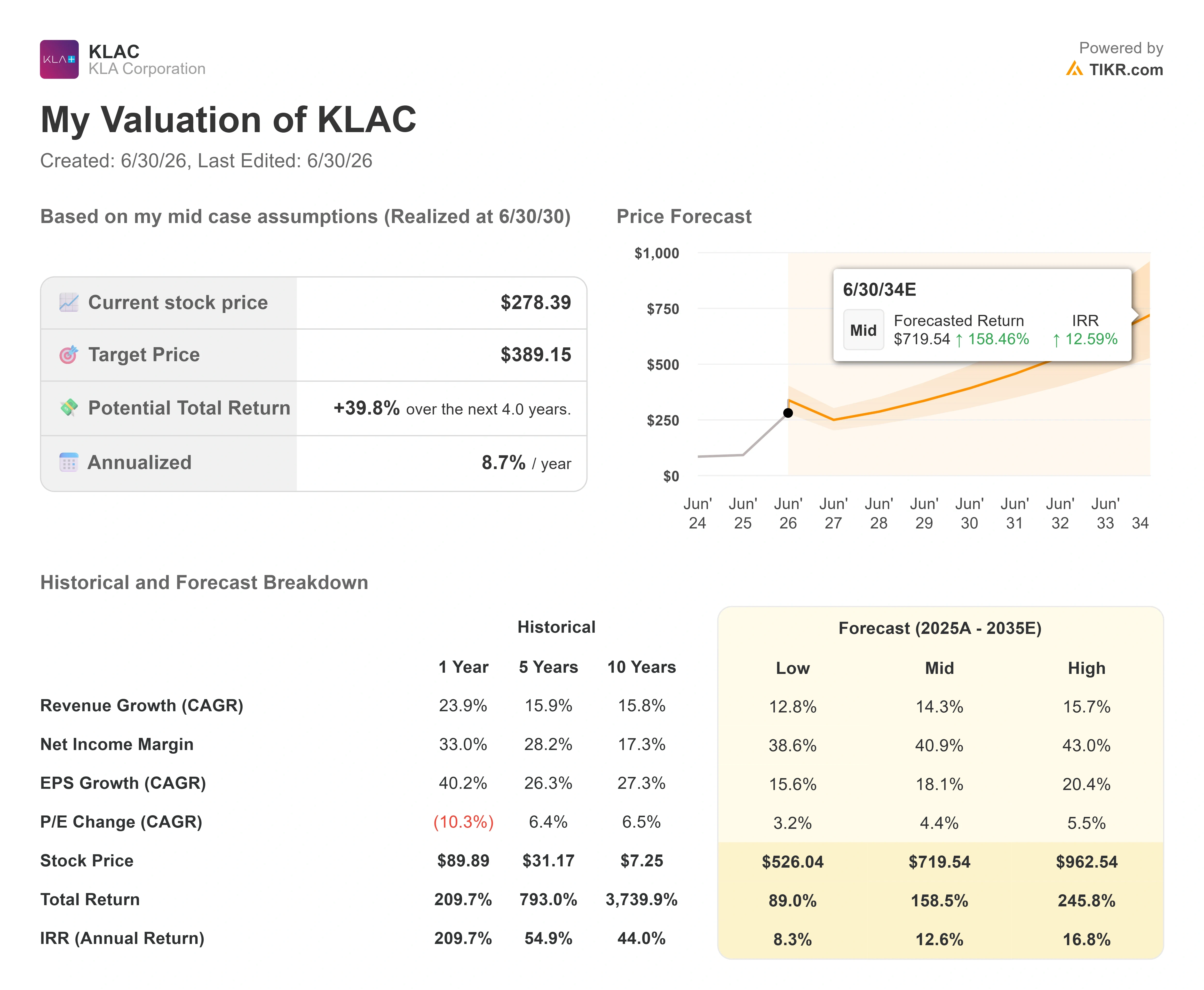

Key Stats for KLA Corporation Stock

- Current Price: $278.39

- Target Price (Mid): ~$390

- Street Target (Mean): ~$214

- Street Target (High, Cantor): $325

- Potential Total Return: ~40%

- Annualized IRR: ~9% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

KLA Corporation (KLAC) closed up 11.97% on June 29, a near-$30 jump to $278.39 that came six days after the same stock fell more than 9% on someone else’s bad news. That whipsaw is the story. The bounce was sharp, it was fast, and it pushed a stock that bears had just left for oversold back toward its highs. The question investors are now asking is simple: was that a fundamental re-rating, or a relief rally that ran on positioning?

The proximate cause is easy to name. On June 29, Cantor Fitzgerald raised its price target on KLAC to $325 from $250 and kept an Overweight rating. That $325 is now the highest target on the Street. The firm framed the AI infrastructure buildout as a generational semiconductor cycle, durable and extended by supply constraints, with total industry revenue potentially reaching $3.5 trillion by 2030. That is the size of the whole semiconductor market, not KLA’s slice of it, but as the dominant process-control supplier, KLA captures a growing share of the equipment spending that growth requires.

Here is the tension. The highest analyst on the Street just set $325, roughly 17% above today’s price, but the average analyst target sits at around $214, below where the stock trades right now. So one well-followed firm sees clear upside while the consensus sees downside. Neither can be right, and the gap between them is exactly what makes KLA stock in 2026 hard to call.

Why the rebound happened when it did

The setup mattered as much as the catalyst. KLA had dropped 9.17% on June 23 after a report that South Korea’s SK Hynix was slowing its high-bandwidth memory ramp, the stacked memory that feeds AI chips, to protect conventional DRAM margins. That move had nothing to do with KLA’s own business. It hit the whole AI-memory complex, and KLA fell with the group.

