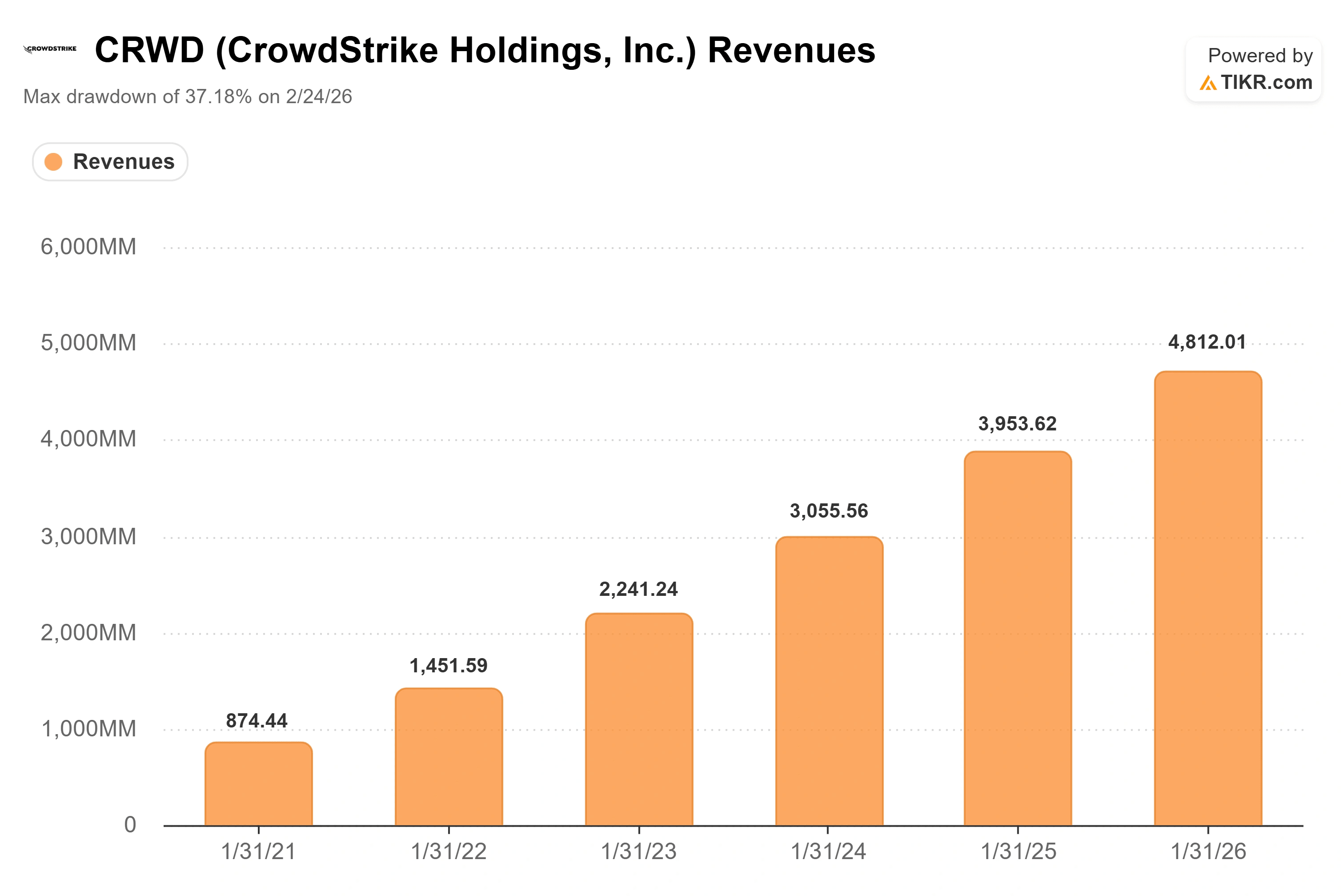

The split grabbed attention, but the catalyst that earned it came on June 3. CrowdStrike reported fiscal first-quarter 2027 results that beat across the board, and management raised full-year guidance for net new ARR, the annual recurring revenue added in a period, by 520 basis points at the midpoint.

The company posted record Q1 net new ARR of $255.8 million, up 32% year over year. Ending ARR reached $5.51 billion, accelerating to more than 24% growth. Revenue grew 26% to $1.39 billion, the fourth consecutive quarter of accelerating year-over-year growth. Free cash flow hit an all-time record of $468.5 million, or 34% of revenue.

CEO George Kurtz framed the quarter around a single idea. As he put it on the call, “CrowdStrike is now being understood as critical AI infrastructure.” That reframes the AI debate that haunted the stock earlier this year. The fear was that agentic AI would make security software obsolete. Management’s argument is the reverse: more AI means more attack surface, and more attack surface means more security spend.