By late last week, the stock was technically oversold. When Cantor’s note landed on an already-stretched short base, the snapback was violent. Short covering amplified the move, which is why a single target raise translated into a near-12% session rather than a 2% one. That dynamic cuts both ways. It explains the size of the bounce, but it also means part of the move was mechanical, not a vote on fundamentals.

The fundamentals underneath, though, have been firming for months. At the Bank of America Global Technology Conference on June 3, CFO Bren Higgins put the 2026 wafer fabrication equipment market, the tools chipmakers buy to build chips, at “$140 billion plus” and said it might end up “a little bit stronger than that.” He was more striking the following year. “The visibility is really remarkable to be midway through ’26 and be talking about ’27 and talking about ’27 with meaningful growth expectations,” Higgins said. That matters because backlog visibility this early signals customers are locking delivery slots for fabs opening in 2027, which converts today’s urgency into tomorrow’s revenue.

See historical and forward estimates for KLA Corporation stock (It’s free!) >>>

The packaging number that keeps getting bigger

The most concrete growth data point Higgins gave was on advanced packaging, the back-end process of connecting and stacking chips that AI processors increasingly depend on. KLA’s process control revenue from packaging is tracking toward $1 billion in 2026, up from $635 million last year and roughly $300 million the year before. “We’re going to be $1 billion in packaging, up from $635 million last year and $300-ish million the year before,” Higgins said. “So it’s been quite a run.”

That growth matters because it is structural, not cyclical. Less than three years ago, KLA held under 1% of the advanced packaging market. It now holds over 6%, and Higgins guided toward the mid-7% range by year-end. As chipmakers move to hybrid bonding and die-stacking, back-end packaging is demanding inspection complexity that looks more like front-end chip manufacturing, which pulls KLA’s tools into a market that barely existed for it a few years ago.

There is a reason the whole franchise compounds. Higgins put it plainly when describing why high-value chips drive more inspection: bigger, more valuable die mean a single defect destroys a larger share of yield, so customers inspect more, not less. KLA runs about 7.5 times the process control share of its nearest competitor, which turns that “inspect more” reflex into a direct revenue tailwind.

What the valuation actually says

This is where the bull and the bear meet. KLA trades at around 48 times next-twelve-month EV/EBITDA per TIKR, against a peer median near 33 times. ASML sits around 36 times, Applied Materials around 40 times, and Lam Research around 47 times on the same measure. KLA carries the richest multiple in its peer group, and the premium is the entire debate. Bulls argue it is earned: best-in-class margins, a service business with 80% of revenue under long-term contract, and a widening share position inside a growing market. Bears argue a process-control leader tied to a cyclical end market should not trade at growth-software multiples, and that the consensus $214 target is the Street saying exactly that.

The reported numbers support the quality case. KLA’s gross margin runs at 61.4% and its operating margin at 41.7% on a trailing basis, both well ahead of the equipment-maker field. The risk that keeps the premium honest is geography. China contributed roughly $4.04 billion of KLA’s $12.16 billion in fiscal 2025 revenue, and tightening U.S. export controls are expected to trim that contribution. A premium multiple plus a concentrated policy risk is a combination that can re-rate fast in either direction.

There is also a real cash-flow wrinkle worth watching. KLA’s free cash flow conversion missed estimates in recent quarters, even as earnings beat, with reported free cash flow coming in below the Street’s expectation in the March quarter. For a stock priced for everything to go right, the gap between accounting earnings and cash generation is the kind of detail that decides whether a 48x multiple holds.

See how KLA Corporation performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $278.39

- Target Price (Mid): ~$390

- Potential Total Return: ~40%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for KLA Corporation stock (It’s free!) >>>

Using TIKR’s mid-case scenario, the model points to a target of around $390 by mid-2030, implying roughly 40% total return from today’s price, or about 9% annualized. That mid case runs on a revenue CAGR of around 14% off KLA’s $12.16 billion fiscal 2025 base. The two primary revenue drivers are advanced packaging process control compounding from a $1 billion base, and rising inspection intensity at leading-edge DRAM nodes as EUV lithography adds more control steps per layer. The margin driver is operating leverage, with management targeting gross margins of 63% to 64% and the upper end of its 40% to 50% structural operating margin range; the mid-case net income margin assumption is around 41%.

The upside: if Cantor’s read on a multi-year, supply-constrained cycle proves right, second-half acceleration and packaging share gains push earnings and the multiple higher together.

The downside: a China export-control escalation hits the $4.04 billion revenue base the model depends on, and a premium multiple compresses fast. Notably, the model’s ~9% annualized return sits between Cantor’s $325 optimism and the Street’s $214 caution, a reminder that even the bull case here is a high-single-digit compounder, not a doubling.

Conclusion

The June 29 bounce told you what the market does when a beaten-down quality name gets a fresh bull target on an oversold base. It did not tell you who is right. That answer comes July 30, when KLA reports fiscal fourth-quarter results against guidance of about $3.575 billion in revenue. Watch two things, not one. A revenue print at or above that guide confirms the second-half ramp the whole thesis rests on. But watch free cash flow just as closely: another quarter where cash conversion trails the earnings beat would hand bears the valuation argument even on a top-line win. Above guide on both, and the $325 case has data behind it. A miss on either, and the consensus $214 starts to look like the more honest number.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in KLA Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KLA Corporation, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track KLA Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze KLA Corporation on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!