The catalyst behind that claim has a name. Kurtz pointed to what he called the “Mythos moment” in April, when new frontier models from Anthropic and OpenAI drove a wave of enterprise demand to secure AI deployments. CrowdStrike was selected by both labs from the start to help secure their model rollouts, and the company turned that into a coalition it calls Project QuiltWorks. The numbers that followed were specific. CrowdStrike’s new AIDR product, which stands for AI detection and response, grew ending ARR more than 250% sequentially, with a Q2 pipeline already above $50 million. Kurtz called it a larger opportunity than the endpoint market the company built its business on, because, in his words, there will eventually be “90 agents per employee,” each one a new thing to protect.

See historical and forward estimates for CrowdStrike stock (It’s free!) >>>

Why the Market Reaction Is Not as Simple as It Looks

Here is the wrinkle. When the quarter actually dropped on June 3, the stock fell 3.81% that day. The 6% surge came three weeks later, as the split date approached and analysts revised targets upward. The market did not reward the print immediately. It warmed to the story over time.

That gap explains a lot about where CRWD sits today. The stock has roughly doubled off its 52-week low of $342.72 and now trades close to its 52-week high of $785.66. Investor anxiety is no longer about whether AI is a threat. It has shifted to whether a stock this expensive can keep climbing on momentum that a split does nothing to justify.

The valuation case is genuinely two-sided. CrowdStrike trades at 98 times forward EV/EBITDA and around 142 times forward earnings. Against software peers, that is in a category of its own. Datadog trades near 74 times forward EV/EBITDA and Palo Alto Networks near 54 times, while the broader software peer set sits at a median closer to 11 times. CrowdStrike commands a premium of more than eight times the median on that measure. The bull answer is that no peer combines its growth rate, its 79% gross margins, and its 34% free cash flow margin. The bear answer is that even a great business has a price, and 98 times leaves no room for a single soft quarter.

Insider activity sharpens the bear’s point. Over the past six months, CrowdStrike insiders recorded more than 1,000 open-market sales and zero purchases, including sales by Kurtz himself in the days before the split. Much of this runs through pre-arranged plans, so it is not a smoking gun. But it is not the picture of a leadership team that thinks the stock is cheap, either.

The counterweight is what the Street has done since the quarter. Bernstein, the most cautious major shop on the name, still raised its target to $413 from $368 while keeping a Market Perform rating, a target that now implies more than 40% downside. Goldman Sachs moved to $726. Morgan Stanley raised its target on what it called accelerating ARR confidence. The Street’s mean target sits around $715, which is the unusual part: after the June 29 close, CrowdStrike trades slightly above where the average analyst thinks it should be. Of the latest estimates, 30 are Buys, 11 are Outperforms, 11 are Holds, 1 is an Underperform, and there are no Sells, with 2 analysts offering no opinion.

See how CrowdStrike performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $742.91

- Target Price (Mid): ~$1,230

- Potential Total Return: ~66%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for CrowdStrike stock (It’s free!) >>>

TIKR’s valuation model, built on mid-case assumptions, sees further upside even from here. The model targets a price of around $1,230 by January 2031, implying a potential total return of about 66% and an annualized IRR of roughly 12% per year over the next 4.6 years. That target sits above the Street’s mean, which reflects how recently the stock re-rated and how much the model leans on durable compounding rather than a near-term multiple.

This article uses the mid case because it best captures the central question: not whether CrowdStrike grows, but at what pace and at what margin. The two revenue CAGR drivers are platform consolidation through the Falcon Flex subscription model, where re-Flex customers expand spending an average of 51% over their original contract, and the new AIDR category that management believes can eventually exceed the endpoint business. The margin driver is operating leverage: non-GAAP operating margin expanded 530 basis points year over year to 24% as scale benefits compound. The primary risk is the multiple itself. A stock at 98 times forward EV/EBITDA re-rates downward fast when growth disappoints, exactly as it did in February.

The upside: if CrowdStrike sustains 20%-plus revenue growth and converts AIDR demand into durable ARR, the mid-case target points to roughly 66% total return over the next 4.6 years.

The downside: if net new ARR growth slips back below 25% and the multiple compresses toward the Street’s most cautious view, the stock has more than 40% of room to fall to Bernstein’s $413.

Conclusion

The split is cosmetic. The real test arrives with second-quarter fiscal 2027 results, which the company is expected to report in late August. Management guided to net new ARR of $284 million to $286 million, up 28% to 29% year over year. That is the number that confirms or breaks the thesis. Above the high end, and the AI-security inflection story holds and the premium looks earned. Below $284 million, and the bears who pointed to insider selling and a 98-times multiple get their evidence that the easy gains are behind the stock. Watch that ARR line in August. The split will be long forgotten by then, but the growth rate will tell investors everything they need to know.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in CrowdStrike?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CrowdStrike, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CrowdStrike alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CrowdStrike on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!